THE BANK OF JAPAN'S EFFORTS TOWARD OVERCOMING DEFLATION

Shirakawa Masaaki

Introduction

It is a great honor for me to have the opportunity to speak to you today at the prestigious Japan National Press Club. This is my third time speaking here, having initially done so in May 2008 — my first public speech after becoming Governor of the Bank of Japan — and then again in May 2010, around the time when the European debt problem triggered by the crisis in Greece started to overshadow the global financial markets. Given that today happens to be just a few days after the Bank implemented measures to further enhance monetary easing, this is my first opportunity to provide a thorough explanation of this latest policy decision. The previous two speaking events before the Club were valuable opportunities for me, because they resulted in my being presented with many thought-provoking opinions and questions and provided the chance to put my own thoughts in order. With that in mind, I really look forward to exchanging views with you after delivering my speech.

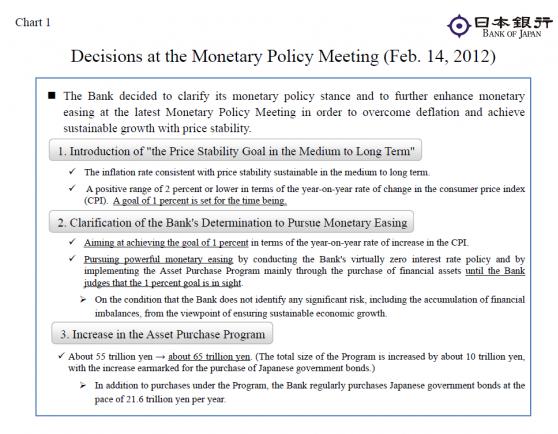

As I have just mentioned, the Bank decided the following three measures this week, at the Monetary Policy Meeting on the 14th, with a view toward clarifying its monetary policy stance and to further enhance monetary easing in order to overcome deflation and achieve sustainable growth with price stability (Chart 1). First, the Bank introduced a numerical expression of price stability in the form of “the price stability goal in the medium to long term.” Second, as for its conduct of monetary policy for the time being, the Bank stated that it will “continue pursuing powerful monetary easing with the aim of achieving the goal of 1 percent in terms of the year-on-year rate of increase in the consumer price index (CPI) until it judges that the 1 percent goal is in sight.” And third, the Bank increased the total size of the Asset Purchase Program introduced in the fall of 2010, from about 55 trillion yen to about 65 trillion yen, by adding another 10 trillion yen earmarked for the purchase of Japanese government bonds (JGBs).

Today, I will first explain the aim of and thinking behind these decisions. In the second half of my speech, I will focus on the challenge of overcoming deflation, which is the goal of the aforementioned measures, and discuss the causes of deflation as well as our thinking on necessary policy actions. After short-term interest rates in major economies including Japan declined to virtually zero, the scope of the operational tools of monetary policy has expanded from a traditional way of “raising and cutting interest rates” to the area of unconventional policy tools such as the purchase of various financial assets. Therefore, please forgive me if some parts of my speech inevitably become somewhat technical.

I. “The Price Stability Goal in the Medium to Long Term”

Numerical Expression of Price Stability

I will begin with “the price stability goal in the medium to long term.” This is the inflation rate that the Bank judges to be consistent with price stability sustainable in the medium to long term. The Bank judges it to be “in a positive range of 2 percent or lower in terms of the year-on-year rate of change in the CPI” and, more specifically, has set “a goal at 1 percent for the time being.”

The Bank conducts monetary policy based on the Principle of Currency and Monetary Control as clearly stipulated in the Bank of Japan Act; namely, that the policy shall be aimed at “achieving price stability, thereby contributing to the sound development of the national economy.” In doing so, the price stability must be of the sort that is sustainable in the medium to long term. Then, what kind of state does this “price stability” refer to? Conceptually, we can express it as “a state where economic agents such as households and firms may make decisions regarding economic activities without being concerned about the fluctuations in the general price level.” In the conduct of monetary policy, price stability needs to be expressed in numerical terms. Individual central banks express price stability in numerical terms within the context of each country’s situation and name the expression differently. Examples of such numerical expressions include the Bank of England’s “target,” “definition of price stability” adopted by the European Central Bank and the Swiss National Bank, and the U.S. Federal Reserve’s previously adopted “longer-run projection,” as well as the “longer-run goal” it introduced recently.

“Understanding,” “Goal,” and “Target”

Six years ago, in March 2006, the Bank introduced its own framework under which it expressed price stability in numerical terms, named “an understanding of medium- to long-term price stability.” After undergoing a series of changes in expression, the Bank’s recent “understanding” was “a positive range of 2 percent or lower, centering around 1 percent” on the basis of a year-on-year rate of change in the CPI.

