Will Fiscal Reconstruction Advance?

Ⅰ. Introduction

Prof. Sato Motohiro

The Japanese government raised the consumption tax rate to 10% in October 2019. Many people have criticized such tax increases, citing them as a cause of an economic downturn. However, the tax hike resulted from an increase in social security expenses associated with the aging of the Japanese population. Another source of revenue would have been sought or the control of benefits would have been requested if the consumption tax was not picked as a solution. In fact, social security benefits will expand from the current level of 120 trillion yen (the figure for fiscal 2018) to 190 trillion yen in fiscal 2040, according to a trial calculation performed by the Cabinet Office. Such an increase in social security expenses is due to the structural problem in twenty-first-century Japan called aging. It will not be all right when the economy picks up.

Consequently, we must ask how to guarantee the sustainability of social security and public finances. Further fiscal reconstruction is sought for that reason. The government adopted the achievement of a surplus in the primary balance (balance of payments by the central and local governments) by fiscal 2025 as a goal in its new plan for achieving fiscal health. As interim indicators for the progress of the plan, the government adopted the lower end of the 180% range for the ratio of outstanding debts to gross domestic product (GDP) and 3% or less for the ratio of fiscal deficits to GDP in fiscal 2021. However, we cannot be optimistic about the prospect for achieving fiscal consolidation. According to “Economic and Fiscal Projections for Medium to Long Term Analysis” released by the Cabinet Office on January 30, 2019, a deficit of 2.3 trillion yen (equivalent to 0.4% of GDP) will remain in fiscal 2025 even in a case where high economic growth (at a real growth rate of 3%) is achieved. In a more realistic baseline case (assuming a real growth rate of about 1%), the deficit will amount to 1.2% of GDP in fiscal 2025. The Fiscal System Council stated, “Additional measures must be examined from the perspectives of both annual expenditures and annual revenues as needed in order to inspect the progress of reform initiatives and guarantee target achievement […], in addition to concentrating and accelerating such initiatives over a three-year period through fiscal 2021.” Those additional measures may include a consumption tax increase. Working to economize benefits is a matter of course. A revenue source will also need to be enhanced. The consumption tax rate will not remain at 10%. The Japan Association of Corporate Executives has proposed 17% as the consumption tax rate. Likewise, the International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development (OECD) have asked the government to raise the consumption tax rate to a level above 10%. This article considers how Japan should reconstruct public finances and where the issues occur.

Ⅱ. What should be done to secure a revenue source for social security?

Revenue sources for social security are broadly divided into (1) consumption tax and (2) social insurance premiums. Insurance premiums account for about 70 trillion yen of social security benefits that currently total approximately 120 trillion yen. Consumption tax covers the remaining benefits of 50 trillion yen. Unlike consumption tax, the burdens of social insurance premiums are not shared widely among different generations as existing conditions, but concentrated on working households. There are lump-sum portions in premiums for the National Pension and the National Health Insurance. Therefore, the National Pension and the National Health Insurance impose heavy burdens on people in the low income bracket. They are regressive. Furthermore, social insurance premiums paid by companies, such as premiums for the Employees’ Pension Insurance and the Employee Health Insurance, work like taxation on regular employees and thus undermine employment. They may promote the expansion of non-regular employment as a replacement for regular employment.

On the other hand, consumption tax has a high funding capacity. It stabilizes tax revenues and makes them less susceptible to economic trends and changes in the demographic structure. As a matter of course, consumption tax imposes heavy burdens on people in the low income bracket as a regressive tax. It can cause an economic downturn and push the economy back into a period of deflation. Many people criticize consumption tax for those reasons. However, from an economic perspective, consumption tax causes small distortions in economic activities compared with social insurance premiums for the following reasons. Consumption tax is a multiple-stage tax on distribution transactions imposed in the stages of processing, production, wholesaling and retailing, respectively. There is a system called input tax credit for preventing the accumulation of consumption tax that arises from such business-to-business transactions. Taxable business operators can deduct consumption tax paid for purchasing raw materials and the like from consumption tax imposed on their sales. Accordingly, burdens produced by consumption tax do not accumulate in the production process. Capital investment by companies does not obstruct this system, because the investment is treated as immediately deductible. Consumers bear consumption tax because they are not taxable business operators (they are ineligible for input tax credit).

