BANKS’ HOLDING OF BONDS OBSTRUCTS JAPAN’S GROWTH

Katsu Etsuko

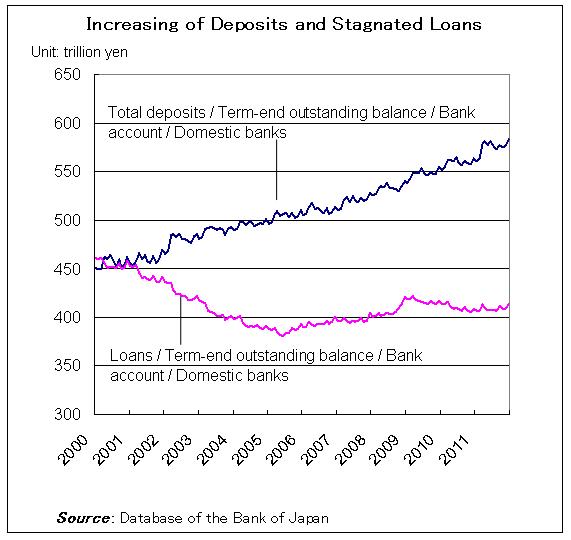

Amid a declining loan-deposit ratio (the ratio of outstanding loans against outstanding deposits), Japanese banks have been increasing their holdings of Japanese government bonds.

The three mega banks alone held as much as approximately ¥100 trillion of both short- and long-term government bonds as at the end of March 2010. JP Bank held ¥147 trillion worth of bonds.

The reasons why Japanese banks are increasing their holding of Japanese government bonds include the following: (i) Demand of corporations for financing has been contracting, as the corporate sector has been a financial surplus sector since 1998, according to the Flow of Funds Accounts Statistics of BOJ; (ii) Holding government bonds that have risk weight of zero percent (risk weighting on assets in accordance with their risk dimention) under the capital adequacy requirements by Basel committee (Bank for International Settlements (BIS) ratios) is beneficial from the perspective of capital efficiency; (iii) Banks are inclined to avoid risks associated with extending loans, reflecting the strict supervisory attitude of the Financial Services Agency in Japan; and (iv) In a zero interest-rate environment, banks can secure reasonable earnings from bond operations.

Amid declining demand for financing from companies, purchasing government bonds appears to be a reasonable course of actions for Japanese banks at first glance. Contrary to this conventional view, it can be seen that these operations potentially contain significant risk.

Japan crisis will take place?

While the sovereign crisis in Europe continues to escalate, and issues on budget deficits in the United States are presenting concerns, the outstanding balance of Japan’s gross government debt reached 213% of GDP (2011; OECD estimate), the highest level among developed nations. Moreover, the government’s annual financing requirement, including short-term bills, for fiscal 2010 reached 55% of GDP, voicing risks about holding Japanese government bonds is increasing.

Japanese banks have been failing to pursue their primary functions of credit creation and to make risk-taking, while stepping up the purchase of government bonds in a zero interest economy. These activities are in fact considered to be high risk given the potential for a hike in interest rates (a collapse in bond prices) in the future and in the context of the need to expand the Japanese economy.

The fundamental reason for the banks to choose to pursue such activities is sluggish demand for bank financing of Japanese corporations. However given the fact of the rising risk in fluctuations of asset prices, especially share prices, household financial assets have been flowing into deposits, pushing the outstanding of deposits larger.

As a result, the difference between outstanding balances of deposits and loans has been expanding, reaching as high as 183 trillion in August 2011, or 37% of GDP. Nonetheless, these activities of Japanese banks may prove to be beneficial in terms of BIS capital adequacy requirements especially of liquidity ratio standards which will be introduced in the future, Japanese banks look set to have a significant advantage over Western banks.

Holding government bonds is a reasonable private corporate activity. However, taking into account the fact that as much as 80% of household financial assets of 1,480 trillion (as at the end of fiscal 2010) is held in deposits, pension, and insurance, from a macroeconomic viewpoint, banks’ focus on bonds seems to be obstructing the flow of funds to the private sector.

This activity of banks restricting funds from flowing into the domestic private sector hinders economic growth, choking our own growth.

Meanwhile, there are also concerns that risks associated with holding government bonds are directly weakening the banking system. Although there are “home bias” phenomena for holding government bonds, Japanese banks tend to have a much higher weighting of Japanese government bonds than European banks have of European bonds. According to BIS, the ratio of the outstanding balance of domestic government bonds to their own capital exceeds 100% in Greece and Belgium, the highest levels in Europe. But the ratio for Japanese banks tops 400%.

If the rating of government bonds is downgraded, the fall in prices of government bonds will directly hit the banks’ balance sheets. Funding costs may increase, as a result of a fall in the value of collateral used for repurchasing transactions (bond lending transactions) and other financing transactions.

A fall in the value of collateral may also affect open market operations that are carried out by central banks, potentially exacerbating the credit crunch. In Japan, the share of sovereign bonds in total collateral in central bank operation is 95%, compared with approximately 15% in Europe and the United States.

