LESSONS OF JAPAN'S BUBBLE ECONOMY

Two decades have passed since Japan’s bubble began to burst in 1990, and throughout this period the economy has been in poor health. It has encountered successive financial crises, experienced price deflation for the first time since World War II, and seen the public debt mushroom, all the while limping along at a very slow growth rate. This has been a bewildering change for a nation that until then was registering spectacular growth. After all, over a period of more than 40 years after the war’s end, Japan’s economy had grown into an entity so weighty that it was even said to have become a threat to the economy of the United States.

Why did a speculative bubble with so much destructive power inflate in the second half of the 1980s, and why has the impact of its deflation lasted so long? These are questions that many economists are still trying to answer. Without doubt a variety of factors were involved. It is said that a failure in macroeconomic policy management was the cause of the bubble economy and that when the bubble burst, policymakers again bungled their response. And it is also said that there was basically nothing the government could have done to weather the nation’s first full-blown financial crisis of the postwar period. Arguments like these deserve to be carefully examined one by one, but treating all of them would take up more space than is available to me.

In the following I will instead place the changes in the Japanese economy in long-range perspective and seek to throw light on where and how, within the historical flow, a bubble inflated in the second half of the 1980s and stagnation set in starting in the 1990s. As I develop this argument, it will become evident that it is useful not just for looking at Japan but also for clarifying points in common with the problems many countries have encountered.

In 1990, when the bubble began to collapse, the baby-boom generation’s older members were reaching the age of 45. Subsequently large piles of nonperforming loans accumulated, quite a few financial institutions failed, and Japan got its first taste of price deflation in the postwar period. As the 1990s drew to a close, the baby-boomers were moving into their fifties. This was a time when the bubble’s collapse ushered in a period of falling prices, and it was also when the Japanese economy moved beyond the stage of fast growth with a youthful population. Japanese society had matured, and the assorted problems associated with an aging population and declining number of children had to be tackled. This huge shift in demographic structure was intimately related to the nation’s experience during the age of the bubble and falling prices.

Actually quite a few industrially advanced countries are going through a similar transition. Many are countries with their own baby-boom generation, and many are experiencing a declining birthrate, with the result that they also have a population growing top-heavy from the swelling ranks of senior citizens. The changes in Japan, though, have been more dramatic. The Japanese economy grew faster during the years of high-tempo growth, and the Japanese population has been aging faster since early in the 1990s, with the birthrate falling further. The speediness of the changes is reflected in the severity of the bubble and the downward trend in prices. In this light, a study of Japan’s experience during this period should yield lessons that will be of interest to people in other developed nations.

The High-Growth Model’s Bubble Effect

The creation of the bubble economy was not unrelated to Japan’s high-tempo postwar development. When we examine the companies that acquired a heavy debt load during the bubble’s formation, such as distribution firms and property-related businesses like general contractors, we find that they had been busily acquiring real estate with the help of extensive borrowing from banks. In the case of the distribution industry, chain stores bought land to build new outlets, and if this property rose in value, they used it as collateral for borrowing more money and buying more land. Even at times when the profits from distribution were slim, rising property prices would push up the corporate value of the chains.

As long as property prices continued to climb, this business model offered a very effective method of increasing corporate scale over a short period of time. To be sure, it should have been apparent that the model would break down if property prices stopped rising. The Japanese economy had been enjoying fast growth for a long time, however, and we may say that this threw corporate behavior off course.

Distortions in Japan’s financial markets were another key cause of the bubble’s formation. Inherently, it is not normal for a big business in distribution or a property-related industry to go calling on a bank when it wants to raise a large chunk of cash. As a financial system grows more sophisticated, major corporations become able to raise all the funds they need by issuing corporate bonds and other types of securities, which permit them to cut back on bank borrowing. Unfortunately, Japan in those days still had the financial markets of a newly industrialized country, and the weight of bank borrowing in financing remained large.

When the purpose of financing is to complete a real estate deal, companies ordinarily need to utilize the methods provided by securitization. They raise funds broadly, collecting money from numerous investors. This makes it unnecessary for firms whose main business is in distribution or real estate to provide excessive padding to their balance sheets. General investors, meanwhile, gain the opportunity to put some of their funds into property-related businesses. In the 1980s, however, there were practically no arrangements available in Japan for securitizing real estate, and even large corporations had no choice but to rely on banks for financing property transactions.