Furthermore, consumption tax is neutral in the international competitiveness of domestic companies, because the imposition depends on the destination. Imports fall under the scope of taxation while a zero tax rate is applied to exports. Japanese consumption tax does not affect exporters in Japan competing in overseas markets. Taxable companies in Japan whose businesses are in competition with imports also do not suffer competitive disadvantages, because the consumption tax is imposed on imports as well. In contrast, corporate income tax based on income sources and social insurance premiums (corresponding to the substantial taxation of personnel expenses) impair competitiveness against products from low-tax countries, because they increase production cost for companies in Japan. In this way, the advantage of destination-based taxation is rising in the global economy where people, goods and money move across national borders. Controlling corporate income tax and social insurance premiums and replacing them with consumption tax (value-added tax) has been a trend for tax system reform in Europe.

However, people in Japan tend to think consumption tax adversely affects the economy based on their experiences during the previous consumption tax hike. Reader, draw a line between short-term business conditions and medium- and long-term growth at this point. Short-term business conditions are susceptible to macroeconomic demand, such as consumption. An increase in the consumption tax rate affects them. Meanwhile, the supply side determines medium- and long-term growth. Structural reforms and the like, such as work-style reforms and regulation reviews, are aimed at improving productivity on the supply side. Consumption tax does not impair this supply-side productivity. It shows a high affinity for economic growth.

The previous tax system, heavily reliant on corporate income tax and social insurance premiums, assumed growth in the population of the working generations that support social security and high economic growth. Meanwhile, new economic conditions, such as the aging of the society and globalization of the economy demand the construction of a new tax system with consumption tax at its center. However, citizens and politicians tend to dislike consumption tax. A great sense of burden created by the tax included in prices must be one of the reasons for that tendency. It should be noted that consciousness of such a burden motivates citizens to pay attention to use of the tax and thus discipline their government. Tacit collusion has traditionally existed between citizens, politicians and bureaucrats. The latter has been allowed to keep public finances inefficient (wasteful) while the former has avoided tax raises. A consumption tax increase may be able to positively change the relationships between citizens, politicians and bureaucrats.