Moreover, the downgrade of government bonds may result in a downgrade of the banks themselves. This will not only raise banks’ funding costs, but also restrict their access to funding market, potentially resulting in a hike in liquidity risks.

To manage the market risk, banks allocate the necessary capital after quantifying risk through the basis point value (BPV; an interest rate risk indicator), the value at risk (VaR; a method that calculates the maximum loss of a portfolio based on statistical probability), and other measures. However, as these responses are based on statistical probability, it is not fully adequate.

The change of the flow of funds also potentially raises the risks of Japanese government bonds.

Corporate financial surpluses and individual financial surpluses are sources of Japan’s excess savings at present. However, demand for reconstruction after the Great East Japan Earthquake grows, corporate demand for funds will rise, and corporates’ financial surpluses are likely to decline. Moreover, if pension funds accelerate payouts reflecting the aging society, total excess savings will turn into a shortage in funds (into current account deficits), and we may see a decline in absorbing ability of the issued government bonds which is now absorbed by 95% in domestic entities.

There is another risk of global spillovers. Japanese government bonds yields are sensitive to global risk factors including in the U.S. treasury market in particular. Among holders of Japanese government bonds, nonresidents account for only 5% as mentioned above, taking this into account a global spillover in Japanese government bonds is unlikely to take place. However, in the government bond futures market, as nonresidents account for one third of participants the spillover can certainly take place.

There is also a possibility of an increase in market volatility in the face of higher interest rate volatility. In fact, in 2003, prices of Japanese government bonds suddenly dropped and long-term interest rates jumped from 0.4% to 1.4%. This interest rate volatility was created when banks simultaneously tried to avoid risks by using the VaR (this phenomenon is called the VaR shock). There are concerns that if a rollover of government bonds cannot be carried out smoothly, a sudden change in the market can take place in the same fashion as above.

Banks must focus on their primary operations

There are three scenarios that can be forged to avoid the risks mentioned above. First, the government can cut fiscal deficits steadily and reduce the rollover risk. Second, central bank should avoid ultra-easy monetary policies including underwriting government bonds. Third, to facilitate loans to small and medium enterprises and other local companies who are short of funds, financial institutions can actively take on domestic risks using the securitization method and strengthening management advisory services for example.

Amid global trends in strengthening financial regulations, the BIS capital adequacy requirements were also strengthened (Basel III). In particular, systematically important financial institutions (SIFIs) are likely to be required to increase their capital ratio by approximately 1% to 2.5% points. Japan’s mega banks will probably be included in SIFIs.

Japanese banks have, however, successfully increased their quality of capital to date. Their capital adequacy ratios have risen significantly from past levels, and are higher than those of Western banks. The capital adequacy ratio of the Bank of Tokyo-Mitsubishi UFJ reached 14.53% as of June 2011, while Mizuho Bank reported 14.76%, and Sumitomo Mitsui Banking Corporation recorded 12.47%.

On the back of this strong capital base, Japanese banks are actively doing business in the Asian market. As a result, profit in Asian business account for as much as 30% of overall profit. In recent years, Japanese banks have made merge and acquisition of retail banks and non-banks including automobile loan companies in Asian countries, expanding their operations by capturing growth in emerging Asian economies. The banks should aggressively adopt these initiatives of credit creation which is the primary operations of banks, in Japan, their home market. Through these initiatives, Japanese banks are likely to be able to reduce risk going forward.

Translated from “Seicho wo sogaisuru hogin no kokusai hoyu (Banks’ Holding of Bonds Obstructs Japan’s Growth),”Shukan Ekonomisuto (Weekly Economist), November 1 2011, pp. 50-51. (Courtesy of Mainichi Shimbunsha)

Related posts:

JAPANESE BANKS HAVE THE POTENTIAL TO SAVE THE GLOBAL ECONOMY

JAPANESE BANKS HAVE THE POTENTIAL TO SAVE THE GLOBAL ECONOMY

PRIORITIZING THE MAINTENANCE OF LONG-TERM, COMPREHENSIVE, AND OPTIMAL COMPETITIVENESS

PRIORITIZING THE MAINTENANCE OF LONG-TERM, COMPREHENSIVE, AND OPTIMAL COMPETITIVENESS

TIME TO RECREATE JAPAN THROUGH GREEN AND SILVER INNOVATION

TIME TO RECREATE JAPAN THROUGH GREEN AND SILVER INNOVATION

DON’T FEAR HOLLOWING OUT–TRANSFORMING INTO AN INVESTMENT NATION Will SAVE JAPAN

DON’T FEAR HOLLOWING OUT–TRANSFORMING INTO AN INVESTMENT NATION Will SAVE JAPAN

PROMOTING GROWTH AND RESTORING FISCAL HEALTH SIMULTANEOUSLY

PROMOTING GROWTH AND RESTORING FISCAL HEALTH SIMULTANEOUSLY