THE NEED TO TRANSFORM BUSINESS MODELS

February brought a shocking piece of news to Japanese people. They learned that their country has become a net importer of consumer electronics–the very goods it had once exported to every corner of the globe. It had already become clear previously that Japan had become an importer of large household appliances, such as washing machines and refrigerators, but statistics for 2010 show that Japan has also become a net importer of digital consumer goods, such as flat-screen TVs. This is not due simply to an increase in imports of goods from overseas. A major underlying factor is that Japanese consumer electronics makers have shifted their production offshore.

One manifestation of this can be seen in the electronics megastores in Tokyo’s Akihabara district. Many among the increasing number of Chinese tourists to Japan look forward to shopping at stores in this district. But since last year or so, some of these tourists have started to collar store staff and demand to know where the made-in-Japan products are. The Akihabara Electrical Town Organization, representing the district’s retailers, has reacted by submitting a petition to Japanese manufacturers calling on them to supply more domestically produced goods.

What has been the outcome of shifting production to overseas sites? One result has been to allow manufacturers to reap the benefits of the strong yen, increasing their profits by producing goods offshore and importing them back to Japan. For Japanese corporations, accustomed to struggling to cope with a strong currency, this is an unusual situation. But they can end up losing sight of fundamental considerations if they focus so much on this that they end up adopting the short-sighted view that utilizing overseas production plants always works out for the best.

So what fundamental considerations do corporations need to bear in mind? One important point at present is for Japan to forge a win-win economic relationship with emerging countries while finding ways to secure appropriate returns for itself. In this article, I will examine the business models of winning corporations in today’s business world, with a focus on learning from their approach to working with emerging countries.

Leading Technologically but Losing at Business

The global situation is changing rapidly. With the swift advance of economic globalization, there is strong demand for industries, corporations, and businesses to enhance their competitive power and for them to pursue innovation so as to create new value for society using science and technology. In addition, the shortening of the product cycle has sped up the pace of technological development and increased the sophistication and complexity of technologies. Meanwhile, markets have become even more enormous than before, and the international division of labor has progressed rapidly as new countries reach the emerging stage and those that emerged earlier become more advanced.

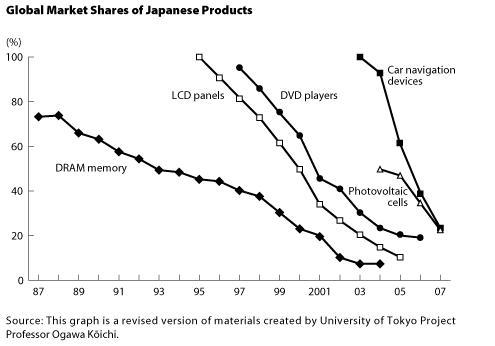

Unfortunately, however, numerous cases have occurred in which Japan has lost out on the business end despite leading the way technologically. My colleague at the University of Tokyo, Project Professor Ogawa Kōichi, created a graph to illustrate the situation; I attach a slightly revised version.

Japan’s market share has declined rapidly in the case of products for which it boasts outstanding technologies, such as semiconductors, liquid crystal panels, DVD players, and car navigation devices. I have been keeping a close eye on the electronics market these past 10 years in my capacity as the head of an effort to redevelop the Akihabara district and have been astonished at how quickly Japanese products have vanished from the marketplace–as is clear from the graph.

What we see is that when Japanese companies commercialize products after working hard on research and development, they start out in full command of the market, but a few years later their share slips to the single-digit level.

However, two explanatory notes should be made regarding the graph. First, underlying the downward movement on the graph is the existence of an upward movement in terms of the worldwide spread of the same products. That is to say, when a given global market was largely limited to certain industrialized nations, Japanese products dominated, but as the market rapidly expanded to include industrialized countries in general and emerging countries, then these Japanese products began to rapidly lose their relative market share. The second point to note is that downward lines become steeper the closer we get to the present; this attests to the accelerating speed at which a global market can get up and running. In other words, a clear transformation occurred between the expansion of the market during the analog era among the Group of Seven countries, with a population totaling 1 billion people, and the expansion during the digital era among the Group of 20 countries, which have 3 billion people. Moreover, the increasingly rapid pace at which Japan is losing its global market share clearly points to the fact that leading overseas companies are learning what it takes to defeat their Japanese counterparts. In many cases, this is the result of joint innovation-oriented efforts undertaken by winning corporations in Western countries and their partners in emerging nations, which have been squeezing Japan from both sides.

