The Significance of Changes in the Current Account Balance

Japan’s current account balance had securely and consistently remained in surplus since the 1980s. The current account surplus as a percentage of nominal GDP stood at 2% to 3%. However, a turnaround occurred in 2011, when the surplus started to decline. The current account surplus as a percentage of GDP was at 1.0% in 2012 and 0.7% in 2013. This is because the trade balance, which had been recording a major surplus until then, moved into deficit (Figure 1).

So why did the trade balance move into deficit? This change in the trade deficit was a result of a confluence of the following three factors.

First, the export volume declined. The export volume in 2012 was 7.4% lower compared with that in 2010. This can be attributed to factors that kept a lid on exports, such as the global economic slowdown as a result of the European debt crisis, the disruption to the supply chain resulting from the Great East Japan Earthquake as well as the deterioration in Japan-Sino relations.

Komine Takao, Professor, Hosei Graduate School of Regional Policy Design

Second, import volume increased. Import volume rose by 5.4% during the same period. This was due to an increase in imports of oil and LNG as a substitute for nuclear power.

Third, the growth rate in import prices was higher than that of export prices. During the same period, export prices rose by 2.1%, while import prices increased by 10.4%. This is mainly because of a surge in energy prices. In short, it means that the terms of trade (the ratio of export prices and import prices) deteriorated.

Looking at conditions in 2013 , export volumes declined by 1.5% from the previous year, showing no change to the sluggish conditions, while import volume remained more or less unchanged (up 0.4%). Both import and export prices rose due to the weakening yen that started in late 2012, but the rise in import prices was greater than that for export prices, showing that there was no change to deteriorating terms of trade (export prices rose 11.1%, while important prices increased 14.5%).

So will the current account balance continue to remain in deficit? Many Japanese economists do expect Japan’s current account balance to remain in deficit over the long term. This is a reflection of the aging population. Specifically, as a population ages, the savings rate for the entire economy declines as the percentage of workers who save in the population declines, while the percentage of those who spend their savings, namely retired persons, rises. When this happens, the country will move from having a savings surplus to a savings deficit. If we look at it from the perspective of a savings and investment balance, a deficit in savings in the country is synonymous with having a current account deficit. This is the story behind how a change in the composition of the population can bring about a deficit in the current account.

With the current account moving rapidly toward deficit since 2011, the day when the current account would be clearly in deficit looked as if it could occur much sooner than originally thought. This school of thought is based on one that says that the current account deficit, which advanced rapidly after the earthquake, will continue to trend in the same manner into the future. In other words, Japan’s current account deficit will move deeper into deficit amid a move among Japanese corporations to shift their manufacturing bases overseas, the move toward dependency on overseas energy sources and the trend of these energy prices to remain at high levels.

The problem lies in how we should assess this move toward a deficit in the current account balance. Many people appear to think that the decline in the current account surplus or posting a deficit is bad for the economy. However, this is not necessarily correct.

What I would like to stress here is that the current account itself is not seen as an overly important target in the context of economic policy. Industrialized nations, including Japan, have positioned the following as important policy targets: keeping growth rates as high as possible at a sustainable level, ensuring stable prices, and keeping the unemployment rate as low as possible. No country has named the current account balance as a policy target.

This is not surprising. Public welfare will clearly erode if economic growth wanes, prices surge or if the unemployment rate remains at high levels, but public welfare will not be tarnished by a change in the current account balance.

Regardless, many people tend to think that a current account surplus is better than a deficit probably because they think that an increase in exports is positive and an increase in imports is negative for the economy. Still, exports are a means to secure income, and by using this earned income to import the necessary goods, the country’s living standard will improve. In other words, an increase in both exports and imports is precisely what benefits trade.

Still, this does not necessarily mean that the move of the current account into deficit is problem free. The fact that the shape of the current account balance itself is in the process of transforming means that some part of the economy that surrounds us has changed (or could possibly change). From this standpoint, what we need to consider are the changes in the terms of trade and the relationship of the current account to fiscal deficit.