III. Outlandish schemes preventing fiscal reconstruction

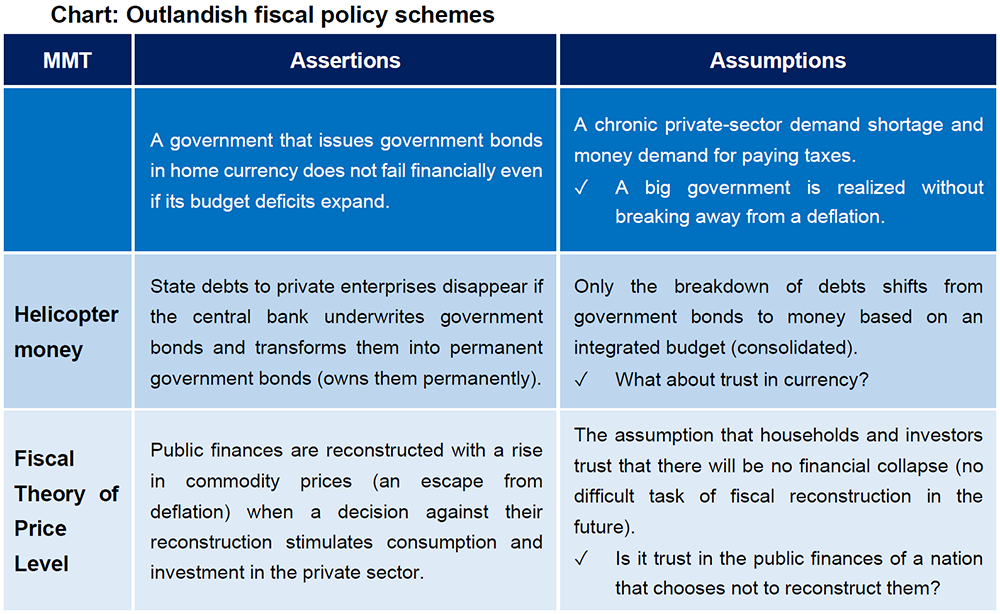

Right or wrong, rather than a method (tax increase or expenditure control), has been questioned regarding fiscal reconstruction. The assertion is that fiscal reconstruction in a way that involves pain is unnecessary. Expectation for growth, known as Domar’s condition, is one such view. According to this theorem, the primary balance needed for stably controlling the ratio of outstanding public debts to GDP depends on the difference between a growth rate and an interest rate. This condition results from a rise in the numerator called outstanding public debts in proportion to the interest level (additional debts in the case of a deficit) and a primary balance and an increase in a denominator called GDP in proportion to the growth rate. The sustainability of public finances is guaranteed in the sense that the ratio of outstanding public debts to GDP does not diverge (debts do not continue expanding beyond the size of the economy) even if the primary balance remains in the red in cases where a growth rate is high compared with an interest rate. Accordingly, expansionary fiscal policy advocates say that public finances are sustainable with a deficit left from raising a growth rate with a large-scale fiscal stimulus while monetary easing of unprecedented dimensions keeps interest rates low. However, things do not go according to plan. Companies will expand capital investment if business conditions improve. Interest rates will start rising when state and corporate capital requirements expand. According to the trial calculation by the Cabinet Office, interest rates (0% on the whole in the most recent quarter) will approach the growth rate (2.4% in the most recent quarter) in the medium and long term. It is impossible to indefinitely resist a market mechanism (upward pressures on interest rates) by artificially maintaining low interest rates through a restrictive monetary policy. According to Domar’s condition, public finances are unsustainable unless a primary balance surplus is achieved under the circumstances.

Meanwhile, the so-called Sims theory (the Fiscal Theory of Price Level) says fiscal reconstruction is feasible with inflation in place of growth. Long-term fiscal spending by the government equals the sum of the real value of public debts outstanding at present (the nominal amount divided by the price level) and the current value of a primary balance surplus and in the future viewed in real terms, assuming that public finances do not collapse (default of public debts does not occur). Using household finances as an example, the condition corresponds to the general equivalence of lifetime consumption and lifetime income. Accounts do not balance unless inflation reduces the real value of outstanding public debts, provided that the government chooses not to improve a primary balance under this condition. Consequently, a breakaway from deflation and debt compression is realized simultaneously. This is a considerably convenient scenario. Expectation holds the key to the scenario. Consumption expands when households anticipate that there will be no financial reconstruction for some time; in other words, there will be no tax increase in the future. The expansion of macroeconomic demand becomes a major cause of a commodity price increase. However, households may develop different expectations. Fiscal deterioration may increase anxiety about the future. Interest rates will rise steeply by taking the risk of default into consideration if trust in public finances declines. Increasing interest payments will accelerate fiscal deterioration as a result. Sims theory excludes those possibilities with assumptions, instead of results.

Expectations are also rising for helicopter money. In this concept, state debts are written off when the central bank underwrites government bonds. However, no such magic appears to exist. This should be obvious when we consolidate balance sheets for the state (equivalent to a parent company) and the central bank (equivalent to a subsidiary). Government bonds held by the Bank of Japan (BOJ) do not appear in consolidated balance sheets because they are offset by state debts. Some helicopter money advocates assert that this is proof that the government’s debts disappear, and fiscal reconstruction is achieved if the BOJ buys all government bonds. However, a reserve deposit the central bank is obliged to pay to private banks (the BOJ’s current account) and banknotes in circulation appear in consolidated balance sheets as liabilities. Normally, a reserve deposit bears no interest with the exception of special cases. At present, negative interest rates are imposed on some of the reserve deposits substantially in excess of legal reserves (excess reserves). The BOJ will be forced to pay positive interest for a credit squeeze when monetary easing comes to an end. In other words, the interpretation that excess reserve deposits (bearing interests) simply replaced national debts becomes possible. The central bank may try to maintain artificially low interest rates on reserve deposits by abandoning the stability of commodity prices and implementing monetary controls stated above. However, it will be difficult for the central bank to resist global market pressures (fund transfers across national borders) for a long time. The consolidated government will be asked to pay interest by amending laws and achieving a primary balance surplus if the BOJ is unable to pay interest with seigniorage of its own. Inflation will impose burdens on asset holders unless the consolidated government takes that step. In any case, there will be burdens for citizens.

