JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

Kanno Masaaki

In 2011, Japan posted its first trade deficit since 1980. Was the deficit a temporary phenomenon? And will it move back into surplus from 2012?

It is true that a decline in exports caused by the disruption to supply chains associated with the Great East Japan Earthquake and the flooding in Thailand, combined with an increase in imports of alternative energy, were significant factors for the trade deficit in 2011. In 2012, the trade balance will improve as supply chains return to normal, although it is questionable whether nuclear reactors will resume operation.

However, this does not mean that Japan’s trade balance will go back to pre-3/11 status, because a structural deficit is forming, reflecting changes in Japan’s trade structure. To provide insights into the behavior of the current account of Japan, it is essential to analyze and project the trade balance, the source of the current account surplus, along with the balance of income.

Trade deficit to increase further

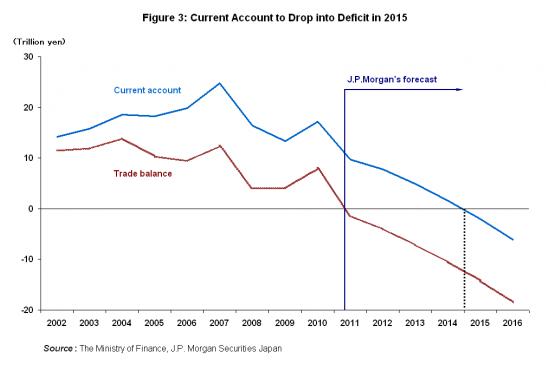

When we forecast the trade balance using a simple economic model based on the assumption that the external competitiveness of the yen (based on the real effective exchange rate) will remain unchanged and that the global economy will stage a moderate recovery, we found that the trade deficit will increase approximately three trillion yen each year to exceed 10 trillion yen in three years. According to the model, the trade deficit will be larger than the total surplus of income, services, and current transfers in early 2015, and the current account will fall into the red.

In simple terms, it is calculated as follows. Based on the assumption that the growth rate of the global economy is 3% annually (which is equivalent to 4% annually based on the forecast by the International Monetary Fund [IMF]) and that the real effective exchange rate of the yen remains unchanged, Japan’s export volume will increase 4.1% annually. Meanwhile, Japan’s import volume will increase 2.9% annually, if it is calculated under the same assumptions. Comparing the export volume with the import volume, growth in the export volume will be 1.2%point larger than that in the import volume.

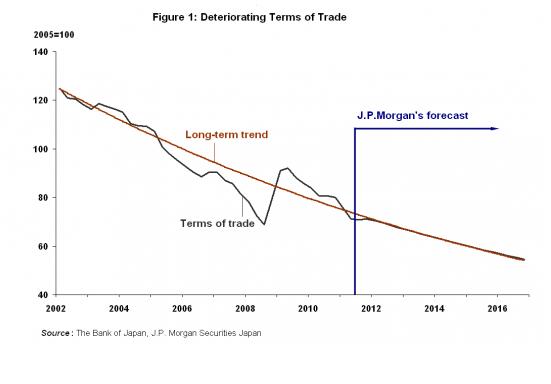

However, since the beginning of 2000, the terms of trade (export prices/import prices) of Japan have been deteriorating by 5.5% a year on average (Figure 1). In other words, the rise in import prices has been much higher than the rise in export prices. Assuming that this trend will continue, the deterioration of the terms of trade will exceed the improvement in the net export volume by 4.3% (5.5%-1.2%). Since exports and imports of Japan are roughly 70 trillion yen, the annual deterioration of the trade balance comes to three trillion yen (70 trillion yen × 4.3%).

The structural change in trade

The structural change in trade

It was after the global financial crisis that the structural changes in Japan’s trade balance became evident. Real exports (based on GDP) in the fourth quarter (October-December) of 2010 before the Great East Japan Earthquake were 9.0% less than the level of their pre-crisis peak (the first quarter [January-March] of 2008), despite the global economic recovery. For Germany, which like Japan has a comparative advantage in manufacturing, real exports in the fourth quarter of 2010 were comparable to the pre-crisis peak level and actually exceeded it by 6.1% in the third quarter (July-September) of 2011, despite the poor performance of European economies.