The word “understanding” was chosen for a definite reason. Back then, the Bank was approaching the exit from its quantitative easing policy, which had lasted for the five years since 2001, and the Policy Board members had a wide range of views with regard to price stability in the coming new phase. At the same time, all the members recognized the need to publish, as the Policy Board, the basic idea of price stability in numerical terms. As a result, the decision was made to ask individual Policy Board members to present their own understanding of price stability in specific inflation rates and issue numerical expressions in the form of a range covering the presented rates, and this was published as the “understanding.”[1. For more details, please refer to “The Bank’s Thinking on Price Stability” (March 10, 2006) and Minutes of the Monetary Policy Meeting on March 8 and 9, 2006.]

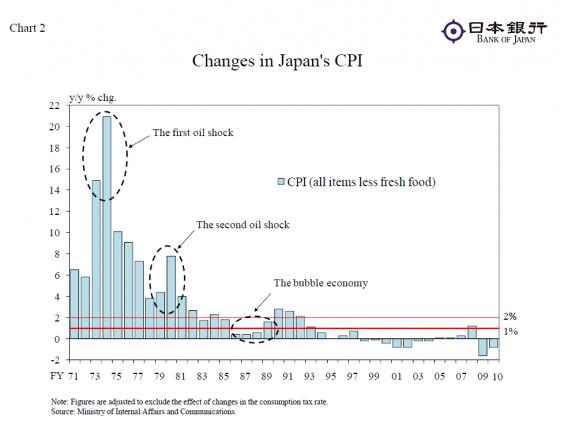

Over time, however, a growing number of voices began to be heard, pointing to the difficulties in understanding the Bank’s judgment from a collection of individual views held by each member. Others expressed the view that connotations of “understanding” did not allow for smooth interpretations of the Bank’s policy stance in its efforts toward achieving price stability, and in overcoming deflation in light of the current situation. The Bank’s decision to introduce “the price stability goal in the medium to long term” also took into account such various views. Let me summarize the differences between the “goal” and the former “understanding.” First, the “goal” introduced represented “a judgment by the Bank” and not “the views of individual Policy Board members.” Second, while judging that the “goal” was “in a positive range of 2 percent or lower in terms of the year-on-year rate of change in the CPI,” the Bank clarified this by setting it at a more specific 1 percent for the time being (Chart 2). And third, in order to strengthen the so-called “policy duration effects,” the goal is more clearly linked to the Bank’s policy commitment on the duration of powerful monetary easing including the virtually zero interest rate policy, which I will explain in more detail later.

Based on my explanation to this point, the question of why the Bank did not choose alternatives such as “target” might arise. The basic idea of the “goal” introduced is largely in line with the basic thinking held by some central banks abroad with regard to using the word “a target,” in that it expresses the inflation rate the Bank judges to be consistent with the mission of a central bank and is one that the Bank aims to achieve in the medium to long term. In Japan, however, it is still often the case that “inflation targeting” is mistakenly considered equivalent to conducting monetary policy in an automatic manner in pursuit of a certain inflation rate. In reality, in many countries, including those adopting inflation targeting, monetary policy is conducted not in such an automatic manner but with an emphasis on price and economic stability in the medium to long term, as I will explain in more detail later. The Bank judged that the Japanese wording of “the price stability goal in the medium to long term” would be the most appropriate name for the actual conduct of monetary policy.

In the case of Japan, while inflation rates have remained low over a protracted period, the sustainable levels of such rates could rise gradually in the future if efforts to strengthen the economy’s growth potential bear fruit.[2. In the “Economic and Fiscal Projections for Medium to Long Term Analysis” released by the Cabinet Office in January 2012, the following two figures are provided as estimates of the rate of increase in the CPI for the medium to long term: (1) around 1 percent (an average of 1.1 percent for the period until fiscal 2020) under the assumption that economic developments at home and abroad require vigilance, and (2) around 2 percent (an average of 1.7 percent for the period until fiscal 2020) if measures proposed in the “Basic Strategy for Revitalizing Japan” are steadily implemented amid robust economic developments at home and abroad and the average growth rates for the period until fiscal 2020 rise to about 2 percent.] In view of the high uncertainty surrounding future developments, including possible structural changes in Japan’s economy and the global economic environment, the Bank judged it appropriate to attach the term “goal” to the inflation rate that the Bank aims to achieve in the medium to long term, instead of the expression of “target” that gives a rigid impression, and to review it once a year in principle.

