WHAT GIVES KOREAN COMPANIES THEIR EDGE?

“The global economy is a tiger. All we can do is keep riding on its back. If we get thrown off, we’ll be eaten up.” This was the grim determination expressed by a senior South Korean official charged with directing his country’s structural reform program following the 1997-98 currency crisis. In hindsight, that East Asian currency crisis was a harbinger of the global financial crisis that struck in 2008. South Korea, facing the shock of the backwash from the global economy that hit in the wake of the earlier crisis, decided to go with the flow. Its trade dependency ratio rose from 58% in 2001 to 92% in 2008. The collapse of Lehman Brothers in September that year marked the start of a financial crisis that spread through the global economy, but despite this, South Korea’s trade dependency figure declined relatively little; the ratio for 2009 was 82%.

The structural reforms that South Korea implemented in the wake of the earlier crisis led to its success in weathering the more recent one. It was one of the few advanced economies to record a positive growth rate for gross domestic product in 2009, and this year it has been quick to ride the wave of global recovery. In the first half of 2010 the economy expanded at a rate of 7.6% year on year, powered both by strong performance in exports (up 15.0% from the first half of 2009) and by upturns in domestic capital investment and consumer spending. Current profits for the first half of the year at listed corporations (with business years ending in December) surged by 124.2% from the previous year, contributing to a recovery in businesses’ appetite for investment and a lessening in concerns about jobs. In July the Bank of Korea hiked its benchmark interest rate by 0.25 percentage points, and though the outlook for the second half of the year is uncertain, it is hoped that the growth rate for the year as a whole will come to around 6%.

Factors behind this successful performance include (1) growth in emerging markets, (2) the weakening of the South Korean won, and (3) nimble policy support from the government, all of which have contributed to a considerable strengthening of the competitive edge of major corporations. South Korea’s big companies have fully accepted the forces of globalization; what message does their performance send to Japanese business?

Paradigm Shift Toward the Emerging Markets

The growth of the emerging economies has contributed greatly to the strong performance of South Korea’s major corporations. Up to the year 2000, the markets of the emerging countries accounted for less than 30% of world trade, but as of 2009 their share had risen to around 40%, and it is only a matter of time until the figure tops 50%. Korean companies understood the shift taking place in the global structure of trade, and they focused efforts on developing the emerging markets. South Korea’s exports to these markets grew by 228.2% from 2000 to 2009, and their share of the country’s export total topped the 50% mark in 2002, reaching 66% in 2009. The Chinese market now accounts for a quarter of the total, and exports to the members of the Association of Southeast Asian Nations exceed both those to the United States and those to Japan.

Originally South Korean companies moved into the emerging markets out of necessity rather than by choice. Over the years Korean industry has been racing to catch up with Japan, and each time the Koreans have reached a goal, competition between the two countries’ companies has intensified. Japanese companies have done their best to shake off the pursuit of their Korean rivals by devoting themselves to research and development, shifting to products with greater added value, and thereby holding on to their leading positions in the high-end markets of advanced countries. And they have enjoyed a domestic market that is one of the world’s biggest. The South Koreans were thus forced to turn to the markets of the emerging countries–places seen as presenting high risks, both politically and economically, and offering little depth. People in the Korean business world openly expressed such concerns about these markets.

Thanks to globalization, though, it became possible for business resources of every sort to move freely around the world, and big emerging countries like China and India found themselves with opportunities for completely new forms of development. China turned itself into a global center for manufacturing, taking advantage of direct investment in the form of packages including goods, money, and technology. And India grasped the chance to develop as an outsourcing destination in such fields as information technology and engineering. Rapid economic growth in these countries with big populations led in short order to the emergence of domestic middle-income markets, with the spread of the Internet and mobile phones contributing to the growth of a new class of consumers. Companies from South Korea, whose own middle class had grown sharply and which had been quick to embrace IT, were quicker than their Japanese counterparts to take note of this paradigm shift in the global economy and to set out in pursuit of the new opportunities it offered.

The nature of demand in emerging markets is affected by constraints from their limited infrastructure, and products do not necessarily have to be at the high end of the range. Korean firms, which had been prompted by the crisis of the late 1990s to shift their focus from manufacturing superior products to manufacturing products that would sell, found themselves better positioned to tap demand in the emerging markets than in the mature markets of advanced countries, where they struggled against the brand-name power of earlier entrants.

