GAUGING JAPAN'S "SOVERRIGN RISK"

In September 2008 the world economy, hit by the financial crisis symbolized by the bankruptcy of Lehman Brothers, went into a tailspin, but in the second half of 2009 it pulled out of the dive and began to regain altitude. Then in March and April 2010, just when optimistic views were becoming widespread, yields on Greek government bonds suddenly rose, and a crisis of sovereign risk came into view. Confidence in the euro was badly shaken, and worries about European economies and the global economy spread. Once again the future of the world became shrouded in uncertainty. Stock markets tumbled, and many countries in Europe and other parts of the world experienced a mushrooming of fiscal deficits, since tax revenues had declined following the Lehman shock, while government spending had been stepped up to apply stimulus. With Greek government bonds sustaining a crippling blow, uneasiness quickly rippled through the developed world, affecting not just such Southern European nations as Portugal, Spain, and Italy, which had their own fiscal deficits and large public debts, but also Ireland, Britain, and other countries.

In its latest Economic Outlook, released on May 26, the Organization for Economic Cooperation and Development unveiled a rather rosy view in the midst of the Greek crisis. Revising its November 2009 projection for its members in the upward direction, it predicted that real economic growth would reach 2.7% in 2010 and 2.8% in 2011. To be sure, it also laid stress on worrisome developments, notably the buildup of debts in public finance, and acknowledged the uncertainty of future prospects. It called for the start of a return to balanced fiscal positions. It is imperative, the OECD said, that each country put together by the end of the year a detailed medium-term plan for restoring health to public finance.

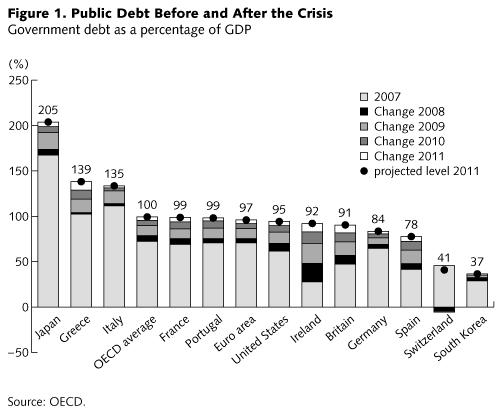

Japan’s public debt amounted to 189.3% of gross domestic product in 2009, a much larger debt ratio even than that of Greece. According to the OECD forecast, Japan’s government debt will rise to 205% of GDP in 2011 (Figure 1). In the following, after reviewing the risks hidden behind the world economy’s recovery since the time of the Lehman shock, I will sum up the arguments over a serious risk that has emerged against the backdrop of Japan’s worsening fiscal condition. This is the possibility of a collapse in the market for Japanese government bonds. At the end, I will touch on the tasks facing Kan Naoto, Japan’s new prime minister.

The Eve of the Greek Crisis

Statistics on both real GDP and industrial production indicate that the Japanese economy bottomed out in the second quarter of 2009. The Bank of Japan’s quarterly tankan surveys of business sentiment found that large manufacturers began to regain optimism in the second quarter and rapidly became more upbeat during the rest of 2009 on into 2010. In the middle of 2009 both the government and the Bank of Japan released statements declaring that business was picking up or at least no longer growing worse, and in and after the October-December quarter they reported that clear evidence of the upturn had been confirmed. Even so, in the first quarter of 2010 neither real GDP nor industrial production had regained the level they were at before the Lehman shock. In the euro area, similarly, growth resumed but did not become readily visible.

The United States fared better despite being the epicenter of the financial earthquake, and real GDP more or less recovered to the pre-crisis level. Among emerging-market countries, China staged a vigorous recovery, with GDP in the fourth quarter of 2009 expanding at an annualized pace close to 10%, while Brazil resumed positive growth in that quarter. According to the OECD Outlook, strong growth in emerging economies should contribute significantly to the recovery of the developed nations. On the eve of the Greek debt crisis, the world’s stock markets were rebounding based on the expectation that growth of real economies would continue. In New York, the Dow Jones Industrial Average of 30 large corporations had just about returned to where it was before the 2008 crash. Stock prices in Europe and Japan also rallied, rising by more than 40% in the space of a year.