Modern Monetary Theory (MMT) has been popular since the beginning of this year. MMT has drawn attention because its chief advocate, Professor Stephanie Kelton of the State University of New York at Stony Brook, served as an advisor to Senator Bernie Sanders, who took the 2016 Democratic nomination for president by storm. The idea that there is no need for government authorities to put currency into circulation and issue government bonds to consider budget deficits and outstanding debts in fiscal policies (or try to reconstruct public finances) lies at the heart of this theory. In short, the government faces no financial restrictions. If anything, it is desirable for the government to specialize in economic policies for achieving and maintaining full employment. The government can cover its debts by putting currency into circulation (performing so-called debt monetization) in conjunction with the central bank.

Japan is cited as a practical MMT example because the BOJ has kept buying a large amount of government bonds by continuing unprecedented monetary easing under Governor Haruhiko Kuroda. However, there is a large difference between monetary policies assumed in the MMT and monetary easing measures taken by the BOJ. The BOJ adopts 2% as its target for a commodity price increase. It positions government bond purchases as a way to achieve that target. The BOJ aims to appeal to people’s inflation expectations (expectations for a future rise in commodity prices) by increasing the money supply (monetary base) in exchange for government bond purchases. Monetary easing will come to an end when the inflation target is achieved. On the other hand, MMT sets no such target or exit for the central bank. The central bank just plays the role of covering budget deficits produced by the government continuously. In that sense, monetary policies are subordinate to public finances. The independence of the central bank is also lost.

Mainstream economists agree on public spending with budgets in deficit as a way to manage demand under exceptional conditions, such as the depression in the wake of the Lehman collapse, where macroeconomic demand for consumption, investment and the like is insufficient. Private companies tend to keep investment down during serious deflation. Households control consumption and save income for reasons including anxiety about the future. In other words, the condition of a surplus fund (lenders exceeding borrowers in number) arises in the private sector as a whole. In that case, interest rates do not climb even if government bonds are additionally issued. If anything, their issuance leads to a virtuous circle through which government expenditures generate new employment and income, and the generated employment and income cause private-sector demand including demand for consumption and investment to recover. However, maintaining huge budget deficits under ordinary circumstances involves the risks of an interest rate increase and inflation. Therefore, many economists criticize MMT, saying it does not serve as a guide for economic policies under ordinary circumstances. As a matter of fact, MMT does not deny inflation attributable to budget deficits. However, that position is not based on the view of the quantity theory of money addressed by the monetarist. Instead, MMT adopts the view that relationships between budget deficits and a monetary surplus (surplus funds) in the private sector at the point of full employment determines the presence or absence of an inflation. Furthermore, MMT assumes that public finances can be flexibly retrenched once an inflation occurs. A resolution by the national assembly is required for deciding the fiscal policy (as long as financial democracy is adopted). Yet, the degree of flexibility will be less than that assumed in MMT. The assertion that public finances can be reconstructed without a tax increase is also held by the Ageshio-ha (the rising tide school of economists). However, Ageshio-ha economists bear in mind the achievement of high economic growth led by the private sector, natural growth in tax revenues, and the elimination of budget deficits (the balancing of fiscal revenue and expenditures) as the result of achieving an exit from deflation. High growth is not expected in MMT.

MMT is not a prescription for escaping from deflation. Pay attention to the MMT assumption of a chronic demand shortage (monetary surplus in the private sector). It is not the role of markets but the role of the government to achieve full employment under that condition. For that purpose, the government continues to absorb money that budget deficits have made useless. The result is big government. In practice, demand shortage (a deflationary gap) has started to disappear. The problem has shifted to a manpower shortage. Start-up companies are facing financial difficulties. Personnel and funds for dealing with innovations and the like will run short if the public sector keeps absorbing manpower and funds. Such a trend can end up stagnating the economy. In addition, money swollen as a result of debt monetization does not cause inflation because people hoard money for reasons including preparation for future tax payments. (It is paradoxical, but the government does not need to care about fiscal revenues and expenditures in MMT, because it can increase taxes whenever it wants.) Such money kept as deposits will go toward consumption (goods), provided that no tax is imposed in the future. Inflation may accelerate if too much money is spent compared with the volume of goods. To be sure, what MMT asserts looks attractive at a glance. There is no need for fiscal reconstruction that involves pain. The government can upgrade social security and increase public works spending without such fiscal reconstruction. Benefits from the expenditures are similar to a free lunch in the sense that they cost people nothing. However, what MMT calls a free lunch depends on suspicious assumptions, including (1) a chronic demand shortage and (2) money kept under the mattress for paying taxes.