The biggest factor for the weak Japanese exports was the appreciation of the yen. The relationship between Japan’s export volumes and the exchange rate of the yen is such that for every 1% rise in the yen, the export volume falls 0.34%. The yen strengthened about 30% from the second half (April-June) of 2007 to the first quarter of 2009, encompassing the period of the global financial crisis. This was the result of rapid unwinding of the carry trade (in which investors borrow the yen at low interest rates and invest it to purchase currencies yielding higher interest rates) that was active in Japan and overseas until 2007. As a result of the stronger yen, the export volume declined approximately 10%.

Japanese exporters had been doing well until 2007. The export volume had been increasing 10.3% annually on average between 2002 and 2007. Exports benefited from the weak yen, with the Japanese currency declining 22% during this period. The import volume also increased 3.8% annually during this period, but growth in the export volume was 6.5% greater. This was able to offset the sharp deterioration in the terms of trade during this period.

The structural changes in Japan’s trade had already begun to occur in the early 2000s. That is, it was at the beginning of the 2000s that emerging countries such as China made their presence felt in the global market as big importers of natural resources, and it was at this point that crude oil prices began to rise, ending a period of price stability. Although Japan was forced to pay more for its imports given this historical global paradigm shift, the price of machinery, the main export for Japan, inevitably fell in international markets because of the intensified competition.

The reason why Japan was able to maintain its trade surplus despite the deteriorated terms of trade that resulted from these circumstances was that export volumes jumped thanks to the weaker yen. Following the global financial crisis, sluggish growth in export volumes due to the strong yen combined with the continuously worsening terms of trade to worsen Japan’s trade balance, as mentioned earlier.

Rapid shift to overseas production

This suggests that unless growth in export volumes recovers significantly, Japan is likely to see a growing trade deficit in the years ahead. It has been noted that Japanese exporters are increasingly sensitive to exchange rates lately.

“The Japanese Economy Outlook 2010-2011” (December 2010), a report published by the Cabinet Office, notes that “the effect of the strong yen of pushing down export volumes increased in the 2000s.” As a reason for this, the report seems to suggest that the magnitude of the fall in sales of key Japanese export industries, such as automobiles and electrical machinery, may have increased when the effect of the stronger yen was added to prices denominated in foreign currencies, as competition in overseas markets, particularly with Korean and Taiwanese manufactures, intensified.

Even looking at the situation by industry, there are many examples that suggest a deterioration of the trade balance in the future.

First, in the automobile industry, automakers have begun to shift the production of some models overseas in earnest. The industry is expected to raise the overseas production ratio further in order to boost sales in emerging markets, while also dealing with the strong yen.

J.P. Morgan Securities Japan estimates that the overseas production ratio of major Japanese automobile manufacturers has risen from 48.9% in fiscal 2003 to 67.5% in fiscal 2011 and expects it to climb to 75% in fiscal 2014 (Figure 2). In the meantime, domestic output is likely to follow a moderate downward trend.

In addition, if the overseas production ratio continues to rise in the future, it is also likely that for some models, domestic production of which has terminated, products manufactured overseas will be reimported into Japan.

Meanwhile, in the electrical goods industry, imports are rising sharply at present, and the gap between exports and imports (the trade surplus of electrical machinery) is diminishing rapidly. This is mainly because more and more companies are importing components from overseas to reduce the currency risk. If this trend continues, trade in electrical machinery will be at break-even in a few years, at which point we will no longer be able to call Japan’s electrical goods industry an export industry. Other than this, with imports of telecommunication equipment rising sharply and exceeding exports by a large margin, it has become an import industry. It is likely that imports of final products such as smartphones (multifunctional mobile phones) is accounting for a large portion of the sharp increase in imports at present.

Moreover, in the basic materials industry, the penetration of imported goods is also rising. It is reported that along with the stronger yen, imports of cheaper and half-finished goods is increasing for certain steel and chemical products with little product differentiation.

Given these developments, we note that the trade balance of Japan in the future will be greatly affected by the exchange rate behavior. It is difficult to anticipate any development in the currency market that will lead the yen to rapidly weaken in the near future. The short-term behavior of exchange rates will be significantly influenced by national monetary policy.