In this way, many people were inclining to optimistic views, but they did so only by disregarding some major pitfalls. For one thing, the recovery relied heavily on stimulus measures, and it was going to be costly to return fiscal and monetary policies to normal. In addition, virtually zero interest rates were continuing to prevail, and this set the stage for wild fluctuations in government bond yields and resource prices. Excessive liquidity, which was a consequence of extreme monetary relaxation, became a cause of short-term volatility in the prices of stocks, bonds, and resources, as well as in exchange rates, working in conjunction with changes in political and economic circumstances.

The Nikkei average of 225 shares on the Tokyo Stock Exchange fell below the 9,500 mark on May 25, hitting the lowest level in half a year, because funds were being shifted from the stock market into the bond market. Ordinarily one would not have expected funds to be invested in government bonds around that time, since questions of sovereign risk had moved to the fore, but apparently the world’s market players had come to the conclusion that stocks were even riskier than bonds, and they were executing a return to bond markets. But while prices are now subject to great short-term volatility, it is evident that the mounting public debts cannot be sustained. Policy managers must recognize that if the yields on government bonds soar (that is, their prices plummet), the markets for government bonds run the risk of collapse.

Sovereign Risk in Developed Countries

One of the root causes of the Lehman shock was that the United States, whose current account deficits snowballed in the second half of the century’s first decade, needed to draw in funds from around the world in order to finance the deficits. With the American savings rate remaining low, financial institutions saw the development of high-risk, high-return products as a necessity for stimulating the inflow of funds from abroad. The ultimate expression of this innovation was the class of financial instruments created by securitizing subprime loans. After the financial crisis hit, however, rebalancing got underway in the United States. The savings of the household sector rose, and the deficits in the current account contracted.

The average American consumer savings rate was about 2% from 2005 to 2008, but in 2009 it jumped above 4%. We can take this as a sign that families were correcting their tendency to consume too much. With private capital investment in the United States having fallen more than 20% below its level at the start of the financial crisis, the private sector’s surplus of saving over investment expanded. The US federal budget deficit rose above 10% of GDP, but the current account deficit in 2009 fell to half its size in 2006, when it was above $800 billion. Despite such evident signs of rebalancing, however, the yield on 10-year US government bonds began to rise steeply at the end of March 2010. In Britain, meanwhile, yields on government bonds began their ascent in early February.

In Britain and the United States the government stepped in to shoulder the bad debts the private sector was saddled with by the collapse of bubbles in financial and property markets, while in Japan, where a deflationary slump persisted, public debts swelled to an unprecedented size under the impact of the Lehman shock. Worries about sovereign risk have emerged even in these countries.

Meanwhile, central banks continued to pursue a policy of exceptionally easy money. While this policy stance is presumed to have headed off any worsening of the financial crisis, the surplus funds wound up not being invested in items like plants and equipment and instead contributed to the rise in the prices of stocks, international commodities, and emerging-market assets. The assets of central banks have swollen as a result of the extreme monetary relaxation, but the velocity of money, which provides a measure of how much the money supply is contributing to economic activity, has slowed down. Easy money has failed to lead to improvement of real economies. Ripple effects associated with sovereign risk have dealt losses to financial institutions, narrowing the scope of the risks they can accommodate and applying the brakes to their lending. There is, moreover, the further risk of getting caught in a vicious circle in which a credit crunch drives down asset prices and throws cold water on business activity.