There is deep-rooted support for this MMT among liberals in the United States. Distrust of a market economy due to causes including the widening income gap lies in its background. A reaction to fiscal tightening in the wake of a financial crisis is another aspect found in Europe. In Japan, outlandish schemes not limited to MMT that assert no need for fiscal reconstruction involving pains, such as helicopter money theory and Sims theory (the Fiscal Theory of Price Level) mentioned above, have circulated. All of those schemes have theoretical and ideological backgrounds that are different from MMT. However, they might have been lionized because any reason is considered to be acceptable as long as it makes the difficult task of fiscal reconstruction, including a consumption tax increase, unnecessary. All of those outlandish schemes lack conviction in their correctness. The author thinks they might be partially based on the wish for them to be correct. The danger is that assertions that are easy to understand or pleasant to the ear are not necessarily correct.

Ⅳ. Will things work out eventually?

In the Economic Growth Achieved Case in the trial calculation by the Cabinet Office (released on January 30, 2019), a primary balance deficit of 10.1 trillion yen (equaling 1.7% of GDP) will remain in fiscal 2020. However, the primary balance is forecasted to move into the black in fiscal 2026, backed by firm economic growth (at a real rate of 2%). Furthermore, the ratio of outstanding central and local government debts to GDP is expected to fall from 190% in fiscal 2017 to 156% in fiscal 2028, with an interest rate level predicted to stay below the growth rate for some time. There are several conditions for such forecasts that require attention, though. For example, the productivity growth rate for the economy is assumed to rise from about 0.4% to 1.3% or thereabouts. This corresponds to the rate of increase in the 1980s, when deflation and aging were absent. The women’s participation rate in the labor force is expected to rise gradually until fiscal 2028. The participation rate in the labor force by the elderly is also assumed to sustain an upward trend found in the most recent quarter. The Economic Growth Achieved Case assumes progress in overall labor participation. A high economic growth rate is estimated under the conditions of high productivity and a high labor participation rate. Stated differently, the Case is subject to the success of policies on which the government is working at present, including those for reforming working practices in Japan. On the other hand, in the Baseline Case based on the current potential growth rate, real growth rate will be about 1.1% in the 2020s and primary balance deficit will remain in fiscal 2028 (a deficit of 6.2 trillion yen (equivalent to about 1% of GDP) will remain). The ratio of public debts to GDP will also remain high.

Will optimistic forecasts, such as those in the Economic Growth Achieved Case, dispel citizens’ anxiety about public finances and social security? Will the forecasts stimulate initiatives for reforms aimed at achieving high growth, including the reviews of the so-called bedrock regulations? Many citizens will smell self-aggrandizement by public offices in those forecasts and find them hard to trust. The view that structural reforms involving pain are unnecessary as long as Abenomics succeeds may spread. If anything, reforms necessary for high growth will not advance. The achievement of fiscal health may also take longer. The government has adopted a stable reduction in the ratio of public debts to GDP as a goal together with the achievement of a primary balance surplus. In the trial calculation, the latter will be achieved by the middle of the 2020s at the latest. The assertion that hurrying the achievement of a primary balance surplus is unnecessary is likely to strengthen.

The government intention to do something about the situation may act as a driving force for reforms, provided that the government advances structural reforms, such as deregulation and working style reforms, to achieve growth at a rate of 3%. Meanwhile, the view that things will work out somehow even in the absence of reforms that involve pain will spread if high growth is taken for granted. Such a view will not lead to strengthening the foundation needed for making economic growth and fiscal policies sustainable, a goal adopted in the Basic Policy on Economic and Fiscal Management and Reform 2019. Economic forecasts are not the only cause of the optimistic view that things will work out. In social security improvement pledged in the integrated reforms of social security and tax systems, the government has done something about childcare by postponing the consumption tax hike. The BOJ has also done something about fiscal management (interest payment costs and the like) by buying government bonds in bulk and maintaining close to zero interest on them through its monetary easing measures. Those operations have undeniably given citizens and market players the expectation that things will work out even though state debts surpass 1,000 trillion yen.