Another point in the Koreans’ favor in the emerging markets was the decisive importance of speedy decision making. By the time a company moves to implement a plan that has been carefully formulated to the point of perfection, the intended market may well have shifted. In this respect the Korean style of business is a good match for the emerging countries. The corporate governance of South Korea’s family-managed big businesses came under harsh criticism at the time of the East Asian currency crisis, but management by owners has the advantage of allowing swift and bold decisions. And in many cases the business counterparts in the emerging countries are also family-run firms, so that talks between the top executives serve as a key element in forming ties between companies. In addition, after the currency crisis, Korean companies implemented rigorous meritocracy and delegation of power, with the result that they have developed highly talented and specialized senior management teams to run their operations. Their high-speed management has shown its strength in the new age of the emerging markets.

A Weakening Won Helps the Koreans Win

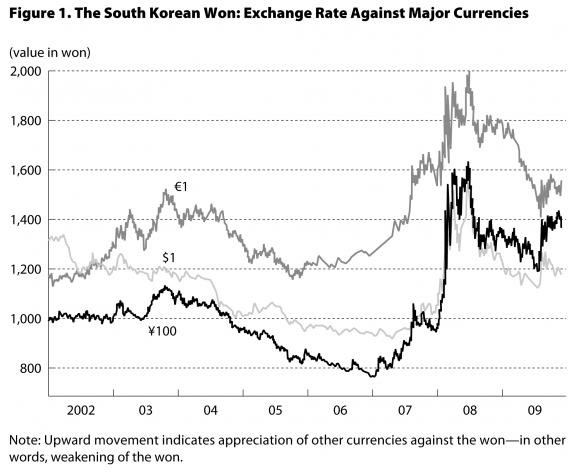

Since the recent global financial crisis struck, South Korea’s won has weakened against other currencies, and this has further helped Korean companies to do business around the world. As the attached chart shows, the won appreciated against the dollar, euro, and yen from 2004 through 2007, but when the global financial crisis struck, the size of the country’s short-term external liabilities became a cause for concern, and after September 2008 Korean banks found it hard to raise funds. This development, accompanied by a sharp drop in the stock market, caused the won to start losing value again. This year the exchange rate has continued to run about 20% lower than the real effective rate. And the won has depreciated much more against the yen than against the dollar since 2009. The appreciation of the yen against the won has strengthened Korea’s hand in export markets, and it has also worked to the Koreans’ advantage in the competition for plant and construction orders, such as the one for a nuclear power project in the United Arab Emirates that a Korean consortium won over rival bidders from Japan and France.

To be sure, Korea relies on imports from Japan for many parts and materials, and the structure continues to be one in which an increase in Korea’s exports to the rest of the world causes its imports from Japan to rise in tandem. Much of this import trade is denominated in yen, meaning higher bills for Korean firms, and if firms also have debts in yen, they face a higher repayment burden as well. But if we look just at the major companies, we find that their debt ratios are low and they have plenty of liquidity on hand, so they are not feeling the sort of pinch they did in the wake of the currency crisis. Meanwhile, the yen’s appreciation has promoted the flow of direct investment from Japan to Korea, which surged from $990 million in 2007 to $1.93 billion in 2009. Investment aimed at production in fields including semiconductors, liquid-crystal panels, and environment-related industries has risen, and improved quality has led to an ongoing increase in exports to Japan as well. Overall South Korea has benefited greatly from the yen’s rise against the won.

Korea Inc. in the Global Age

South Korea’s major corporations have also benefited from the support of what we might call a new “Korea Inc.” in the form of agile economic policy management by the government. Immediately after the financial crisis struck in 2008, the authorities pledged fiscal stimulus on the order of 3.6% of GDP, a level second only to that of Russia. This topped China’s 3.1% of GDP, Japan’s 2.4%, and the United States’ 2.0% (Samsung Economic Research Institute). The stimulus included both public works and outlays aimed at promoting the takeoff of the environment industry through the provision of subsidies.

In addition, the South Korean government has actively worked at concluding free trade agreements with other countries. The FTA that South Korea negotiated with the United States still awaits ratification, but this year a pact with India went into effect (while Japan’s is still pending), and the agreement that has been completed with the European Union will go into force in July next year. The EU imposes some relatively high tariffs: 10% on automobiles, 4.5% on auto parts, 14% on color televisions, and 8% on bearings. Korean automakers, like their Japanese counterparts, have been shifting to local production in the EU, but the FTA is expected to promote a switch to Korea for supplies of parts and other highly competitive products. Meanwhile, the prospect for conclusion of a Japan-EU FTA is nowhere in sight. The Koreans are also expecting their FTA with the EU to result in a shift from Japan to the EU as the source of some of their own import supplies. And this pact is likely to have an impact on the reopening of FTA negotiations with Japan, which have been put on hold, and on the start of similar negotiations with China.