Learning from Intel

How is it that the situation has reached this point? The classic example we can look to is the semiconductor business of Intel Corporation. Over the past 20 years, Intel has managed to maintain a market share of over 80% for the microprocessor units (MPUs) installed in personal computers and other devices, and its gross profit margin is also said to be in excess of 40%. At the core of this winning corporation’s business strategy is the innovation-oriented win-win relationships it has formed with emerging nations during the second phase of its market expansion.

Personal computers were once integral products That is to say, these computers–unlike modular products–could not be easily produced by assembling parts, as is the case today, but required the integration of individual parts. Initially, companies that manufactured finished computers, such as NEC and Fujitsu, would use their high technical prowess to create products by integrating parts. In this sense, the market leaders at the time were the manufacturers of finished goods.

Given this situation, Intel, which was a parts supplier at the time, realized that if it hoped to not end up as a mere subcontractor to manufacturers of finished goods, it would have to create a system making its own products crucial to the finished products. The practical manifestation of Intel’s strategy in the area of personal computers, as is well known, was its alliance with Microsoft. The two companies created the key components for PCs, with Intel handling the MPUs for the hardware and Microsoft creating the software operating system, Windows. Other parts manufacturers and software developers then had to make their own offerings compatible with these key components. Through the two companies’ alliance, PCs became dependent on them and they gained control of the market.

Intel’s MPU chip was turned into a sort of “black box” containing the key components of a PC; at the same time the company made its protocol for connectivity to external components available to other companies as an international standard. The Intel approach, in other words, was to create a black box internally using its own technology, while externally offering open access to standard technologies. This transformed the personal computer from an integral product into a modular product.

Other parts makers ended up adjusting their own interface to be laterally compatible with Intel. By the time that manufacturers of finished PCs realized what was going on, nearly all parts makers were taking their marching orders from “Wintel,” as the Microsoft (Windows) and Intel tandem came to be known.

The next step for Intel was to gain a firm understanding of market formation in terms of how to greatly expand the market for PCs requiring Intel parts. The key was for PC production itself to remain simple and convenient, no matter how sophisticated MPUs became. Intel accomplished this by developing an intermediary part called the motherboard. It became possible to easily assemble a finished PC by inserting a motherboard equipped with the MPU. The development of the motherboard helped greatly facilitate PC production. According to the conventional logic of the time, the creation of the motherboard could have been a means for Intel to transform itself into a manufacturer of finished goods. However, in the early 1990s, Intel made the surprise move of providing know-how on motherboard production to companies in the emerging economy of Taiwan. The companies that received the know-how then inexpensively mass-produced the motherboard. This bold strategy laid the groundwork for Intel’s MPUs–a key component for PCs–to come into wide use.

This resulted in the subsequent supply chain automatically getting under way. Manufacturers who assembled PCs using the motherboard appeared one after another. These included, most prominently, Dell and its up-and-coming Taiwan-based rival Acer, which is one of the companies to which Intel initially outsourced motherboard production.

The Intel MPU is selling extremely well now that the PC market has expanded to include not only advanced countries but emerging ones as well. Intel focused on a key aspect, while letting other companies (particularly those in emerging countries) handle the remaining tasks, with the result being that a market was rapidly formed in an automatic way. And the profits flowed back to Intel. It would be hard to imagine a more brilliant business model.

This is an insider model, where the finished products are subordinate to the key components. It is also a pioneering model of a Western corporation utilizing emerging nations to aim for innovation through a joint effort with corporations in those countries. Later I will also discuss the outsider model used by Apple to counter Sony and Panasonic, which involves the technique of relying heavily on the emerging country of China as a production base.

Ever since corporations began to follow the model of using emerging nations, the once-proud product lineups of Japanese corporations have quickly lost their competitive edge and fallen behind those of their global competitors.

Innovation-based Competitiveness

As is clear from the classic example of Intel, the reason that Japanese products are losing out is not because Japan’s technologies are lagging behind the global level. Rather, it is the result of lagging behind Western corporations when it comes to developing know-how on the best ways to utilize technologies. Japanese corporations trail their Western counterparts with regard to devising a business model and then coming up with the product/service architecture and the management of intellectual property and standards to bring the model to fruition; they also lag in terms of fostering relations with emerging countries.