A similar situation is occurring for local public utility charges. Many local governments have used general accounts to make up for deficits without raising the charges when higher costs related to the replacement of the water supply and sewerage facilities, their management and the like drove business proceeds into the red. Likewise, they have avoided increasing National Health Insurance premiums with transfers from general accounts when medical expenses grew. In both cases, they have worked things out somehow to avoid burdening residents. It is safe to say that the local governments have given residents the impression that things will work out in spite of the deterioration of the water supply and sewerage facilities and a rise in medical expenses.

As stated above, both the central and local governments have worked things out to keep everyone away from issues in social security and other public services while presenting severe forecasts for public finances. People say that trust has been lost because of political scandals such as Moritomo Gakuen and other problems. However, central and local government officials in Japan may be honest in general. In the United States, some of the federal government offices and tourist facilities, including the Statue of Liberty, reportedly closed in January 2019 due to confrontation between the administration and the Congress that prevented the passage of a federal budget. Their closure was natural because there was no budget. However, the Japanese government might have managed the situation under those circumstances. Such an operation could send out the wrong message that things will work out. Pressure from politicians to expand fiscal expenditures are unlikely to subside if things will work out. The actual conditions of national and local public finances will not reach citizens and residents accurately under that condition. They will not share a sense of crisis. Interest in the condition as a matter of their own concern will not grow. Future forecasts for public finances and the economy require objectivity and caution.

What can the government do? Discussions in favor of establishing independent fiscal institutions for controlling political pressures on budget deficits have picked up steam in Europe since the 2000s. Granting certain political independence to such institutions and giving them responsibilities for (1) preparing economic forecasts as budgetary assumptions, (2) estimating public finances in the medium and long term, and (3) assessing fiscal policies have been assumed in those discussions. The Bureau for Economic Policy Analysis of the Netherlands (CPB established in 1945) and the Congressional Budget Office of the United States (CBO founded in 1974) are well-known independent fiscal institutions with a long history. More institutions have been established in recent years. They include the Office for Budget Responsibility of Britain (OBR set up in 2010), the Swedish Fiscal Policy Council (founded in 2007), the Parliamentary Budget Officer of Canada (established in 2008) and the Irish Fiscal Advisory Council (instituted in 2011). All of those agencies play the roles described above. Among the members of the OECD, including Japan, more than twenty countries had established an independent fiscal institution as of 2014, which grew in number four times since 2000. For that reason, the OECD recently published the Recommendation on Principles for Independent Fiscal Institutions. However, no independent fiscal institution exists in Japan at present, and one is strongly expected.

Ⅴ. EBPM as infrastructure for fiscal reconstruction

In the following section, the author would like to take up evidence-based policymaking (EBPM) and cost consciousness as the infrastructure for fiscal reconstruction. Momentum for EBPM is growing within the central and local governments. There has been a traditional tendency to attach importance to local cases and experiences (episodes) in formulating policies. There are many policies and undertakings whose reviews do not advance despite the time elapsed from their launch and changes occurred in economic and social conditions because they have continued as customary practices. On the other hand, EBPM corresponds to initiatives for clarifying a basic policy framework based on evidence (a definition by the Ministry of Internal Affairs and Communications), including those for (1) making policy goals clear and (2) identifying administrative measures truly effective for the goals. EBPM attaches importance to quantitative and objective data and policy formulation based on their analysis. The Final Report of the Statistics Reform Promotion Council published in May 2017 states the government is expected to effectively apply limited resources and develop administration to gain the greater trust of citizens in the context of rapid changes in the Japanese economic and social structures. To that end, the government will implement EBPM through the three arrows of administrative program reviews, policy assessment, and the inspection and assessment of plans for restoring the economy and public finances, according to an announcement by the Headquarters for the Promotion of Administrative Reform made in January 2018. The government has stated that it will promote EBPM and statistical reforms in an integrated manner. According to the Basic Policy on Economic and Fiscal Management and Reform 2017, the government will promote the improvement of economic statistics and the reconstruction and reuse of statistical systems from the viewpoint of users, in addition to advancing the practice of EBPM and building systems for promoting EBPM through its initiatives in functions for reviewing the stages of policies, measures and administration, respectively.