Another key factor is that President Lee Myung-bak is himself a former chief executive of a major corporation and is enthusiastically undertaking top-level economic diplomacy. Like Japan, South Korea has a strategy toward the emerging markets that is not limited to the export of goods but also extends to infrastructure-related plant exports and construction projects and the development of energy and other resources as central elements. The Blue House (president’s executive office) directs political support on a unified basis, and in line with its wishes various state-owned corporations and other public-sector organizations, such as Korea National Oil Corporation, Korea Electric Power Corporation, and Korea Railroad Corporation, cooperate with private-sector firms in winning project orders and developing new markets.

Unlike advanced countries where state-owned enterprises have been privatized, South Korea still has many public-sector corporations, which are in a position to take on greater risks than private-sector businesses. Meanwhile, civil servants and employees of public-sector corporations are subject to performance rating, and because jobs at major private-sector firms are limited, many talented people have gone to work in the bureaucracy and other public-sector organizations, which are thus quite capable of implementing projects. We can see a big difference between Japan and South Korea in this respect. In Japan, private-sector businesses have their hands tied by strict compliance requirements, and the political picture is unsteady, with cabinet ministers being frequently replaced; meanwhile, the panoply of independent administrative agencies and other government-affiliated organizations are now feeling the heat from the program-screening process being implemented by the current administration. In South Korea, by contrast, “Korea Inc.” is fully functional and has accepted the need to go global.

A Growing Competitive Edge

Benefiting from the three factors described above, South Korea’s companies have made great advances. In the Fortune Global 500 rankings of companies for 2010 by revenues, Samsung Electronics ranked number 32 ($108.9 billion); among Asian manufacturers it was topped only by Toyota Motor. LG, at number 67, beat out Sony (69) and approached Panasonic (65). In terms of profits, Samsung Electronics, with a figure of $7,562 million, shone by comparison with Japan’s Hitachi (47), Panasonic, Sony, Toshiba (89), Fujitsu (138), NEC (185), and Sharp (264), which all added together recorded losses of $1,745 million. Meanwhile, Hyundai Motor (78) is racing to catch up with Japan’s Toyota (5), Honda (51), and Nissan (63); if one includes the figures for its affiliate Kia Motors, its unit sales in 2009 topped those of Honda, putting it in the fifth spot among the world’s automakers, and it is considered certain that it will overtake Ford by this measure in 2010 to grab fourth place.

Until around the middle of the 2000-2009 decade, Korean manufacturers of consumer goods competed by turning out simple, stylish products designed to be easy to use; they avoided the tendency seen among Japanese companies to load on multiple functions in a quest for greater added value. But in the past few years the Korean companies have been focusing on quality. Samsung Electronics has won a string of awards from EISA, the European Imaging and Sound Association, and it has been some time since it surpassed its Japanese rivals in terms of the number of patent applications filed in the United States. In another of the many examples of Korean firms winning attention for high quality, Hyundai Motor’s Genesis won the North American Car of the Year award for 2009. The improved quality of final products shows the quality of the parts and materials Korean manufacturers are using, and it also indicates that they have become better at making all the elements work together. While Korean firms continue to rely on imports from Japan for some of their parts and materials, they have been shifting to domestic production of them on the basis of profitability criteria, and they have acquired export competitiveness in this area. The share of parts and materials in South Korea’s total exports has risen sharply, and in the first quarter of 2010 it topped 50%.

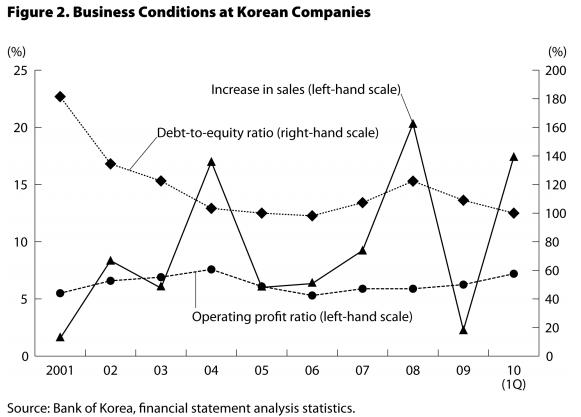

The implementation of structural reforms has led to increased earning power at major companies in South Korea, and their finances are also in better shape. Figure 2 shows that, while the rate of increase in their sales has fluctuated greatly, they achieved a quick V-shaped recovery in the first quarter of 2010 from the sharp downturn in 2009. Meanwhile, their operating profit ratios have held steady in the 6%-7% range, and their debt-to-equity ratios have been steady in the vicinity of 100%. If we compare this performance with that of Japanese corporations, whose sales dropped 5.7% in 2008 and whose operating profit ratio was a mere 1.5%, we can clearly see that South Korea’s companies have been able to display their strength even under difficult conditions.