Comparing the monetary policy of Japan with that of the United States and Europe, while the Federal Reserve Board (FRB) and the European Central Bank (ECB) are talking of additional credit easing, the Bank of Japan (BoJ) is basically maintaining the stance of the status quo (although the BoJ says that it will continue to ease credit). This suggests that it is still difficult to cast aside the risk of a stronger yen as the basic direction.

Rise of emerging countries

A necessary condition for the current account of Japan to move into the black is a strong America. First, if US consumer spending rebounds, consumers in the United States will purchase high value-added products made in Japan, which will boost exports from Japan. It is consumers in the United States who value the high value-added products that are made in Japan at high cost. At this point, Japan’s export-oriented economic model will revive.

Second, if unemployment falls in the United States as the economy recovers, the FRB will tighten credit, or change its policy and raise interest rates. As a result, the value of the yen against the dollar will weaken, which will significantly improve the profit margins of Japanese exporters. Third, if the return on investment (ROI) improves with dollar rates rising and bond yields climbing in the United States, Japan’s income account surplus will increase. As Japan has the world’s largest net external credit, its ROI will improve significantly if the profitability of overseas investments increases and the yen becomes weaker.

On the other hand, given the rise of emerging countries, the Japanese-style business model exposes some weaknesses. First, as massive imports of natural resources and energy by emerging countries pushes up their international prices, the terms of trade of Japan will deteriorate, as discussed earlier. This means that the transfer of income from Japan to countries exporting natural resources will increase. Second, the overseas production ratio will jump. Given that the items most likely to benefit from rising demand in emerging countries are low value-added products, it is more advantageous for corporate earnings to manufacture them locally, rather than producing them in Japan where labor costs are high.

Third, the ROI will worsen in developed nations, where Japan has been focusing its investment. The profitability of investment will also decline in the United States, which also has a large output gap and shows signs of a sustained zero-interest policy as in Japan, as yields on U.S. treasuries, which Japan has been accumulating as a result of foreign exchange intervention, will decline. Although emerging countries are rapidly becoming destinations of direct investment from Japan, North America and Europe combined account for 52% of the balance of its investment.

Although the ROI in emerging countries will make a significant contribution to Japan’s income surplus, the increase in the income surplus is likely to remain small in the foreseeable future, partly because the average yield of bond investments will continue to decline.

Building a sustainable system

The discussion above shows that the deterioration of Japan’s trade balance is, in a sense, a natural phenomenon that arises in the process in which the Japanese economy adapts to the global economic realities of a multipolar twenty-first century world with new powers emerging. In a world where there is a large wage gap between developed countries and emerging countries and where manufacturing know-how reaches emerging countries quickly, it is not surprising that the trade balances of developed economies fall into the red.

Among developed countries, only Germany maintains the model of a nation based on trade; that is, achieving economic growth while maintaining a current account surplus. However, this is because Germany is able to export extensively within the euro zone, leveraging its low inflation and relatively weak currency by creating a single currency market with other less competitive eurozone countries.

However, Germany now needs to pay a different kind of cost to maintain the euro, the single currency whose institutional breakdown has become clear. The position of Germany is certainly not solid.

Our estimate shows that Japan will record a current account deficit as early as 2015 (Figure 3). However, instead of fearing a current account in the red, Japan should dedicate itself entirely to creating a sustainable economic system even under a current account deficit.

A current account deficit means that Japan will become a net importer of capital. In other words, at least some of the budget deficit of the Japanese government, the largest borrower in Japan, will need to be financed by foreign investors. This is likely to push yields on Japanese government bonds (JGB) higher, as foreign investors will demand a premium when purchasing JGBs, unlike domestic investors.

The market’s first warning

It does not necessarily mean that JGB yields will rise sharply. How much interest rates will rise will depend on how the Japanese government will respond. Although the government has been posting ever higher budget deficits, JGB yields have been falling almost consistently. As a result, although the government debt has moved constantly higher, the ratio of the debt-servicing cost to GDP has remained at only around 2%, as low as the level in the United States. A rise in JGB yields should be interpreted as the first warning of the market to the Japanese government.