While Greece has been brought to its knees, Germany is standing tall. After the introduction of the euro in 2002, differentials in current account positions widened within the euro area. Wage costs were held down in Germany, and competitiveness grew stronger. Two-thirds of Germany’s exports go to other countries in the euro area. These exports provided Germany with recurring current account surpluses, but they became a component of growing current account deficits in some of Germany’s trading partners, such as Greece, Spain, and Italy.

In countries with red ink in the current account, the need is for wage and price restraint and fiscal austerity. The implementation of deflationary measures is politically difficult, however, since it provokes a public backlash. When we look over the content of the Greek bailout deal agreed to on May 2, we find that it is premised on action that Greece will have a tough time taking, such as lifting the value-added tax from 21% to 23% and overhauling the pension system. European economies must grapple with the structural task of recovering competitive power. The OECD outlook takes a pessimistic view of the prospects in some countries, particularly those in Southern Europe, for restructuring public finance and regaining a competitive position. There is apprehension that the risks in these heavily indebted nations will only grow larger. In Germany, by contrast, exports to countries outside of Europe are expanding briskly thanks to the euro’s depreciation. Inequalities among the euro-zone countries are thus threatening to widen. Action on restoring health to public finance is urgently needed in order to correct the euro’s overly weak value. Beyond that, the conditions for keeping the euro sound as a common currency need to be reestablished.

Japan’s Slow Slide into Fiscal Insolvency

Japan’s public debt mounted swiftly starting in the mid-1990s, more than doubling within a period of about 10 years. The reasons for the growing indebtedness can be summed up in three points.

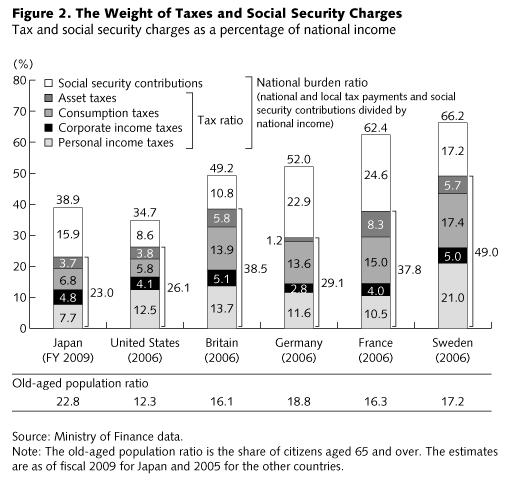

First, the tax and social welfare burden is comparatively light. The Ministry of Finance calculates what is known in Japan as the “national burden ratio” by dividing the total of tax payments and social security contributions by national income. As shown in Figure 2, the ratio was 38.9% in fiscal 2009 (April 2009 to March 2010), considerably below the ratios in European countries (as of 2006). Sweden had a very high ratio of 66.2% because of heavy taxes, which amount to 49.0% of national income. Comparing Japan and Germany, we find that even though Japan has a larger share of senior citizens, social security imposes a relatively light load of roughly 16%, against about 23% in Germany.

Second, even as the aging of the population engendered a steep climb in social security costs, tax revenue tended to dwindle as a result of sluggish growth of nominal GDP. Social security benefits, including healthcare, pensions, and other welfare spending, came to a total of ¥47 trillion in 1990 (13.6% of national income), but they almost doubled to ¥90 trillion in 2006 (23.9% of national income). It is small wonder that the state’s debts piled up.

Third, the nation’s fiscal structure was not suited to smoothly absorbing the rapidly climbing social security costs. Note that public finances did not deteriorate on account of a bloated government. In fact, the scale of Japan’s government is relatively small. When spending on social security is excluded, the GDP ratio of the remaining government expenditures for public works, civil servant salaries, and other such items falls just below 20% in Japan, lower than the ratios in Sweden (25.8%), France (24.2%), and even the United States (20.7%). But because of the graying of Japanese society, the bill for social security has been skyrocketing. Japan’s ratio of old-aged citizens (aged 65 and over) was an estimated 22.8% in 2009, the highest in the world.