II. Strengthening of Policy Duration Effects

Clarification of Determination to Pursue Monetary Easing

Next, I would like to explain the second step taken at the latest Monetary Policy Meeting — the strengthening of policy duration effects. In order to generate the policy duration effects, central banks make a commitment to the future course of monetary policy based on certain conditions. When short-term interest rates almost hit zero, leaving little room for a further decline, there is a need to introduce measures that influence the entire yield curve, including the longer end, in place of the traditional operation of controlling short-term interest rates. Long-term interest rates are formulated based on the expected future path of short-term interest rates and risk premiums. Therefore, if market participants believe that a central bank’s commitment to monetary easing will continue for a long period of time and that a short-term interest rate that is a policy rate will stay low for an extended period, then this will exert a downward force on long-term interest rates.

The Bank has made the best use of the policy duration effects while engaging in maintaining the zero interest rate policy since 1999 and quantitative easing policy since 2001. More recently, based on the “understanding of medium- to long-term price stability” that I explained, the Bank made it clear that it would “continue the virtually zero interest rate policy until it judges that price stability is in sight.” Although this commitment had played a certain role in encouraging the stable formation of long-term interest rates, the Bank made two changes this time, with the aim of further clarifying its policy stance toward overcoming deflation. First, the condition for policy duration is now more clearly specified based on the 1 percent inflation rate that is set as a price stability goal for the time being. Second, the Bank judged that it was more appropriate to express the policy stance on the conduct of monetary policy in a more active manner; that is, not only acknowledging the continuation of the virtually zero interest rate policy but also pointing to other policy measures that have actually been taken. For this reason, it introduced a new policy commitment, which says “For the time being, the Bank will continue pursuing powerful monetary easing by conducting its virtually zero interest policy and by implementing the Asset Purchase Program mainly through the purchase of financial assets, with the aim of achieving the goal of 1 percent in terms of the year-on-year rate of increase in the CPI until the goal is in sight.” At the same time, based on the experiences of the forming and bursting of a bubble in Japan and the global financial crisis following bubbles in recent years, a condition to the above commitment was set that, even when price stability is maintained, the Bank checks to see whether any significant risk is materializing, including the accumulation of financial imbalances, from the viewpoint of ensuring sustainable economic growth (Chart 2).[3. During the bubble period in Japan, the rate of increase in the CPI (all items less fresh food, after adjusting for the effect of a consumption tax hike) was 0.4 percent in fiscal 1987, 0.6 percent in fiscal 1988, and 1.6 percent in fiscal 1989.]

Commitment of Timing and Commitment of Conditions

This kind of policy commitment aimed at generating policy duration effects is also adopted by central banks abroad. One way of doing this is to refer to a specific duration or timing of an exit, just like the U.S. Federal Reserve does. According to its statement, the U.S. Federal Reserve currently anticipates that economic conditions are likely to warrant an exceptionally low level of its policy rate “at least through late 2014,” but holds significant reservations with regard to such anticipation being subject to change depending on economic and price outlooks. On the other hand, the Bank of Japan makes its commitment on a “condition” based on the CPI inflation rate, instead of a specific “timing” of an exit from monetary easing. The Bank judged it better to present a condition in terms of an inflation goal, rather than specifying the timing of an exit from monetary easing to gain a greater “credibility of commitment,” and consequently more effectiveness of monetary policy, given the high uncertainty surrounding the economic and price outlooks in Japan at this juncture. As long as economic and price outlooks entail high uncertainty, it is impossible to specify the exact timing of an exit from monetary easing, but there is no uncertainty with regard to the Bank’s policy stance to pursue monetary easing until it sees the exit. Given the current state of Japan’s economy, the Bank believes that this type of policy commitment is more effective in showing its strong determination to pursue policy aiming at overcoming deflation.

Relation to Inflation Targeting

I have explained that the Bank recently introduced the combination of “the price stability goal in the medium to long term” and “strong policy commitment based on the CPI inflation rate.” How is this related to the so-called “inflation targeting?”

I would like to note at the outset that, after going through a bubble in Japan and experiencing the recent financial crises, the monetary authorities around the world have made efforts to improve their frameworks for the conduct of monetary policy by learning from each other’s lessons in the wake of those crises, and consequently have converged to share the following three elements in such frameworks.

First, they published specific inflation rates considered to be consistent with their responsibility. As I have already explained, although the wording differs, such as between the Bank of England’s “target,” “definition” used by the European Central Bank and the Swiss National Bank, the U.S. Federal Reserve’s “goal,” and the Bank’s “medo (in English, ‘goal’),” their characteristics are basically same.