Two Weak Points

Are there no weak points that may affect South Korea’s major companies adversely? The standard answer that one gets from Koreans themselves is the “sandwich” argument. This is the pessimistic assessment that South Korean industry is sandwiched between Japan, which has greater technological strength, and China, which has greater price competitiveness. If one looks simply at the production and pricing of goods, this assessment may be valid. But while Chinese companies may be able to supply assembled products and buy foreign firms, they are not yet able to build value chains extending from the procurement of raw materials through production, distribution, and sales based on their own brand names and relying on their own management setups. China also faces international pressure for revaluation of its currency. It makes little sense for Chinese companies to follow the lead of the Koreans in turning their focus away from their own domestic market, which in China’s case is the second largest in the world and is continuing to grow rapidly, and try to build an added-value chain in the highly competitive markets of the advanced countries.

With respect to their Japanese rivals, meanwhile, South Korea’s companies have reached a competitive level that is comparable, and they have almost completely caught up in technological power with respect to final products. If I were to cite a weakness, it would be that they continue to be feeble in the area of innovation; this, combined with their good business results, leaves them unable to set a new course. Samsung Electronics, which has become the world’s top maker of mobile phones, is poor at integrating its communication technology with its software and unable to come out with a smart phone like the iPhone, but it is not moving in the same sort of direction as Japan’s Nintendō either. And while Hyundai’s Genesis has won plaudits for its high quality, its market debut has failed to have the same sort of impact as that of Toyota’s Lexis in terms of making a statement and displaying cultural depth.

Korean companies have profited greatly in the context of globalization by following the leader, thereby avoiding the risks of basic research, and concentrating their investments in places where viable markets have already been shown to exist. But their reliance on this approach results in weak synergy horizontally among their own businesses, and it makes it difficult for them to embark on innovation-driven growth. In addition, they still tend to favor in-house solutions and find it difficult to rely on outside support for business development, such as that offered by Japan’s trading companies.

Another weak point is the flip side of the Koreans’ global orientation: In various respects the domestic South Korean economy has fragile foundations. Though it is ticking over reasonably well, the persistent concern about jobs and the swelling of household debt, along with the volatility of housing prices, have been putting dampers on consumer spending. The improvement in big companies’ financial condition has been produced through the rigorous pursuit of efficiency and performance-based personnel evaluation. Even though firms are enjoying steady export growth, most of them are reluctant to invest in production facilities within South Korea, where costs are high. They have passed on some of their profits to shareholders, executives, and employees, but the smaller companies that do business with them have benefited little. As a result, regular employment has been slow to grow. Meanwhile, companies have been effectively implementing mandatory early retirement. And unemployment among young people, 80% of whom are now university graduates, is close to 8%.

The bleak employment situation has been hurting household finances, and debt in the household sector, after being hit by the collapse of the credit card bubble in 2003, is once again rising at a faster pace than disposable income. The fact that South Korea got drawn into the global financial crisis was a result of the high level of mortgage lending, which made outside observers associate it with the United States. The country is not on the verge of experiencing defaults on a large scale, but domestic consumption faces the risk of a major drop in housing prices, and it is structurally difficult to expect innovation from the domestic market.

Benefiting from the Weaknesses of Japanese Firms

Though South Korean firms may have additional weak points, a more important consideration for Japanese companies is the fact that their weaknesses have fed their Korean rivals’ strengths. Globalization has turned many of the strong points that Japanese companies previously boasted into weak points. Conversely, for Korean companies, which used to look up to Japan’s firms as unsinkable battleships, the process of coping with globalization has caused various weaknesses to end up becoming strengths.

For example, Japanese manufacturers seem still to espouse what one might call “technology fundamentalism.” Technology is of course important for a manufacturer. But if a company devotes so much money to research and development that it must scrimp on marketing, distribution, and other spending for its value chain, or if it delays making decisions regarding commercialization risks, it will be unable to keep up with changes in the market. Particularly in the case of emerging markets it is essential to make concerted moves to introduce the right products when the time is ripe. The notion that “products are sure to sell as long as they are good (from a technical perspective)” does not apply here. Following the structural reform process, financial departments have become much more powerful within Korean companies, which have switched to a policy of “making products that will sell.”