The issue comes down to the change that has occurred in the competitive model. There has been a shift from the previous improvement model of fine-tuning the existing approach that was the source of competitiveness, to an innovation model aimed at replacing the existing model with a new model that generates social value and then encouraging it to take root. We have, in other words, arrived at what might be called the “pro-innovation” age.

For Japanese manufacturers, the shift toward innovation becoming the source of competitive strength has been a terrible change in the corporate environment because they had maintained their edge by making steady, incremental improvements over time. Particularly in the automobile industry, where kaizen (improvement) has been the byword, the creation of the new electric-vehicle model–replacing the gasoline engines that have powered cars for over a century–is calling into question the foundation of the industry’s competitive strength.

We are no longer in the era when innovation was synonymous with invention, meaning that a company could succeed through technical prowess alone. These days it takes more than just technical innovation to cultivate a competitive advantage. Companies also need to have a business model for using the technique of teaming up with emerging countries–as well as the product architecture and management of intellectual property and standards to make the model possible.

The Business Model Is the Key

Despite this new reality, more than a few managers and top executives of Japanese manufacturing companies would be at a loss if asked what their companies are doing to turn their technological strengths into business strengths–in other words, what their company’s fundamental business model is. These corporate leaders are not hesitant to answer out of concern to guard their secrets. Rather, up to now they simply have had almost no awareness of business models at all. One cannot help wondering if this means that numerous companies in various industries lack any business model apart from the stale notion that a business will succeed as long as it stays out in front technologically.

Japanese business leaders are also likely to flash a look of bewilderment if asked to voice an opinion on what sort of product/service architecture is optimal when incorporating their technologies into products. It is a question they cannot understand because they have never pondered it before and it is quite alien to their mind-set. The reaction to such questions among Japanese executives basically shows how out of touch most are to the issue of how to manage value formation.

Many conversations with these business leaders freeze up if one asks whether they think it sufficient to just firm up patents on technologies and how they would propose to utilize international standards to their own benefit. In my view, this reaction among Japanese business leaders attests to how their ideas on managing property rights and standards lag 20 years behind those of their overseas counterparts.

If this backward response continues, I cannot help feeling a fundamental sense of crisis about Japanese industry. I say this because Japanese corporations have not demonstrated the type of ingenuity needed to move beyond the level of a business model focused on succeeding through gaining a technological edge or reducing costs.

Electronics Industry’s Innovative Business Model

In the electronics industry, there have been some remarkable ups and downs. As I noted earlier, Japan’s presence is on the wane in industries where it formerly commanded a considerable share of the global market, including areas ranging from semiconductors to consumer electronics that had once been the country’s mainstay products. Moreover, many of its machinery industries also rapidly lost their competitive edge as a result of advances in information technology and mechatronics. Even the automobile industry, which has driven Japanese manufacturing, faces doubts about its competitive prowess now that the age of electric cars is arriving. In short, the digitization of product technologies has led Japanese industry to quickly lose its competitiveness in one area after another.

The rapid transformation of the electronics industry was brought about by the creation of new business models and innovation that stem from the opportunities provided by the digital revolution. The winning corporations that emerged out of this situation were those that could bring together their knowledge in a business model that optimized their own technological strengths. The classic example is the insider model of Intel, which I touched on earlier.

Among the many business models to be seen, another example we can look to is Apple’s outsider model. In contrast to the insider model, Apple’s approach has been to create an overall system of value formation composed of multiple layers of products and services. For example, Apple’s iPod was the focus of attention for its cool concept, backed up by the company’s great brand power, and its interface design, which realized the concept in such a way as to draw optimally on the user experience. But the real key to success was that Apple linked such products as the iPod and iPhone to content sold at its iTunes Store. The triumph of the business model, in other words, was based on synergistic value-creation management between products and services. Underlying Apple’s achievement is of course its extensive management of intellectual properties, including the standardization that makes the business model possible. Also, even though Apple produces most of its flagship products on its own, it has outside manufacturers handle most of the peripheral parts, driving a hard bargain when it comes to parts prices, and its production control system effectively utilizes manufacturing plants in China. However, not many people are aware that even though Apple has over 10,000 applications that are created by third parties, it employs a carrot-and-stick approach of providing them with low-priced development kits while at the same time reining them in with a tight contract so they do Apple’s bidding.

