Japan’s Economic Outlook for 2020

Prof. Komine Takao

In this article, I would like to discuss some of the points that are crucial to Japan’s economic outlook for 2020.

First, we should examine whether or not the Japanese economy has peaked out. A reference date related to a peak or a bottom in a business cycle is determined by the Economic and Social Research Institute of the Cabinet Office. It usually takes more than a year for them to determine whether a peak or a bottom has actually occurred in a business cycle because their judgments require comprehensive statistical information pertaining to a certain period of time. This suggests that the government research institute may have missed an opportunity to announce a reference date of a business-cycle peak in a more timely manner simply because comprehensive statistical data are not yet available for them to make a judgment. This assumption sounds extremely plausible. In fact, many experts argue that the Japanese economy peaked out in or around October 2018.

According to the ESP Forecast Survey (in January 2020), a poll of 40 leading economists conducted on a regular basis by the Japan Center for Economic Research, 11 out of 34 respondents believe that the Japanese economy has already been in a recession for around a year. I believe that the business cycle in Japan peaked out in or around October 2018, as pointed out by a limited number of economists, given the second point to follow next.

Second, we should observe how the US-China trade disputes develop. It appears that President Trump believes that import cuts will help production and employment to grow in America, but his theory is completely wrong in economics. Higher import tariffs imposed by the United States will be followed by retaliatory tariffs on American goods imported by other nations, which will eventually result in lower exports from the United States to the rest of the world, sending global trade into a diminishing spiral.

These concerns appear to have materialized already, as seen in a series of reactionary developments that have followed since fall 2018 in the wake of the US-China trade conflict causing slower growth in global trade, which has resulted in a reduction of Japan’s exports and lower industrial production. Typically, a slowdown in exports triggers a slide into an economic recession for Japan. Considering all these developments, I believe that Japan has already entered a recession.

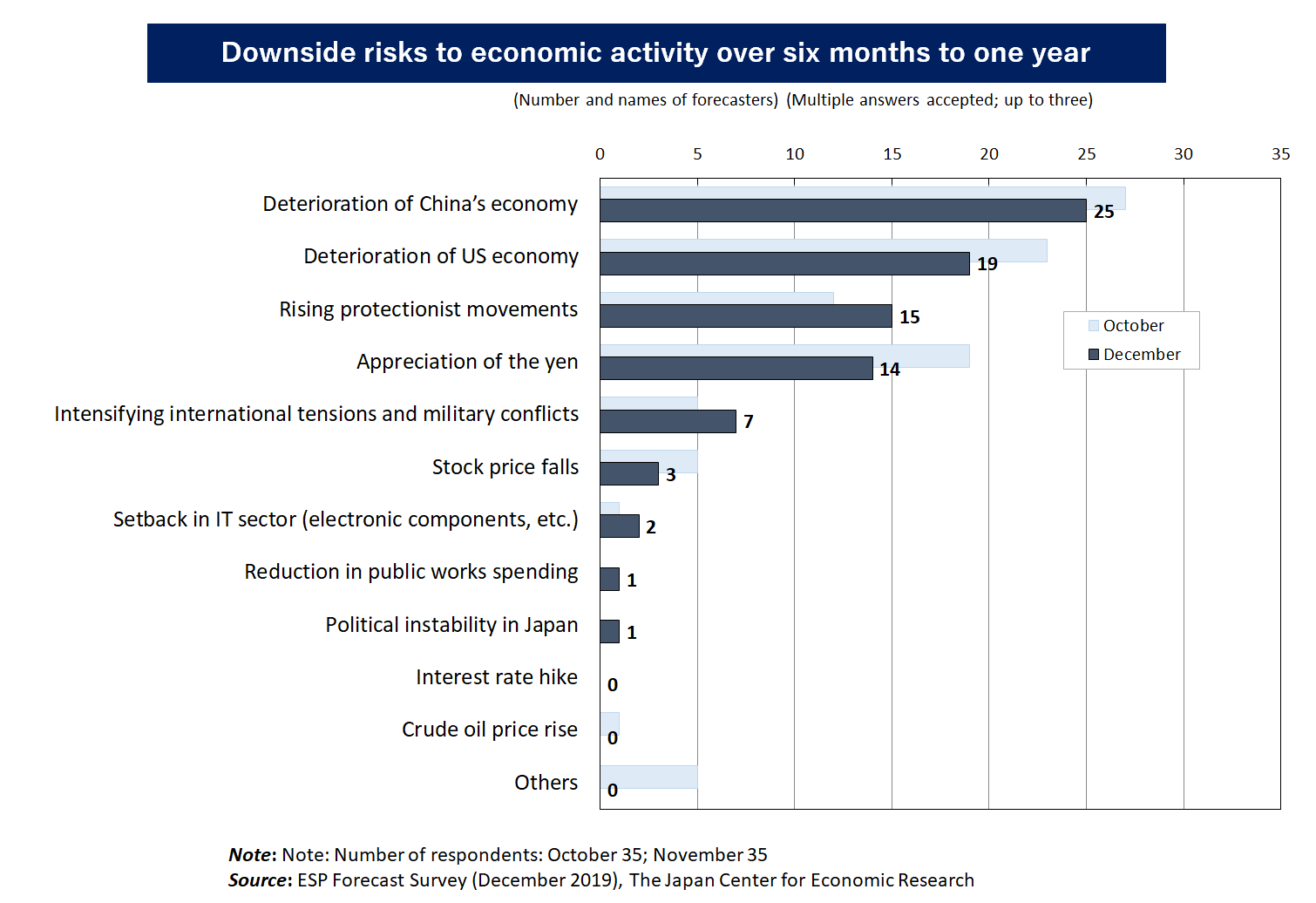

In the ESP Forecast Survey that I mentioned earlier, Japan’s leading economists were asked what they believe to be potential downside risks for the economy over the coming 6–12 months. The December 2019 survey results indicate that China’s economic slowdown was the most common risk perceived among the polled economists, which was followed by the slowdown of the US economy, rising protectionist movements and the stronger yen. (Please refer to the Figure.)