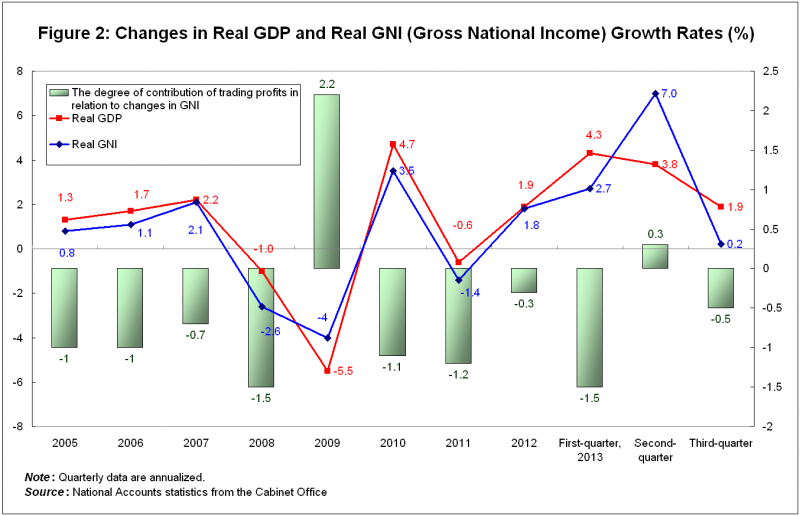

As noted earlier, one of the main factors behind Japan’s trade balance moving into the red was the deterioration in the terms of trade. It is clear that a deterioration in the terms of trade erodes national welfare. Since there will be a decline in returns from exports, actual income will not rise as much as the actual work performed. This change in the terms of trade appears in the form of trade gains (or trade losses) in Gross National Income (GNI) statistics. As shown in figure 2, the growth rate of GNI is lower than that of GDP during most of the periods, making it apparent that the main factor is due to trading losses. We are facing a situation in which our standard of living will not improve (the GNI will not increase) despite our workload (despite GDP growing), and this is because of the deterioration in the terms of trade.

This is a result of corporations having to work on raising export prices in some manner, such as by cutting costs, lowering wages and earning reduced profits, in contrast to the change in the operating environment to date, such as a strong yen or a rise in energy prices. This type of response, in which companies curb their added value, did help secure export volume and was successful in preventing GDP from declining, but on the other hand, it brought about a deterioration in the terms of trade and pushed down real GNI. To prevent this from happening, it is important for Japanese companies to be able to exhibit their capability to create added value by improving their ability to develop technology and human talent.

Next, let us look at the relationship between the current account balance and Japan’s fiscal deficit. A current account deficit signifies a lack of funds in the country, and thus if the current account dips into deficit, it becomes more likely that Japan will need to depend on overseas markets to finance its fiscal deficit. If this happens and the assessment of Japanese government bonds is harsher among overseas investors than among domestic investors, there is a greater possibility of investors starting to question the confidence placed on JGBs.

That said, it would be a mistake to pursue a surplus in the current account balance. Fiscal reform is the correct response to a fiscal deficit, and even if the current account remains in deficit, the government should proceed with fiscal reform so that confidence in JGBs does not waver.

As shown above, instead of worrying about the current account remaining in deficit, it is important to closely investigate the factors that are behind the current account deficit and then create a new growth model from the findings and work diligently on preventing the deficit from recurring.

Translated from an original article in Japanese written for Discuss Japan. [February 2014]

Related posts:

Farewell to Mega-pessimism

Farewell to Mega-pessimism

Concerning a Target Population of 100 Million

Concerning a Target Population of 100 Million

The Illusion and Dilemma of Innovation that Permeate Japan

Soros’ Warning of a Hard Landing in China and Tremendous Adjustments to Its Debt Economy

The Illusion and Dilemma of Innovation that Permeate Japan

Soros’ Warning of a Hard Landing in China and Tremendous Adjustments to Its Debt Economy

Legacy of “Japonisme 2018” (I): Transitioning from International Expositions to Exhibitions of Japanese Culture

Legacy of “Japonisme 2018” (I): Transitioning from International Expositions to Exhibitions of Japanese Culture