If the government can respond to the market warning by showing a path to fiscal consolidation, through initiatives such as tax increases and spending cuts, any rise in long-term interest rates will be limited. In contrast, if the government continues to post higher budget deficits, ignoring the warning of the market, JGB prices will plunge while JGB yields will jump. Nevertheless, given that the average remaining period of JGB is a little longer than six years, the servicing cost will not immediately double even if JGB yields rise sharply from 1% to 2%.

However, unless the government shows the market a clear fiscal consolidation plan, investors will increasingly refrain from purchasing JGB or sell the JGBs they hold, viewing the budget deficits as unsustainable. If market sentiment is upset, even domestic investors will become jittery about holding JGBs.

The worst-case scenario would be that the government increases fiscal spending and at the same time tries to hold down JGB yields by having the BoJ purchase them. This policy would trigger inflation, as the increase in fiscal spending will be covered by BOJ financing. Although some may be pleased with this, thinking that Japan will be able to exit its deflation, the debt-servicing cost of the government will increase, as the higher expected rate of inflation will immediately push up JGB yields in the market.

In particular, if the BoJ tries to monetize the government debt without a clear commitment to fiscal consolidation, then the rise in JGB yields will be unpredictable. The recent rise in yields on government bonds of European peripheral countries with fiscal problems makes us realize the gravity of losing market confidence.

Diversify the channels for capital inflow

Meanwhile, Japan needs to diversify its channels for capital inflow from overseas, if it has become a current account deficit country. Even without relying on the bond purchase of foreign investors, capital will continue to flow into Japan, as long as there are other channels. If, for example, foreigners’ investment in real estate in Japan increases, funds will ultimately flow into the bond market.

For this money flow to become reality, it is necessary to develop an investor friendly investment conditions in Japan. For the real estate market, the United Kingdom should be used as a model. Even though the United Kingdom runs a current account deficit, its bond market remains stable in part as a result of capital inflows from overseas into real estate markets, while fiscal discipline is maintained.

At the moment, the credit default swap (CDS) spread is much lower for government bonds of the United Kingdom than it is for JGBs. The real estate market in the United Kingdom is investor-friendly, and lease contracts are based on a long-term agreement to maintain the transparency of investment profitability. Japan, too, needs to promote inbound investment through deregulation and the review of the tax system.

Translated from “Kozoteki na boeki-akajikoku ni natta nihon – 2015 nen niwa keijo-akajikoku ni naru (Japan Acquires a Structural Trade Deficit and Looks Set to Have a Current Account Deficit in 2015),”Shukan Ekonomisuto (Weekly Economist), February 21 2012, pp. 26-29. (Courtesy of Mainichi Shimbunsha)

Related posts:

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

THE BANK OF JAPAN'S EFFORTS TOWARD OVERCOMING DEFLATION

THE BANK OF JAPAN'S EFFORTS TOWARD OVERCOMING DEFLATION

TOP MANAGERS DEBATE THE CONSUMPTION TAX ISSUE — No TIME FOR DELAY? OR ARE THERE THINGS TO DO BEFORE TAXES ARE INCREASED?

TOP MANAGERS DEBATE THE CONSUMPTION TAX ISSUE — No TIME FOR DELAY? OR ARE THERE THINGS TO DO BEFORE TAXES ARE INCREASED?

The Chinese Economic Slowdown — How Does It Affect Japan? Massive debts, rising consumer prices, declining childbirth and an aging society — Days of fearing the “phantom superpower” are over

The Chinese Economic Slowdown — How Does It Affect Japan? Massive debts, rising consumer prices, declining childbirth and an aging society — Days of fearing the “phantom superpower” are over

Control of social security expenses should be expedited.Ensuring Escape from the Deflationary Spiral and to Again Increase Consumption Tax― Outlook of the primary balance of the central and local governments― Case where consumption tax rate was raised to 10% as originally planned

Control of social security expenses should be expedited.Ensuring Escape from the Deflationary Spiral and to Again Increase Consumption Tax― Outlook of the primary balance of the central and local governments― Case where consumption tax rate was raised to 10% as originally planned