Second, and more importantly, they have placed increasing emphasis on economic and price stability in the medium to long term, instead of the short term, when using the numerical expression of price stability in their conduct of monetary policy. In many cases, bubbles are formed when the economy enjoys price stability and their bursting results in significant fluctuations in economic activity and prices later. Even if the authorities try to control the effect of supply shocks such as volatility in crude oil prices in the short run, economic activity suffers a significant burden and price stability ultimately is endangered in the long run. All these kinds of experiences in recent years underscore the importance of pursuing price stability sustainable in the medium to long term. Even in the United Kingdom, where the monetary policy framework is called inflation targeting, the actual conduct of monetary policy is increasingly aimed at achieving the inflation target in the medium to long term while paying attention to economic and financial stability, instead of achieving the target at all costs in the short term.

Third, and related to the second element, major central banks have come to publish their economic and price outlooks covering a longer period. Having said that, the longer the period of forecasts, the greater their inevitable decline in terms of reliability. Therefore, these central banks increasingly emphasize the medium- to long-term perspectives in showing their basic thinking on the mechanism behind the outlook and assessing risks, instead of focusing too much on highlighting the forecast numbers themselves.

Given that the monetary policy frameworks of major central banks have converged as described, I think it no longer important to play with the taxonomy of which one is inflation targeting or not. In fact, while Chairman Bernanke made it clear that the newly introduced longer-run goal does not mean the introduction of inflation targeting, some nevertheless do call it inflation targeting. If the new monetary policy framework adopted by the U.S. Federal Reserve can be called inflation targeting, a similar view could be taken in the case of the Bank’s new framework.

III. Expansion of the Asset Purchase Program

10 Trillion Yen Increase in the Purchase of JGBs

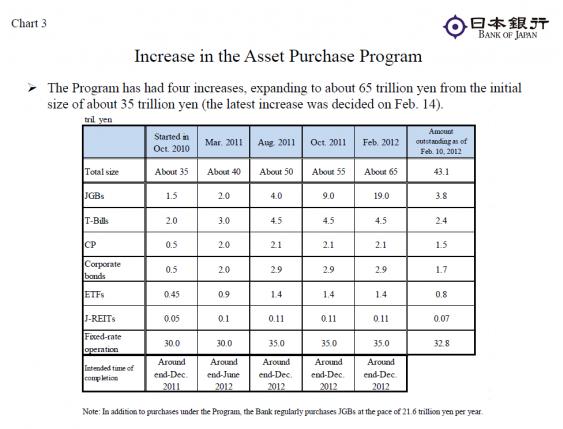

Now I would like to touch upon the third step taken at the latest Monetary Policy Meeting. That is, the expansion of the Asset Purchase Program (Chart 3).

As part of the comprehensive monetary easing introduced in October 2010, the Bank has purchased various types of financial assets through the Program. Using the newly established segregated fund on its balance sheet, which is also used for the funds-supplying operations over the longer term, the Bank has purchased JGBs — both short-term and long-term — and, in an exceptionally unusual practice for a central bank, risk assets including commercial paper, corporate bonds, exchange-trade funds (ETFs), and Japan real estate investment trusts (J-REITs). The purpose of this operation is to encourage a decline in longer-term market interest rates and a reduction in various risk premiums so that financial conditions surrounding the ultimate borrowers of funds, such as firms and households, will become more accommodative. In the process of enhancing monetary easing, the total size of the Program had been increased repeatedly, from the initial 35 trillion yen in October 2010 to 55 trillion yen, and the Bank made a decision to further increase it to 65 trillion yen by earmarking another 10 trillion yen for the purchase of JGBs at the latest Monetary Policy Meeting. The cumulative increase in the total size of the Program is about 30 trillion yen.

In addition to this Program, the Bank regularly purchases JGBs at the pace of 1.8 trillion yen per month, or 21.6 trillion yen per year, for the purpose of meeting the stable long-term demand for funds. Adding up the purchases through such operation and those through the Program, the Bank is going to purchase a large amount of JGBs until the end of this year at the pace of 3.3 trillion yen per month, or about 40 trillion yen per year. At the end of last year, the amount of JGBs held by the Bank was 66.1 trillion yen, representing 14.2 percent of nominal GDP. Although you may have the impression that the U.S. Federal Reserve has aggressively purchased government bonds, its holdings at the end of last year were 10.8 percent of nominal GDP. The holdings by the European Central Bank, which started making such purchases in 2010, represented 2.2 percent of nominal GDP.

Such a significant scale of government bond purchases entails risk, to which more attention needs to be paid. More specifically, once the purchase of government bonds by a central bank is perceived as financing government debt and not conducted for the purpose of monetary policy, this could instead invite a hike in long-term interest rates and lead to financial market instability. The Bank has repeatedly cautioned about this risk and rigidly maintains its policy of not conducting purchases of JGBs for the purpose of financing government debt.