The Risk of the “Seeds” Approach to Development

What about the situation in a sector like the chemical industry, which at first glance seems completely unlike the electronics industry? Up to now, most of the functional materials in the chemical industry have not followed a model that starts with a need, as is done in the area of pharmaceuticals where certain illnesses are targeted and effective drugs then developed to treat them. Rather, the starting point has been what might be called a seed. That is to say, first a substance with effective properties is discovered or developed, and this is followed by the search for its applications. Research that is unrelated to any specific market need is carried out and applications are later developed for whatever unique materials or material properties are discovered through the research.

The business strategies pertaining to these functional materials can be broadly divided into three categories. The first strategy is for a business to leverage its scale to come out on top. For existing fields, and general-purpose materials in particular (including numerous types of monomers as well as fundamental polymers), competition centers on keeping costs low. This means that merits of scale are the key factor. Because everything centers on how to provide mass quantities of high-quality items that are produced in an inexpensive, safe, and stable manner, there is no getting around the need for mega-manufacturers to be involved. Japanese corporations find it difficult to succeed on the basis of this strategy. In the case of general products, instead of competing with each other on their own initiative, chemical companies find themselves being made to compete by their customers. They need to display ingenuity in figuring out how to get away from the business model under which they are merely suppliers. The question centers on whether a transformation can be made to an insider model where development of high-value key materials is pushed forward so that finished products become dependent on these materials. Otherwise, there is no alternative but to continue on with the physical war of attrition against corporations in emerging countries, as is the case for the parts suppliers that perform work on an outsourcing basis in the outsider model.

The second business strategy is the “one of a kind” approach that draws on the factor of uniqueness. This requires creating high-performance materials that are distinct from those of one’s competitors, particularly the development of unique functions that can be used in new fields. The field of functional materials is one where basically there are just a few patents for each product. This means that if unique materials are developed, patents on them can be obtained to keep competitors out and form a market in which one’s own business enjoys a monopoly.

In implementing this approach, it becomes important to penetrate the upper-layer products, which are those parts that utilize the materials in question. One might seek to conduct joint research with a corporation likely to bring about innovation in order to develop materials indispensable to next-generation products, thereby gaining full or partial control over the materials thus procured. One example of this approach is how a highly functional seasoning developed by a well-known Japanese food company was essential for one part of Intel’s MPU. Not that many people are familiar with this example, which illustrates the approach aimed at developing sophisticated materials essential to successful components and then having other companies use those materials.

It is worth noting, meanwhile, that there is a Japanese corporation that has developed a brilliant business model for the area of functional materials. I am referring to Mitsubishi Chemical Corporation, which managed to gain control of the market for one type of DVD media through its Azo dye. The corporation developed the dye on the basis of its own dyeing technologies, and its outstanding durability and resistance to light made it possible to increase DVD capacity. Mitsubishi Chemical gained a monopoly over the technology by patenting it, but that alone was not sufficient to form a market for the new type of DVD. This was done when Mitsubishi Chemical succeeded in its effort to make the DVD media premised on the Azo dye the international standard for the write format. This meant that companies wishing to produce the DVD media in accordance with the standard would naturally have to use the Azo dye. Initially, there was even a rumor that the dye was temporarily trading at a higher price than gold. And Mitsubishi Chemical made other strategic moves, such as providing its know-how on manufacturing DVD media to a Taiwanese manufacturer. As a result of these moves, the DVDs became available at an affordable price, leading to the rapid expansion of the market. Naturally this led to a rapid increase in sales of Azo dye. Here we can see another example of a business model in action that makes use of emerging nations, like the case of Intel providing manufacturing know-how on its motherboard to Taiwanese makers to rapidly expand the PC market.

Meanwhile, Mitsubishi Chemical’s subsidiary, Mitsubishi Chemicals Media, launched its own brand-name DVDs. The aim is to form a high-value-added sector of the market through the brand-name product at the same time as expanding the market through affordably priced products. The approach has resulted in Mitsubishi Chemical’s global share of the functional dye market accounting for as much as 70% of the roughly two billion recordable DVD media produced in 2005.