With the public debt steadily growing, worries of a gentle slide into fiscal bankruptcy emerged. While people did not actually expect the state to default on its debts or long-term interest rates to shoot up, some became fearful that the government might nonetheless fall gradually into insolvency. The political leadership had been insisting that fiscal reconstruction could be accomplished without hiking taxes, but because of the spreading apprehension, it began suggesting in mid-2008, during the administration of Prime Minister Fukuda Yasuo, that the tax burden would have to be increased, and this discussion continued into 2009 under Prime Minister Asō Tarō. Because of the financial crisis, however, the economy fell into a recession, tax revenue dwindled, and the planning for fiscal reconstruction was put on hold.

The Democratic Party of Japan rose to power in the general election of August 30, 2009, and it beguiled the public with the gross illusion that public finances could be put in order by weeding out the waste in spending. The DPJ’s election manifesto contained grand promises about how huge sources of revenue were to be unearthed by careful screening of the budget, even while the “provisional” gasoline tax and other levies were discontinued, but all the talk came to naught. Most people have come to the conclusion that the wasteful-spending argument was off base from the start. The authorities say that of the ¥92 trillion budget for fiscal 2010, they will cover some ¥10 trillion by tapping reserves and surplus funds in special accounts, the so-called buried treasure of the public sector, but about ¥44 trillion will have to be financed by the issue of government bonds, which will amount to about 9% of GDP. In fact, an even greater amount of bonds may have to be issued, since it appears that tax revenue could fall even shorter than expected.

Could Government Bonds Really Collapse?

There are two contrasting views of Japan’s government bonds, whose outstanding amount has given Japan a debt ratio even higher than that of Greece, as I noted at the outset. One is the pessimistic opinion that nobody should be surprised if the prices of these bonds plummet, since Japan is in such poor financial health. The other is the optimistic outlook that a collapse in the bond market is hardly likely, since domestic savings can absorb a major portion of the bond issues. Both views, though, are overly shortsighted.

An increase in tax revenue is not in the offing for the time being, but government spending will continue to grow to meet the pledges made by the DPJ administration. The public pension system, meanwhile, is in danger of running out of funds. Under the circumstances, Japan’s public debt is sure to mount to a higher level. It is true that until now most of the government bonds have been absorbed domestically. The demand for funds to channel into investments by private companies has been on the low side ever since the mid-1990s, and as a result, domestic savings have been used mainly for the purchase of government bonds. Increased bond issues have not had a crowding-out effect, which could have caused long-term interest rates to rise. These circumstances, though, cannot be sustained forever. The sluggish capital investment by the private sector will undercut the economy’s growth potential and impede a return to growth in tax revenue.

If and when private capital investment eventually recovers, the pool of funds available for buying government bonds will grow smaller. Interest rates will begin to rise, and relying on bond sales mainly to domestic investors will become difficult. Sales to overseas investors will increase, exposing Japan to the kind of sovereign risk Greece is facing, and bond yields will have to be made more attractive. All this could cause the yen to weaken, which would make imports more expensive and could trigger inflation.

Accelerating the inflation rate is, it is said, the ultimate trick for whittling down the size of the public debt. Looking back over history, we can appreciate that when Japan found itself heavily in debt at the end of World War II, the effective weight of the load was progressively lessened by the postwar inflation. Greece is unable to make use of this strategy, since it has adopted the euro as its currency. In Japan’s case, though, inflation could be put to use. Having the Bank of Japan buy the bonds the government issues represents another possibility, but this would not be a sustainable strategy, since discipline in public finance would grow lax. The inflation route is in effect a means of forcing the people to transfer more income to the government without anybody noticing what is going on. Consumers’ real purchasing power would diminish, but all who are indebted, the government in particular, would benefit.