Ensuring Accommodative Financial Conditions

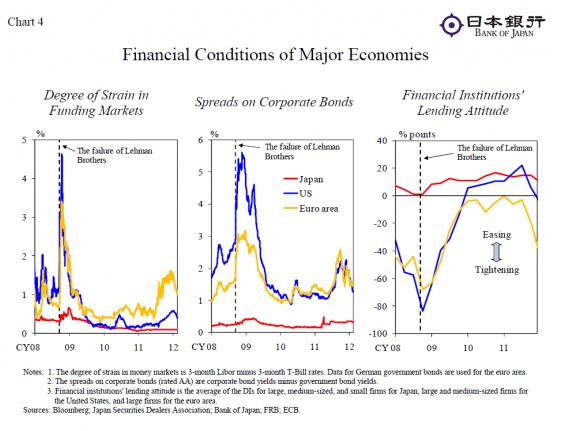

As a result of the comprehensive monetary easing consisting of the aggressive purchase of financial assets and the virtually zero interest rate policy, financial conditions in Japan have become extremely accommodative (Chart 4). More specifically, interest rates — including longer-term ones — in short-term money markets where financial institutions lend and borrow funds have stayed at very low levels, and credit spreads have been stable at low levels in corporate bond and commercial paper markets. Bank lending rates have already reached significantly low levels but continue to decline gradually. According to various surveys, firms see their financial position and financial institutions’ lending attitudes as being on a clear improving trend.

On the other hand, in the period after the Lehman shock, an increase in quantitative indicators such as the size of the Bank’s balance sheet and the monetary base — money provided by a central bank — has been moderate compared to that in the United States and in Europe, sometimes inviting the misunderstanding that the Bank’s monetary easing is insufficient. When interest rates decline to extremely low levels, people tend to hang on to money. This situation is called a “liquidity trap.” Once caught in this, it is no longer possible to measure the degree of monetary easing by simply looking at quantitative financial indicators. In fact, when we ask business managers about confronting challenges, few complain about a shortage of on-hand liquidity and many point to a lack of demand or business. In any case, in such a situation, what is more important is the easiness of financial conditions in a broad sense, such as developments in short-term and long-term funding rates for firms and risk premiums as well as funding conditions of firms and households. In the case of the United States and Europe, a significant expansion of the central bank balance sheet was indispensable to restoring stability in financial markets that had suffered significant damage to their functioning after the Lehman shock. Once provided to financial markets, the funds remained piled up in deposits with central banks because of negligible opportunity costs amid extremely low interest rate levels. On the other hand, in the case of Japan, damage to the functioning of financial markets was relatively limited and financial system stability was maintained even at the time of the Lehman shock. Therefore, without having quantitative expansion on the scale seen in the United States and Europe, the Bank could realize more accommodative financial conditions. Although tensions in global financial markets heightened again last year due to the European debt problem, the Bank has managed to firmly maintain accommodative financial conditions in Japan. It is expected that the recent determined increase in the Asset Purchase Program earmarked for JGBs will further strengthen the easing effects by affecting the entire yield curve, including the longer end.

IV. Our Thinking on Deflation and Needed Actions

Cause of Deflation

So far, I have explained the Bank’s new policy steps, which aim at overcoming deflation and bringing the economy back to a sustainable growth path with price stability. Conducting monetary policy in this way, how significant of an effect can be expected in terms of achieving the goal of overcoming deflation? Put differently, what kinds of measures are needed for Japan’s economy as a whole to ensure that this goal will be achieved? Using the time left for today’s remarks, I would like to share with you our thinking on deflation. A good starting point is to have an accurate understanding of the fundamental cause of deflation in Japan.

The various causes of deflation in Japan have been provided and discussed for years. For example, for some time, downward pressures on prices came from deregulation and the streamlining of distribution systems, which were pursued under the policy initiatives to reduce international price differentials. In Japan, both employers and employees tend to make wage adjustments for the sake of securing employment. As a result, even under the severe economic conditions, the unemployment rate in Japan did not rise compared to that in the United States and in Europe, while the declining trend for wages became more evident. Such a declining trend of wages is one of the factors explaining deflation in Japan.