Mitsubishi Chemical is currently competing with Fuji Film in the same market and has apparently updated its business model a total of seven times. There is no space here to deal with all those developments, but it is worth noting that the company has adopted a strategy that tries to squeeze out the maximum benefit by implementing a string of different business models for a single product. The crux is how much ingenuity manufacturers can bring to developing business models centered on the multiple development and enjoyment of value from a single technology.

However, a corporate strategy aimed at being “one of a kind” will not work if other companies develop alternatives to the products that set the company apart. So what should be done?

The answer is the third strategy, which involves getting away from the materials-based strategy. That is, instead of looking to succeed only through the materials developed, the aim should be to ingeniously chart a course for having materials used in parts, thereby fashioning a business model for taking the lead in the area of mainstay parts, leveraged by key materials.

The fundamental element is the management of value creation originating with customer value. This involves, first of all, making progress in the realm of component materials and parts by bringing sophisticated materials into relation with each other. One example is to combine sophisticated materials with a high-density coating in a highly functional film shape. The next step is to create semi-manufactured goods from the component materials or parts. Ideally this would involve the formation of a product architecture that is integral on the inside and modular on the outside, with the key being to create the platform that is the core of the subsequent finished product. That is the way to secure continuity. Furthermore, an even larger market can be formed if a “full turnkey solution” is put in place that makes use of the component materials and a more advantageous division of labor with emerging countries is also put in place.

There is also a possibility for the creation of strategies at a variety of different levels, including creating products by bringing together original and modified materials, developing material delivery systems (such as the drug-delivery system for pharmaceuticals), and carrying out on-site operations. In all of these cases, the combination and integration of main value formation and additional value formation is the means of forming value.

Learning from Leading Industries

In all sorts of industries, the conventional business model of linking technologies to business is becoming obsolete. The electronics industry has been at the forefront of bringing about a transformation and diversification of business models. Other industries followed in turn, using the transformed and diversified business models pioneered in the electronics industry as a model. The wave of change is not limited to machinery. Business models are now changing and becoming more diverse in various fields, including not only the chemical industry but also the fields of medicine and food products. Failure awaits not only those who do not adapt to the changing business models but also those who do not manage to anticipate where changes are headed. My hope for Japan is that it can gain the know-how on how to best use its technical know-how, which involves developing its knowledge of upper-level business models.

Meanwhile, it is important to figure out how to create a win-win partnership for innovation with emerging countries. Of course, that alone is insufficient. Emerging countries can be viewed as a source of human resources or mineral resources, as well as potential markets. One area in particular in emerging countries that has rapidly been gaining attention is the infrastructure business, where many business deals can be obtained in the public sector for social infrastructure projects, such as highways, nuclear power plants, water and sewage facilities, and telecommunication networks. These are the sorts of projects that economically advanced countries always have to undertake through a partnership between the private and public sectors. However, this is a subject that I will have to deal with on a separate occasion.

In any event, the global economy is no longer on the 1-billion-person scale of the G7 era. The focus now in the G20 era must be on a global economy with a combined population of 3 billion people. In addition, it will be necessary to pay attention to the less developed countries at the “base of the pyramid.”

Japanese industry will need to discard the old concepts based on its experience moving from the domestic to the overseas market and switch to an approach that is focused instead on coming up with business strategies that start from a global perspective.

Translated from an original article in Japanese written for Japan Echo Web. [March 2011]

Related posts:

WHY UNIVERSITY GRADUATES SHOULD CONSIDER APPLYING TO SMES

A CONTRARIAN VIEW OF YOUNG PEOPLE TODAY

TPP MAY SPARK JAPANESE POLITICAL RESTRUCTURING

RESTORING JAPANESE-STYLE MANAGEMENT'S RUDDER

WHY UNIVERSITY GRADUATES SHOULD CONSIDER APPLYING TO SMES

A CONTRARIAN VIEW OF YOUNG PEOPLE TODAY

TPP MAY SPARK JAPANESE POLITICAL RESTRUCTURING

RESTORING JAPANESE-STYLE MANAGEMENT'S RUDDER

Control of social security expenses should be expedited.Ensuring Escape from the Deflationary Spiral and to Again Increase Consumption Tax― Outlook of the primary balance of the central and local governments― Case where consumption tax rate was raised to 10% as originally planned

Control of social security expenses should be expedited.Ensuring Escape from the Deflationary Spiral and to Again Increase Consumption Tax― Outlook of the primary balance of the central and local governments― Case where consumption tax rate was raised to 10% as originally planned