In the June issue of Voice, Ueno Yasunari, chief market economist at Mizuho Securities, addresses the question of the extent to which it would be possible to purchase government bonds relying on domestic funds. Making use of flow-of-funds data, he presents the following figures. As of the end of December 2009, the financial assets held by Japanese households came to ¥1,456.4 trillion, and the net assets after subtracting borrowing were ¥1,148.3 trillion. The net outstanding debts of the central and local governments combined, meanwhile, came to ¥622.9 trillion. The assets, in short, were ¥525.4 trillion larger than the debts. If this represents money that can be channeled into government bond purchases, there is enough money for absorbing new issues on the order of ¥50 trillion annually for another decade or so.

This estimate, though, rests on the premise that corporate demand for investment funds will continue to be sluggish. If private capital investment regains vigor, as I have suggested it should, there is a danger that crowding out could begin. Ueno is confident that the government bond market will not experience a sudden collapse over the next 10 years, but he expresses concern about deterioration in the economy’s fundamentals and downgrading of the soundness of the bonds by rating agencies. Factors like these would cause bond yields to rise gradually and foster conditions in which the domestic absorption of the bonds becomes difficult. We also should note that the problems in Japan’s public finance are seriously complicated by the attitudes of the people toward changing the tax system and revising the distribution of burdens and benefits.

Backpedaling on Postal Services

Early in the twenty-first century, when the economy was growing and tax revenue was flowing in, the administration of Prime Minister Koizumi Jun’ichirō set the target of achieving equilibrium in the “primary balance” by fiscal 2010. The primary balance is the balance between total government revenues and expenditures, excluding new bond issues and debt-servicing costs. The administration trained a spotlight on this aspect of a balanced budget because it saw the elimination of deficits in the primary balance as a requisite first step for heading off ballooning public debts and a crash of government bonds. If in addition to an equilibrium in the primary balance the nominal growth rate could be moved above the long-term interest rate, the ratio of the public debt to nominal GDP would cease to rise, reversing to a trend of decline.

The deficit in the primary balance in fiscal 2009 is estimated to have been ¥40.6 trillion, 8.6% of GDP, making it the largest since 1980, and it will become even larger when the government’s settlement of accounts for fiscal 2009 is finalized. In the initial budget for the year the government presumed that revenue from corporate taxes would amount to ¥10.5 trillion, but the actual results reported by the Ministry of Finance showed revenue of only ¥2.4 trillion, a 63.7% drop from fiscal 2008. Revenue from income taxes, meanwhile, fell below ¥13 trillion for the first time in 27 years. Clearly the primary balance is in even worse shape that it was before, and the time has come to take another look at it.

With the foregoing as our perspective, we can see cause for concern about fiscal discipline in the government’s program for restructuring the postal services. The reform plan has two key points. First, the ceiling for deposits in Japan Post Bank is to be doubled to ¥20 million per customer. Second, the government is to retain more than one-third of the shares in the parent company of the postal services, Japan Post Holdings Co., giving it veto power over decisions, and Japan Post Holdings is to hold more than one-third of the shares in its operation companies, such as Japan Post Bank and Japan Post Insurance. The objective of the changes is to secure funds for increased expenditures to sustain uniform postal services nationwide. But this represents a reversal from the course the government had been following, which was to privatize the postal services and spur improvement in their efficiency and service quality through competition with private businesses.

The impact of the new course on financial markets will be huge. With the doubling of the deposit ceiling for customers, it is more likely that Japanese savings will flow from commercial banks into postal deposits. That will deal a harsh blow particularly to smaller regional financial institutions. Japan Post Bank will become a bully giving commercial banks, especially small ones, a hard time.

Another point to note is that about 80% of the funds managed by Japan Post Bank are plowed into government bonds. It appears that an ulterior motive of the reform plan is to make this bank an institution devoted to absorbing government bonds even as it puts commercial banks under pressure. In effect, the government will be able to sell its bonds using the growing supply of funds in a treasure house it controls, and an erosion of fiscal discipline will become even more serious. The market is liable to take the view that the government simply lacks any solid strategy for keeping the market for its bonds in good health, and in that event bond yields will rise. The DPJ rode into power under a banner proclaiming that it would overthrow the rule of the bureaucrats, but in fact it has restored bureaucratic control over the postal services.