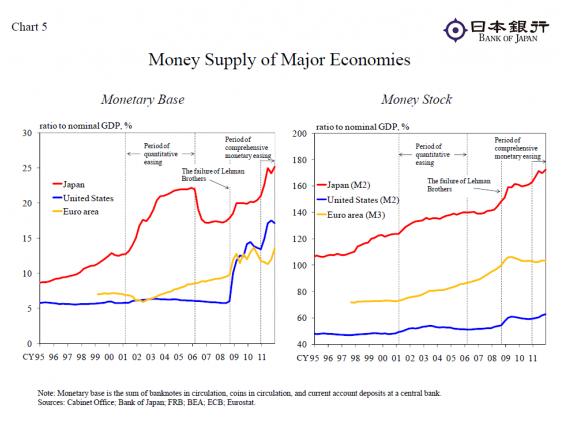

In the meantime, there is an argument that deflation has continued because of an insufficient amount of money — in other words, insufficient monetary easing by the Bank. However, such an argument needs to be properly fact-checked (Chart 5). Let’s take the typical example of money stocks, which are cash and deposits held by firms and households. The Marshallian k is the ratio of money stocks to nominal GDP that is used to measure the size of money stocks in relation to economic activity. In Japan, the ratio had been about 1.1 until the mid-1990s, which means that money stocks and nominal GDP were almost same size. Since then, the ratio has continued to rise against the background of prolonged monetary easing and is now about 1.7 — in other words, the amount of money stocks is about 805 trillion yen while nominal GDP is about 467 trillion yen. This ratio of 1.7 is the highest among major economies. Conducting a similar exercise with the monetary base and the size of the central bank balance sheets results in the same conclusion that the ratio of Japan is the highest among major economies.

As I have stated, the Bank has managed to maintain accommodative financial conditions despite the rising tensions in global financial markets against the background of the European debt problem. Viewed in this way, it appears that the problem of Japan’s economy is not a lack of money but rather a lack of business chances and growth opportunities to make the best use of money.

Ultimately, deflation is a decline in the general price level, and therefore must be caused by a deterioration in the supply and demand balance of the macro economy — i.e., a shortage of demand against supply. An output gap — an indicator for supply and demand balance estimated on the basis of certain assumptions — has continued to indicate a shortage of demand since 2000 with the exception of a very short time period.

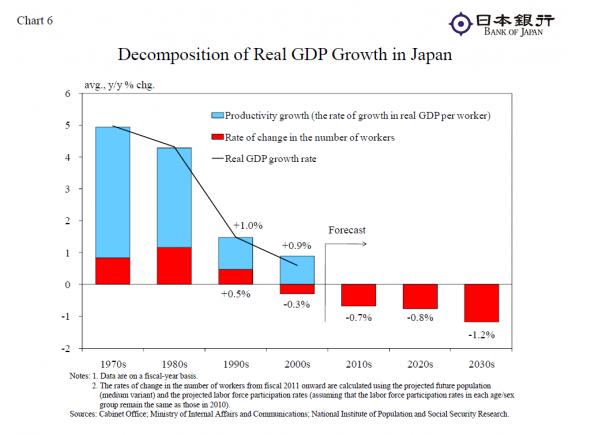

Looking back at real GDP growth rates in Japan from a relatively long viewpoint, the rates have gradually declined from 4.4 percent in the 1980s, to 1.5 percent in the 1990s, and to 0.6 percent in the 2000s (Chart 6). There are several reasons for this decline. First, the negative legacy of the bubble bursting had continued to weigh on the economy since the beginning of the 1990s. To be more specific, while firms and financial institutions were tackling the challenge of balance-sheet repair, Japan’s economy as a whole failed to adjust to a changing environment, such as increasing globalization and a rapid aging of the population. In particular, the effects of the population aging at a much greater speed in Japan than in the rest of the world have become more evident since entering the 2000s. The aforementioned widening of an output gap certainly means a shortage of demand against supply capacity, but in the current conjuncture it is specifically a shortage of demand against the supply capacity of existing goods and services. Rather, it might be interpreted as a widening mismatch of demand and supply in a sense that the supply side fails to sufficiently meet new demand in the new environment, such as demand from seniors.

In any case, when growth rates trend down in this way, households increasingly grow concerned about future income; this results in stagnant consumption and the corporate sector restrains investment in future business. If these events occur, this will lead to a vicious cycle in which contraction of expenditure by firms and households drags down actual growth rates and growth expectations.

The relationship between economic activity and prices could be compared to that between fundamental physical strength and body temperature. In order to raise the body temperature to a normal level, it is necessary to improve the fundamental physical strength. Likewise, we need to face the reality that, in order to raise prices appropriately, it is indispensable to strengthen Japan’s growth potential and growth expectations, and deflation cannot be overcome without such efforts. Of course, there are some cases where only an increase in prices takes place without changes in growth. The two oil shocks in the 1970s and the 1980s are typical examples. However, it also should be noted that a temporary increase in prices will not improve the performance of firms or quality of people’s lives, as you can easily see in the case where crude oil price hikes are transmitted to general prices, and we certainly do not wish to see such a situation materialize. The bottom line is that it is important to realize desirable inflation rates in proper sequencing so that improvement in economic activity leads to a rise in prices in a natural manner.