There is some concern that a further setback in China’s economy, a slide into a recession of the US economy or a further escalation of the US-China trade disputes would cause global trade to diminish, resulting in the deterioration of the Japanese economy along with a reduction in exports.

Third, we should analyze how our economy would be affected by “external shocks” such as the impact of the consumption tax hike implemented in October 2019 and the Tokyo 2020 Olympics.

A consumption tax hike usually affects the economy negatively in two ways: a reactionary plunge following a spike in demand ahead of the tax hike; and a reduction in real income among households with higher commodity prices. Rush buying and a reactionary plunge in demand that subsequently follows are essentially a temporary set of phenomena, and I do not expect that the tax hike will have a lingering effect in 2020. Meanwhile, we must pay attention to the impact that a reduction in household real income might have on the economy. That being said, I believe that it will have a limited impact because the higher tax rate does not appear to have pushed consumer prices up much, which would therefore not reduce real household income much either.

According to my general observations, a rise in consumer prices following the tax hike appears to have been limited to 0.8%, with reduced tax rates applied to some grocery items and daily necessities. Meanwhile, the government has made day care services and preschool education free for children using the new consumption tax revenue. The free preschool education initiative essentially had the same impact as reducing the service fees in terms of consumer prices, resulting in a 0.6% reduction in commodity prices. I believe that this offset the overall 0.8% rise in consumer prices, pushing up overall consumer prices by just 0.2%.

In addition to the reduced tax system, the government has taken some other measures to alleviate any negative impact of the consumption tax hike, including the introduction of a reward points program for cashless payments and premium shopping vouchers as well as higher public works spending. I believe that these countermeasures will be sufficiently effective to offset the economic effects of the hike.

It appears that many experts expect to see the Japanese economy beginning to fall into a recession after the Tokyo 2020 Olympics. It is true that Japan began facing a setback in its economy soon after the previous Tokyo Olympics in 1964, reflecting a significant reactionary plunge in demand for large-scale social infrastructure projects in succession ahead of the incredibly important international event for Japan, notably with the construction of the Shinkansen high-speed rail system, monorails and the metropolitan expressway. On the other hand, social infrastructure investments that have been made for the Tokyo 2020 Olympics appear to be far smaller in size compared with those made for the previous Tokyo Olympics back in 1964, which leads me to believe that a reactionary plunge this time around would probably be much less significant compared with that of the previous Tokyo Olympics in 1964.

As I mentioned earlier in this article, it will become clear to us during the course of next year as to whether the Japanese economy really peaked out in or around fall 2018. If not, Japan will mark its longest growth phase since the end of World War II, confirming the success of Abenomics. If yes, it would suggest that the country’s economy has, in fact, been experiencing a setback for more than a year. If this turns out to be the case, the government will come under criticism for inconsistencies, because it has kept saying in its Monthly Economic Report that the Japanese economy is recovering at a moderate pace.

In my opinion, however, it does not make a great deal of difference whether Japan’s economy did or did not peak out in the fall of 2018 because the economy achieved a long period of growth without achieving a noticeable expansion in scale, involving frequent standstills during the growth phase. Given these circumstances, many people seem to find it difficult to gain a real sense of economic growth, although Japan has actually been experiencing its longest growth phase since the end of World War II.

Meanwhile, even if Japan has been in a recession for some time, it has run its economy at almost full employment with a low unemployment rate. Corporate earnings have also remained strong. Given this situation, many of us may find it hard to gain a real sense of being in the state of an economic recession. In other words, our economy will simply grow further without people having a real sense of it or enter a recession without people realizing it. I would say that our economy will remain flat, anyway.

The fundamental problem for Japan is that its economy has been trapped in a structural low-growth phase beyond the business cycle. I believe that it will be imperative, among other things, for the Japanese economy to overcome the structural state of a low-growth economy. To achieve this goal, it will be necessary to improve productivity in conjunction with employment system reforms while dispelling people’s concerns regarding the future with fiscal and social security reform initiatives. Unfortunately, however, there are no signs of making these initiatives move forward yet. It looks like these issues will be pushed back during the course of 2020 in any event.

Translated from an original article in Japanese written for Discuss Japan. [January 2020]

Related posts:

Farewell to Mega-pessimism

Farewell to Mega-pessimism

The Prospects for the Japanese Economy with a Higher Consumption Tax

The Prospects for the Japanese Economy with a Higher Consumption Tax

The term “innovation” should not be limited to technical innovation: A misunderstanding has seen downgraded from “gain a profit.”

The term “innovation” should not be limited to technical innovation: A misunderstanding has seen downgraded from “gain a profit.”

Legacy of “Japonisme 2018” (I): Transitioning from International Expositions to Exhibitions of Japanese Culture

Legacy of “Japonisme 2018” (I): Transitioning from International Expositions to Exhibitions of Japanese Culture