Visualization of interregional differences is an example of initiatives linked to EBPM. It is natural for interregional differences reflecting different local demand like aging and the industrial structure to exist. That is a matter of course. However, interregional differences unable to be explained with different demand, including those in medical expenses for the elderly remaining after age-based adjustments and different degrees of outsourcing to the private sector among organizations similar in population size and economic conditions, require examination. Such interregional differences are useful information for local governments and residents, because comparison with other regions offers benchmarks for assessing the results of their initiatives. They serve local governments assessed to compare unfavorably in relative results as opportunities (pressures) for reviewing past policies. They urge local governments to modify behaviors (review policies). Visualization is a driving force for expenditure reforms.

Statistical analysis is necessary for going one step further and measuring the effects of policies quantitatively. Examining simple correlations between policies and results indicators is insufficient. Relations between policies and results indicators may seem to be correlations unless external factors for policies are controlled adequately. For example, inspecting differences in results indicators after dividing a sample population into (1) a group that implemented policies (a treatment group) and (2) a group that did not implement policies (a control group) is useful for understanding policy effects. However, the random division of samples into a treated group and a control group is a condition for correctly inspecting policy effects. Otherwise, performance differences with the control group do not necessarily reflect policy effects. This method is known as a randomized controlled trial (RCT). It is a method for inspecting evidence in the results by trying out health promotions and other pioneering policies before their nationwide introduction. Policies are enforced nationwide if results are demonstrated through this experiment. Otherwise, their nationwide introduction is shelved. In Britain, RCTs have been conducted as part of EBPM in a broad range of fields, including education, medical service and tax collection, since 1997, when the Labour Party led by Tony Blair came to power. Meanwhile, the cases of policy analysis in ways resembling randomized experiments remain few in Japan.

It is difficult to convert the culture of policy formulation in the public sector into an evidence base for questioning the types of information and data essentially related to the clarification of policy goals and the measurement of policy effects. In field sites, policies and projects are enforced based on governing laws. Accordingly, governments tend to enforce them because they are written in laws. The author has participated in administrative program reviews (open process and fall reviews) at the Headquarters for the Promotion of Administrative Reform for many years. Many officials in charge of policies have argued against the outcome of programs pointed out by the author, citing governing laws. However, laws (ordinances in the case of local governments) are originally a means of achieving targets or targeted outcome policies. They should not be treated as goals themselves. The author believes that examinations going back to the aims and goals stipulated in laws and the like, ways of thinking about them and grounds for them are necessary (an opinion the author expressed at a meeting of the Headquarters for the Promotion of Administrative Reform in November 2017).

EBPM can also be a means of communication with citizens. The author thinks that evidence, such as how public facilities have been used, their cost structure, and the effects of policies, administrative work and undertakings will pave the way for the agreement of citizens if the government can present it objectively when reorganizing public facilities, discontinuing subsidies and raising public utility and other charges as part of fiscal reconstruction efforts. EBPM can replace traditional power at work behind the scenes and political dynamics as a driving force for reviewing expenditures.

Ⅵ. Stimulating cost consciousness

Building a consensus for fiscal reconstruction requires the stimulated consciousness of concerned parties (including central government offices, local governments and citizens). Accurate cost information must be disclosed for stimulating cost consciousness, in addition to eliminating deficit covering described above. Accurate costs in this context mean full costs or policy costs (1) on the accrual basis (as in corporate accounting) instead of the traditional cash basis, which are (2) calculated for each administrative work or undertaking, or each public facility. In accrual-based accounting, financial statements show these policy costs. Calculation by policy and business, such as welfare and education, characterizes these costs. Look at public facilities, such as community centers and libraries, for example. Business expenses for those facilities have not included depreciation (which reflects renewal costs). Personnel expenses for the facilities have been rough estimates mixed with those of other sections in many cases. Only salaries paid in the current period have been recorded as personnel expenses. Obligations to pay retirement allowances and the like in the future have not been recognized as costs. Fuel and lighting expenses and administrative expenses may have been totaled for complex facilities, such as those where libraries are integrated with cultural facilities. From the viewpoint of local residents, the genuine full costs of the facilities they use are difficult to grasp. Traditional budgets that take only part of the full costs into consideration may lead to the underestimation of expenses. Gaining the agreement of citizens with such budgets will be difficult even if the governments advance the consolidation and concentration of public facilities. The same goes for water supply and sewerage. Accountability for residents and assemblies is not fulfilled if the governments raise charges due to future investment for renewal without clearly stating depreciation expenses. Correct judgment on points, such as the appropriateness of reviews and continuation, is impossible when inspecting the cost-effectiveness of policies and projects in policy assessment unless full costs, including personnel expenses and depreciation expenses, are recognized policy by policy.