Indeed, the DPJ administration is also taking other steps to revive and strengthen government-affiliated financial institutions. In former years the funds from postal savings were channeled into the fiscal investment and loan program, Japan’s so-called second budget, and from there they flowed into a network of public and semipublic financial institutions. This FILP setup provided the bureaucrats with a way to control fund flows. And now it is being brought back to life. Praise can be heard for the actions instituted by the DPJ to break up vested interests, using such techniques as rigorous screening of budget requests, but as far as the postal services are concerned, the administration’s policy line is pointed in the opposite direction.

Kan’s Economic Agenda

Now a new DPJ administration under Prime Minister Kan Naoto has taken over, and it has three major economic tasks to tackle. One is reviewing and revising the child allowance, which is billed as a measure for stemming the decline in the number of children. Another is fashioning and implementing a growth strategy. And the third is drawing up a roadmap for lifting the rate of the consumption tax.

Kan says that Japan can realize a strong economy, strong public finances, and strong social welfare all at the same time, but will this really be possible? It sounds like voodoo-nomics, the plan hatched by US President Ronald Reagan in the early 1980s to enhance tax revenue by cutting taxes. That idea ended up with tax revenue in decline and the federal budget deficit on the increase. Kan’s idea is a little different. While he wants to cut corporate taxes, he hopes to couple this move with an increase in the 5% consumption tax.

Changes in the tax system have staggered effects on the economy. The Dai-ichi Life Research Institute has estimated that a 5% cut in the corporate tax rate would cause GDP to rise by about ¥1 trillion (0.19 percentage points) three years later. But tax revenue would fall by about ¥300 billion starting from the first year. This change in taxes would eventually come to have a positive impact even on government revenue only in about the ninth year. If the authorities are actually serious about adding pep to growth industries, they need to make a deeper slash of 10% or more in the corporate tax rate, and they must be prepared to see tax revenue dwindle by from ¥600 billion to ¥1 trillion during each of the first three years. In short, there would be a considerable lag before this part of Kan’s plan produced an improvement in the government’s fiscal position, and in the meantime deficits would grow, imposing a heavier load on the people. The question, then, is whether Kan will be able to persuade the public of the necessity of a change that will, over the short term, only cause red ink in the government’s budget to mount.

Each year the International Institute for Management Development publishes rankings of the competitiveness of nations. Japan snared the top spot from 1989 to 1992, but then it began a slide and wound up twenty-seventh on the 2010 scoreboard. This is an overall ranking that looks at not just market share but also the state of, for example, government regulation and public finance. We may say that the basic reason for the erosion in Japan’s competitiveness is the deterioration in its fiscal condition and the lack of a solid strategy for returning to the growth track. The government does not have even a medium-term plan for regaining financial health.

Makeshift proposals for hiking taxes to straighten out public finance do not provide a long-term solution. The administration has offered no explanation of how its plans for stepping up spending on social welfare and child allowances will impact the economy, or how they will fit into a strategy for growth over the medium to long term. The political leadership needs to show the public in a calm fashion what it considers to be a proper allocation of burdens and benefits.

The people have fully learned the lesson that populist pork-barrel policies cannot be sustained for long. If the administration hopes to gain public understanding for its plans, it must present a blueprint of the short-term effects and long-range goals, showing how burdens are to be distributed. The longer it delays, the greater will be the risk of financial collapse. When market players consider the prospects for government bonds, they take into account not just the amount of red ink at present but also the expected status of public finance and government debt in the future. Now is the time to present a vision of the desired fiscal setup 10 years down the road, including a plan for an improved tax system.

Translated from an original article in Japanese written for Japan Echo Web. [June 2010]