A particularly explosive bubble formed as the combined result of the myth of fast growth and financial markets of the emerging-country type. The problem of the bubble was then compounded by a monetary policy that was unable to make a proper response. When the bubble was growing in the second half of the 1980s, consumer prices in general were not rising very rapidly even though property and stock prices were skyrocketing. Orthodox monetary policy teaches that in the absence of fast inflation of ordinary prices, there is no need to pull back on the monetary reins. In this respect, Japan’s situation was like that the United States encountered midway through the twenty-first century’s first decade, when moves to tighten credit were put off despite a boom in property prices. The delay came about because US consumer prices were not rising very rapidly at that time.

Mishandling the Bubble’s Collapse

Looking back from today’s perspective, we can see that the Japanese government’s response to the collapse of the bubble created numerous problems. By 1998, eight years after the bubble started to deflate, several major financial institutions had gone bankrupt, including Yamaichi Securities, Hokkaido Takushoku Bank, and the Long-Term Credit Bank of Japan. This was a period when a mountain of bad debts cast a shadow over the economy. The government failed to come to grips with the problem, however, and the financial crisis of the late 1990s was the result. It was not until the 2002-3 period, during the administration of Prime Minister Koizumi Jun’ichirō, that work on clearing away the bad debts began to make substantial progress. More than 10 years had passed with little being done.

This was Japan’s first postwar encounter with such a huge pile of nonperforming loans, and the government did not have arrangements in place for the disposal of the debts. It was quite some time after the bubble began to deflate that the authorities worked out systems for using the power of the state to recover nonperforming assets (the Resolution and Collection Corporation) and support the reconstruction of companies buried under bad debts (the Industrial Revitalization Corporation of Japan). Furthermore, Japan was short of the human resources required for writing off bad debts, recovering assets, and putting companies back on their feet.

As I noted, the Japanese financial system continued to rely excessively on banks for collecting deposits and providing financing. Reforming this financial setup became a crucial task after the bubble burst, but struggling financial institutions were foundering, banks were engaged in realignment through mergers, and arranging a reform paving the way for the introduction of market-based financial methods, as symbolized by property-backed securities, took time. It is fair to say that because such changes and reforms were slow to make progress, the bad debts turned into a veritable quagmire.

To deal with the slump that ensued as the bubble lost air, the government relied on conventional fiscal and monetary tools. On the fiscal front, the authorities applied stimulus by cutting taxes and stepping up spending on public works, and on the monetary side, they made cuts in the policy interest rate. While such macroeconomic policies were needed, in themselves they were inadequate for getting to the root of the problems. Fundamental changes in financial markets and systems were also required. It was, in other words, a half-baked stimulus program, and it had a damaging effect. It persuaded financial institutions and debt-ridden firms to postpone radical restructuring. We should further note that the government debt ballooned as a result of the fiscal stimulation, and this placed a severe constraint on policy management over the ensuing years.

Is Fiscal Stimulus the Answer to Deflation?

At the end of the 1990s, in the midst of the prolonged slump and bad debts, Japan found itself stumbling into a period of deflation. None of the major countries, not just Japan, had experienced such a situation during the years following World War II. For the government and the corporate sector, which were carrying a heavy debt load, the deflation had the effect of further swelling the size of their debts. When it became evident that prices were likely to continue on a downward path for some time, deflation-minded individuals proliferated, and their outlook had a depressing effect on consumer spending, real estate investment, and plant and equipment investment.

It is by no means easy to bring deflation to a stop through the use of monetary tools. The policy interest rate had already been lowered almost all the way to zero, leaving no room for bold action to push interest rates down. In a situation of virtually zero nominal interest rates coupled with deflation, real interest rates rise at the speed of the price decline. Such is deflation’s negative impact on economic activity.

Viewed from the vantage point of classical Keynesian economics, Japan had fallen into a “liquidity trap” in which cuts in interest rates were not possible. Only vigorous fiscal stimulus can rescue an economy caught in a liquidity trap, we are told. The government began to implement a rescue effort of this type around 1998, during the administration of Prime Minister Obuchi Keizō, but it had only a limited effect. Worse than that, it wound up further enlarging the government debt and narrowing the scope of fiscal policy freedom.