Efforts toward Strengthening Growth Potential

Strengthening growth potential is an extremely difficult challenge for Japan, especially given the constraint it faces — namely, the rapid aging of the population. Let me provide you with a rough calculation. The economic growth rate consists of two components: the rate of growth in the number of workers and the GDP per worker — or the rate of growth in productivity (Chart 6).[4. As for various measures for the rate of growth in productivity, see Chart 13 of Shirakawa Masaaki, “Deleveraging and Growth: Is the Developed World Following Japan’s Long and Winding Road?,” Lecture at the London School of Economics and Political Science (Co-hosted by the Asia Research Centre and STICERD, LSE), January 10, 2012.] Of these two components, the rate of growth in the number of workers started to decline in the 2000s and decreased at an annual rate of 0.3 percent on average during that decade. Based on long-term projections of demographic trends recently released by the National Institute of Population and Social Security Research, the rate of decline in the number of workers will increase further to 0.7 percent in the 2010s, 0.8 percent in the 2020s, and 1.2 percent in the 2030s. Meanwhile, although the rate of growth in productivity has fluctuated due to the effects of the Lehman shock, the recent trend is 1 percent on average in the past twenty years and about 1.5 percent on average for the period in the 2000s before the Lehman shock. The rate of growth in productivity in Japan itself is comparable to those of other G-7 economies and was highest in the period in the 2000s before the Lehman shock. However, adding this rate of growth in productivity to the rate of decline in the number of workers leaves us with a grim outlook; that is, not only will the annual rate of economic growth in the 2010s remain around 0.5 percent, but it may decline further in the longer run.

How can we strengthen the economy’s growth potential? First, while it is difficult to induce a dramatic increase in the number of workers, it is still possible to slow the pace of decline in the number by making it easier for elderly people and women to participate in the workforce. Nevertheless, the key to strengthening growth potential lies in efforts to raise productivity growth. In doing so, firms’ efforts to capture global demand and cultivate new diversifying domestic demand become necessary. On the policy front, it is important to take measures such as deregulation in order to create an environment that encourages firms to take on these challenges. Financial institutions’ expertise in identifying good business opportunities and providing risk money also become important with regard to providing financial support to firms in the course of making such efforts. Above all, it will be vital for society as a whole to realize the harsh reality and critical issues facing Japan’s economy and share a sense of values, which should include acceptance of change as well as the need to improve the economic metabolism.

The most significant contribution that a central bank could make in terms of strengthening growth potential is to maintain accommodative financial conditions and support firms from the financial side by creating an environment that makes it easier for them to explore new growth strategies. The Bank will continue to pursue powerful monetary easing, taking full account of “the price stability goal in the medium to long term” I have discussed today. It is also an essential role of the Bank to make efforts to minimize the effects on the financial market and the financial system in Japan, and do its utmost to ensure stability even in the event that some kind of destabilizing factor arises overseas amid high uncertainty surrounding global financial developments, including the European debt problem. Furthermore, in an extraordinary measure for a central bank, the Bank has been proceeding with a new fund-provisioning measure to provide support for strengthening the foundations for economic growth. This is aimed at encouraging firms to explore new growth strategies by taking advantage of financial institutions’ expertise in identifying good business opportunities.

In any event, there is no magical wand that can be used to strengthen growth potential. It is important for business firms, financial institutions, the government, and the central bank to continue making efforts in their respective roles as they face changes in the environment surrounding Japan’s economy — such as globalization and the aging of the population. The goal of overcoming deflation will be achieved through such efforts to strengthen growth potential and support from the financial side.

V. Economic and Price Developments and Outlooks

Lastly, let me brief you on recent economic and price developments as well as the outlook for Japan’s economy, in order to show how much progress has been made in terms of overcoming deflation.