These companies’ strong earning power has in turn led to greater technological strength. The key point is recruitment of superior talent. Every time the going gets tough, Japanese companies fall back on the idea of working together as an “All Japan” team, but the major Korean companies are no longer fighting as “All Korea.” As Japanese companies repeatedly restructure, they shed personnel, and some of these people have gone to work for Korean firms, where they have become valuable sources of information, helping their new employers crack their Japanese rivals’ black box strategies. Naturally the Korean firms’ scouting is not limited to Japan but is an ongoing process around the world. This has been made possible by a combination of earning power, flexible promotion systems based on merit, and top management teams capable of conducting meetings in English whenever necessary.

Another major plus was that structural reform brought the liberalization of imports from Japan, making it possible for Korean companies to procure inexpensive, high-quality intermediate goods from Japan’s various well-developed supporting industries. Because of the heavy concentration of business in big companies, South Korea has not seen the growth of parts suppliers and other supporting industries like the ones in Japan, and for many years this was cited as a major weak point. The government officials and media that continue to rue South Korea’s trade deficit with Japan are still caught in this narrow, single-country mind-set. But in the age of globalization, it makes no sense to set up national barriers to procurement. And in Japan, where big companies have depended heavily on the domestic market, deflation has meant increasing pressure on suppliers to cut costs; this has in turn encouraged these smaller firms to look for customers outside of Japan, particularly in neighboring South Korea. So the big South Korean companies that gave up on building their own domestic supporting industries through the sort of patient efforts undertaken by their Japanese counterparts are now able to tap the full range of such industries in Japan.

Lessons for Japanese Business

For many years South Korea’s big companies took their Japanese counterparts as exemplars. But now the Koreans’ successes offer some important lessons for Japanese companies. One is the need to reconsider their “technology fundamentalism” and actively develop value chains globally. It has become impractical for firms to monopolize their technology, and so there is a limit to how far they can get just with the skilled manufacture of goods; they will have a hard time keeping up with competition against more recent entrants unless they are able to turn out products that form part of a value chain that also includes logistics, finance, advertising, customer services, and other elements. The emphasis that Korean firms place on design, marketing, and sales strategy allows them to take advantage of the weakness of their technology-obsessed Japanese rivals in these areas.

A second lesson is the importance of balance between technological strength and earning power. The original strength of the big Korean companies was their ability to decisively concentrate their investment on selected technologies, but the earning power that this generated has now come around to enhance their technological prowess through recruitment of talented personnel. If a company with poor earning power and limits on its R&D budget insists on scattering its money in every direction, the results will be scant, and the company as a whole is liable to find itself sinking. Some may argue that R&D spending must be sustained because interrupting it will cause the research setup to crumble. But in this age of globalization, it is easy for technology to shift from one company to another through movements of personnel and through business alliances. A company will lose out entirely if insistence on in-house technology causes its overall earnings to decline.

A third lesson from the Koreans’ success is the need for a new structure of cooperation between government and business–what we might call a new Japan Inc. The mainstream in global trade is now the formation of FTAs, and in the wake of the financial crisis governments have taken to intervening more actively in private-sector affairs. Making sure that domestic corporations are able to compete with their international rivals on a level playing field is an important role for governments to play, and close liaison between government and business is essential. Japan, with a lower level of dependence on exports than Korea, has lagged in creating this sort of cooperative setup–which is not to say that it has been able to come up with a strategy for growth led by domestic demand based on structural reform.

In the final analysis, the biggest difference between Japan and South Korea lies in their identities in the context of globalization. In the wake of the currency crisis of the late 1990s, South Korea clearly identified itself as an open, small economy without natural resources. The determination of an identity is what allows a country to create an overall framework, leading to the emergence of corporate strategies, prioritization of objectives, and development of tactical mixes. If Japan remains transfixed by the lingering image of its old status as the world’s number-two economy and fails to face up to the reality of globalization, it will be unable to find its own identity, and stopgap measures will be powerless to prevent the inexorable decline of its industries.

To be sure, the success of Korea’s big companies has come at a tremendous cost to Korean society. The level of income disparity is one of the highest among all the developed economies, as are the divorce rate and the rate of youth suicide, while the birthrate is in the bottom class. But Japan’s figures are not much better, and in terms of income disparity and unemployment they are in fact worse. In Korea, a national campaign to teach English has helped companies win international orders. In Japan, relaxed educational standards have produced a generation with lower achievement levels and little interest in other countries. Which of these two countries is looking ahead? And will Japanese companies be able to overcome the disadvantages that result from these developments beyond their control? These questions, arising from the Koreans’ success, are serious.

Translated from “Nihon kigyō wa naze Kankoku kigyō ni makeru no ka,” Chūō Kōron, November 2010, pp. 36-43; slightly abridged. (Courtesy of Chūō Kōron Shinsha) [November 2010]

Click here for an editorial comment on this article.