In order to understand why prices began to deflate in the first place, we need to examine the macroeconomic supply-demand gap during the period after the bubble burst. For more than 10 years starting from around 1992, aggregate supply was larger than aggregate demand in Japan, creating what is called a deflationary gap. (Statistics for 2010 show that the gap is still present. With the exception of the few years of global overheating around 2005, it has persisted from 1992 to the present day.) A deflationary gap means that the economy has an excessive supply (demand shortage), which produces deflationary pressures and can initiate or perpetuate a downward trend in prices. Bad-debt problems and financial crises can spur the formation of deflationary conditions, but the primary cause of Japan’s falling prices was without doubt the long-term presence of this deflationary gap.

Why should the gap have persisted for so long? The graying of Japanese society is one of the factors involved, and another is the declining birthrate. Despite the massive changes in the structure of the Japanese economy, many companies continued on as before. Because they had too many facilities and too much production capacity, the economy was left with a tendency toward excessive supply. Many Japanese people, meanwhile, were conscious of their advancing years, and they were inclined to hold back on spending. We should see these as structural factors behind the deflationary gap.

On giving thought to the gap’s background, we can appreciate that it could not be easily closed through the continued application of fiscal stimulus. Stepped-up government spending can offset a demand shortage over the short term, but the government cannot continue to run up fiscal deficits year after year to cover a shortfall in demand likely to last a long time. Here we find the reason why the stimulus packages the government assembled did not function well as a remedy for deflation.

Groping in the Dark on the Monetary Front

If there is a limit to what can be accomplished using fiscal policy, might not monetary policy offer a more effective way of curing deflation? We may view the policy responses of the Bank of Japan from the second half of the 1990s until today as a trial-and-error process aimed at fashioning a set of tools for this.

Traditional monetary policy employs a short-term interest rate, the policy interest rate, as a means of adjusting the funds circulating in the money market and influencing interest rates in general, and the BOJ has also relied on this orthodox tool, as I mentioned earlier. Unfortunately, there are limits to what it can do when deflationary conditions take hold. With an economy caught in a liquidity trap and interest rates at rock bottom, making further cuts in interest rates is not possible. The BOJ found itself in a situation it had never encountered in the postwar period, one that not even the central banks of other countries had experience with. We should not be surprised that BOJ officials were perplexed about what should be done. At one point they lifted the policy interest rate overly hastily, hoping to break free of the zero-interest-rate fetters, but the result was that the economy descended into an even more serious deflationary state.

In this context, some of those on the academic side began calling for a more radical monetary policy. They urged the BOJ to deliver a signal to the market containing a commitment to pursue a fixed policy course until Japanese prices were rising at a certain pace. The classic example of this kind of policy is inflation targeting. The central bank picks a number as an inflation target and informs the public that it will implement whatever policy measures are required to attain the target. This can have a major impact on the market’s expectations of inflation. It is said that when one of the causes of falling prices is the widespread presence of deflation-minded individuals, such a policy stance can effectively reshape inflationary expectations.

The pros and cons of having the BOJ adopt inflation targeting are still being debated in Japan. Some economists have voiced negative opinions. Among them, some say that monetary management should not be aimed only at prices, while others point to a variety of problems that could occur if an inflation target were set while there were still questions about whether it would, in fact, engender an upward price trend. As a practical problem, however, the BOJ did not have the option of sticking to its conventional policy course. It had no choice but to experiment with unorthodox monetary tools, trying out methods it had never used before. One of them goes by the name of quantitative easing. Briefly stated, this is an attempt to stimulate financial markets by supplying them with extra liquidity even as interest rates remain in the vicinity of zero. The BOJ also began experimenting with statements clarifying the length of time it would follow its policy course, declaring that it would adhere to a stance of zero interest rates or quantitative easing until it had confirmed that prices were rising. This was a policy with a time limit, and in this sense it had an inflation-targeting nature.

The lessons the BOJ learned from the late 1990s on have influenced the way monetary authorities in the leading countries responded to the global financial crisis triggered by the bankruptcy of Lehman Brothers in 2008. The US Federal Reserve, European Central Bank, and other central banks boldly embarked on their own course of quantitative easing. Concerned that their countries too might descend into deflation, they aggressively bolstered their balance sheets. By then it had been recognized that the orthodox tool of adjusting interest rates to fine-tune liquidity in the money market was inadequate for resolving a major financial crisis and preventing a deflationary slide.