The provision of benefits and services, and related revenue sources must be presented in an integrated manner for formulating policies. A 5% increase in the ratio of consumption tax (from 5% to 10%) was originally supposed to be integrated with the improvement of social security including childcare support, pensions, medical services and nursing care (corresponding to 1% of the tax rate) and the guarantee of its sustainability (corresponding to 4% of the tax rate) in the integrated reforms of social security and tax systems. However, tax increase and social security became separate discussion subjects before long. An upward consumption tax revision to 8% became the reality in April 2014. However, an additional 2% rise in the consumption tax rate was postponed repeatedly. The reviews of how the tax revenue would be used (its application to education) were up for discussion. Only disadvantages for the elderly attracted interest when pension benefits were reduced. People did not show interest in the possibility for a pension contribution increase or the reversal of pension reserve funds to put future benefits at risk if the growth of pension benefits is unrestrained. The following points, (1) a revenue source must be secured with a tax increase if social security services and the like are improved, and (2) service levels must be kept in balance with burdens, or alternatives, such as a social insurance premium increase, must be presented and a political decision must be sought if the avoidance of a tax hike is desired. The fiscal consequences of enforcement or non-enforcement (opportunity costs) should be clarified whether a measure considered for enforcement is the expansion of expenditures or their reduction.

The visualization of costs may not sound great. However, the government cannot advance fiscal reconstruction unless citizens and people at policy sites share a sense of participation. Cost visualization is expected to pave the way for the improvement infrastructure necessary for fiscal reconstruction.

Translated from “Zaisei Saiken wa Susumunoka? (Will Fiscal Reconstruction Advance?),” Ronkyu (research papers, Journal of the Research Bureau of the House of Representatives), No. 16 / December 2019, pp. 1-9. (Courtesy of the Research Bureau of the House of Representatives) [March 2020]

Note: Original article (Japanese only) is available at the website of the Research Bureau of the House of Representatives below.

Keywords

- Sato Motohiro

- Graduate School of Economics

- School of International and Public Policy

- Hitotsubashi University

- fiscal reconstruction

- consumption tax

- social insurance

- social security

- Employees’ Pension Insurance

- Employee Health Insurance

- corporate income tax

- BOJ

- Domar’s condition

- Sims theory

- helicopter money

- Modern Monetary Theory

- MMT

- Ageshio-ha

- evidence-based policymaking

- EBPM

Related posts:

How Japan should avoid becoming a loophole for technology leaks to China

How Japan should avoid becoming a loophole for technology leaks to China

The First Year of Abenomics – Part 3 The impact of monetary easing has been limited— The actual role of monetary easing has been to assist in fiscal policies. — The economy has expanded on the back of public investment.

The First Year of Abenomics – Part 3 The impact of monetary easing has been limited— The actual role of monetary easing has been to assist in fiscal policies. — The economy has expanded on the back of public investment.

The 21st Century Public Policy Institute Research Project Effective Measures to Halt Birthrate Decline -Responding to the declining birthrate and aging society is Japan’s mission in world history -

The 21st Century Public Policy Institute Research Project Effective Measures to Halt Birthrate Decline -Responding to the declining birthrate and aging society is Japan’s mission in world history -

No Need to Fear a Fall in Population

No Need to Fear a Fall in Population

It is not time for local governments to compete with each other. Intensive investment in key base cities nationwide is urgently needed.

It is not time for local governments to compete with each other. Intensive investment in key base cities nationwide is urgently needed.