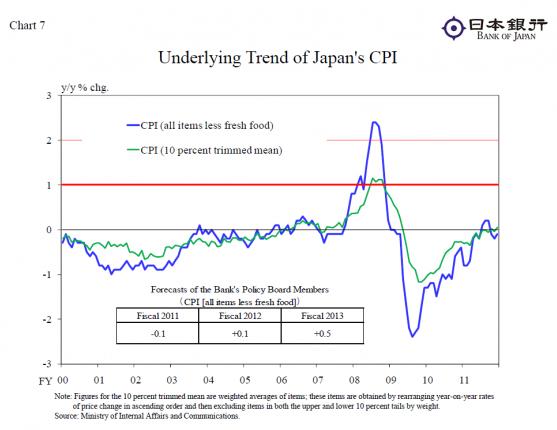

Japan’s economic activity experienced a sharp rebound from a plunge caused by the earthquake disaster in the second half of last year. Recently, economic activity has been more or less flat, reflecting downward forces deriving from the effects of a slowdown in overseas economies and the appreciation of the yen as well as upward forces stemming from firm domestic demand, such as in terms of private consumption. Although this state of the economy is expected to continue for the time being — beyond early spring — the economy is expected to return to a moderate recovery path as the pace of recovery in overseas economies picks up, led by emerging and commodity-exporting economies, and as reconstruction-related demand after the earthquake disaster gradually strengthens. The year-on-year rate of change in the CPI is expected to remain at around 0 percent for the time being but gradually increase to around 0.5 percent in the next two years or so. According to the Bank’s projections released last month of the economic and price outlooks through fiscal 2013, the real GDP growth rate is expected to be -0.4 percent in fiscal 2011, 2 percent in fiscal 2012, and 1.6 percent in fiscal 2013. As for the CPI, the year-on-year rate of increase is expected to gradually rise, from -0.1 percent in fiscal 2011, to 0.1 percent in fiscal 2012, and 0.5 percent in fiscal 2013 (Chart 7).

Looking back, the rate of decrease in the CPI (all items less fresh food) marked a low of -2.4 percent in mid-2009, recording the largest decline in recent years. Thereafter, amid the economic recovery trend, albeit a moderate one, and the narrowing of the negative output gap, the rate of decrease in the CPI has been slowing and finally reached almost zero percent on a year-on-year basis. In this sense, we have been making progress in our steps toward overcoming deflation. We admit, however, that the inflation rate still has a long way to go before it reaches the 1 percent goal that the Bank has set for the time being, as indicated in “the price stability goal in the medium to long term.”

In addition, the environment surrounding Japan’s economy is attended by various uncertainties. We cannot rule out the possibility that future developments in the European debt problem will spill over to Japan’s economy through strains in the global financial market. In terms of domestic factors, there are still many uncertainties regarding the supply and demand balance of electricity and the effects of the yen’s appreciation, as well as the pace of strengthening in reconstruction-related demand. At the same time, however, we must not overlook the fact that positive signs have recently begun to appear among developments at home and abroad. Tensions in global financial markets regarding the European debt problem have abated somewhat since around the end of 2011. Some improvement has recently been observed in the U.S. economy, mainly in the employment situation, despite the burdens of balance-sheet repair. Shifting our focus to Japan’s economy, reconstruction-related demand has begun to materialize in both public works and private demand, and private consumption has recently been firm due in part to a recovery in demand that had been temporarily restrained after the earthquake disaster last year.

The Bank has decided to further enhance monetary easing, through the measures I have discussed, with the aim of supporting the recent positive developments from the financial side. The Bank will continue making its utmost efforts in order to overcome deflation and achieve sustainable growth with price stability. At the same time, I would like to repeat that, in order to strengthen the foundation of Japan’s growth potential, there is a need to concentrate all the efforts made by concerned parties. Firms and financial institutions need to make efforts in an aggressive manner to make the best use of accommodative financial conditions, and government measures to support such initiatives in the private sector are required. In doing so, given that our economy is facing the frontline challenge of a rapid aging of the population, our responses in tackling this challenge must be at the cutting edge. We need to determinedly pave the way by ourselves, recognizing that it is not possible to find case studies for solutions and best practices in other countries. If we succeed in overcoming this challenge by ourselves, our country can provide the rest of the world with a new type of economic and social norm for the first time since we presented the high-growth economic model. I would like to finish my remarks by stressing the importance of solving problems through using our own wisdom and will.

Thank you.

Note: With the permission of the Bank of Japan, this article is reprinted from “The Bank of Japan’s Efforts toward Overcoming Deflation” (Speech at the Japan National Press Club in Tokyo by Shirakawa Masaaki, Governor of the Bank of Japan on February 17, 2012). (Courtesy of Bank of Japan)

Source: http://www.boj.or.jp/en/announcements/press/koen_2012/ko120217a.htm/

Related posts:

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

TOP MANAGERS DEBATE THE CONSUMPTION TAX ISSUE — No TIME FOR DELAY? OR ARE THERE THINGS TO DO BEFORE TAXES ARE INCREASED?

TOP MANAGERS DEBATE THE CONSUMPTION TAX ISSUE — No TIME FOR DELAY? OR ARE THERE THINGS TO DO BEFORE TAXES ARE INCREASED?

COUNTERING PANEM ET CIRCENSES IN THE 21ST CENTURY–FOR THE REEMERGENCE OF QUALITY INTELLECT

COUNTERING PANEM ET CIRCENSES IN THE 21ST CENTURY–FOR THE REEMERGENCE OF QUALITY INTELLECT

TURNING SMART COMMUNITY PRODUCTS INTO NEW EXPORT ITEMS

TURNING SMART COMMUNITY PRODUCTS INTO NEW EXPORT ITEMS