The importance of monetary policy has increased since World War II in the economic management of the leading countries. Once well-functioning financial markets are in place, they become closely linked through arbitrage among them. Central banks target their action mainly at the money market, but the adjustments made there spread speedily into other markets through a variety of channels. The linkages among financial markets support the effectiveness of monetary policy. They are apt to be severed, however, in the confusion of a big financial crisis like a bubble’s collapse or the Lehman shock. In that case the effects of the central bank’s moves in the money market will not necessarily ripple quickly into the markets for commercial paper, government bonds, property-backed securities, foreign exchange, and so forth.

When the global financial crisis began, accordingly, it was recognized that central banks would have to do more than manipulate interest rates in the money market, that they needed to intervene directly in, for instance, the markets for commercial paper and government bonds. In this way, the Japanese experience offers a way of interpreting the moves by central banks following the Lehman shock. Central bankers in Japan, the United States, and other countries conducted operations in a number of markets, including those for commercial paper and property-backed securities. The BOJ had been actively buying Japanese government bonds ever since the late 1990s, and it stepped up these operations.

International Ramifications of Japan’s Deflation Response

In the ongoing effort to contain deflation, Japan’s policy of ultralow interest rates has been kept in place for longer than 10 years. When the world’s second largest economy adheres to such an unusual course, naturally it has a major impact on the world economy. In financial markets, interest has focused in particular on what is called the yen carry trade. It involves raising funds in Japan, where interest rates are low, and investing them in countries where interest rates are higher. In the realm of economic theory, interest rates in all countries are supposed to move toward the same level when expectations of changes in exchange rates are taken into account, although some may have a risk premium attached, leaving them higher than others. In the real world, however, differences in nominal interest rates engender flows of funds across borders in many cases.

We should pay special attention to the yen carry trade in and after 2002, when the world economy was expanding briskly while Japanese interest rates remained close to zero. I do not know exactly how much carry trading was going on at the time, but clearly it was of a sufficient size to influence the yen’s exchange rate. Carry trading works to weaken the currency borrowed, because carry traders sell the borrowed money after converting it into other currencies. The yen in 1995 was stronger than it had ever been before, but thereafter it lost value. When we measure it using the real effective exchange rate, we find that in 2005 it had fallen to a very low level, the weakest it had been in 20 years.

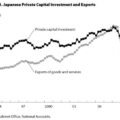

The weak yen gave Japanese exports an edge in overseas markets, notably those in the West. For the Japanese economy as a whole, the strong export performance was exceedingly good news, and it helped to trigger an upturn after the long demand slump dating from the bubble’s collapse. While the speed of the economy’s growth remained modest, the upturn became the longest uninterrupted expansion of the postwar period. From the American perspective, what could be seen was a one-way flow of imports arriving from Japan, steadily mounting deficits in the US current account, and reliance on funds brought in from Japan to finance the deficits. The lopsided relationship did not, in the end, become a politically explosive issue, since China was behaving in the same way as Japan, and on a larger scale. It is nonetheless clear, however, that there were close connections between Japan’s economic situation and the United States’ extraordinary overheating that led to the Lehman shock.

To be sure, one must doubt that an economic expansion powered in this way was good for the Japanese economy. Even though the Lehman shock did not trigger a financial crisis in Japan, the business climate turned colder than that in any other developed country when the world economy plunged into recession. That happened because the economy had been relying so heavily on exports to power the expansion. Over the years following the bubble’s collapse, not enough had been done to rectify structural problems. Action to correct the pattern of excessive supply and energize the domestic market had been put off.

The downturn that followed in the wake of the global financial crisis has provided a valuable opportunity for rethinking the Japanese economy’s structural problems from the bottom up. Whether this nation will be able to survive the difficult times and rebuild a dynamic economy will hinge on whether it can resolutely implement far-reaching reforms to remedy these problems. With the graying of society and declining number of children still in progress, work must also go forward on reforming the social security system and restoring health to public finance. For the Japanese economy, the next few years will be a crucial turning point.

Translated from an original article in Japanese written for Japan Echo Web. [July 2010]