Appropriate Use of Teleworking is the Key—The COVID-19 Crisis and Productivity

Morikawa Masayuki, President, Research Institute of Economy, Trade and Industry

(RIETI)

Morikawa Masayuki, President, RIETI

With the steep decline of gross domestic product (GDP) under the novel coronavirus (COVID-19) crisis, how much has productivity dropped?

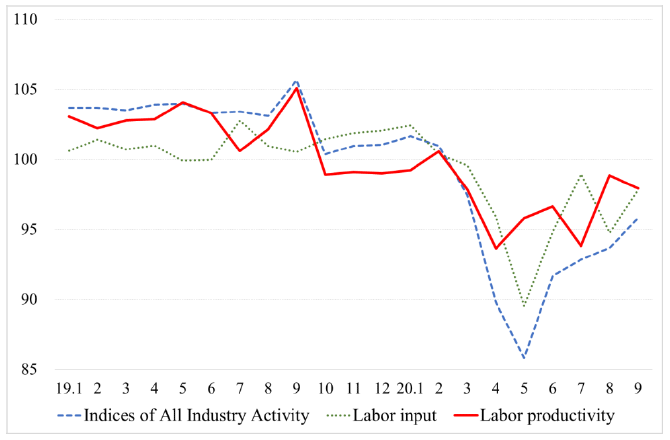

The figure below shows month-by-month changes in the overall productivity of the Japanese economy. While production activity in May 2020 was down around 15% compared with the end of 2019, productivity declined only about 3%. Although productivity still remains below the level before the consumption tax rate hike, it recovered to almost the pre-COVID-19 level in August.

Figure. Labor Productivity Under the COVID-19 Crisis

Note: The figures were indexed with the 2015 level as the base of 100 based on values obtained from the “Indices of All Industry Activity,” by the Ministry of Economy, Trade and Industry; the “Labor Force Survey,” by the Ministry of Internal Affairs and Communications; and the “Monthly Labor Survey,” by the Ministry of Health, Labour and Welfare. As the announcement of “Indices of All Industry Activity” was terminated after July 2020, the weighted average of the growth rates of the “Indices of Industrial Production” and the “Indices of Tertiary Industry Activity” was used as a substitute for the period from August.

The decline in labor productivity until now has been smaller than might have been expected because labor input, which corresponds to the denominator in the calculation, has dropped steeply in tandem with industrial activity. A breakdown shows that working time adjustments, including reduction of overtime work and temporary layoffs, contributed much more to the decline in labor input than any fall in the number of employees. If examined from a different angle, the increase in unemployment was limited because working time adjustments were quick and substantial. Among other factors limiting the labor force adjustment are the use of the employment adjustment subsidy program and companies’ behavior of retaining workers with a future labor shortage in mind.

While total factor productivity (TFP), which reflects the effects of technological innovations, cannot be calculated easily, TFP is estimated to follow a similar trend to labor productivity, given that no technological regress has occurred under the COVID-19 crisis. As productivity is determined by the relationship between output and input, the productivity level that is measured does not change significantly if the input of factors of production are quickly adjusted in accordance with a change in demand.

Given the huge negative supply-demand gap, the challenge at the moment is achieving a recovery in demand, rather than in productivity, so various measures to increase demand have been attempted. On the other hand, as raising productivity is fundamentally a medium- to long-term challenge, productivity improvement efforts should be made continuously. Even so, future productivity could be determined by our ability to successfully manage productivity under the COVID-19 crisis. Below, I will examine what should be done in order to raise productivity in a post-COVID-19 world.

First, teleworking (working from home: WFH) should be used appropriately. Since the first declaration of a state of emergency, WFH has rapidly spread, particularly among white-collar workers at large companies, resulting in an increase in the use of digital technology such as online conferencing. However, according to a survey that I conducted with employees and companies as a research activity under the Research Institute of Economy, Trade and Industry, WFH is 30 to 40% less productive on average relative to working at their usual workplace. As WFH productivity varies extremely widely depending on the nature of the task and the worker characteristics, WFH does in fact lead to higher productivity for some people, although their number is very small. However, when WFH was suddenly introduced to prevent COVID-19 infection, the productivity level was far below the level of in-office work, at least on average.

Although digitalization has made progress, close face-to-face communication is significantly more efficient and casual conversations in the workplace often inspire new ideas. Moreover, on-the-job training and the process of consensus building within an organization may be difficult to implement remotely. As WFH productivity is also affected by the adjustment cost related to the abruptness of the shift from in-office work, it is set to improve through the learning effect and investment in ICT infrastructure at home, but it is difficult to expect an increase to anywhere near the productivity of in-office work. As a matter of fact, even among people who have worked from home since before the COVID-19 crisis, WFH productivity is around 20% lower on average compared with the level in the office.

However, we will have to live with COVID-19 for some time to come, and many people want to continue WFH after the end of the pandemic. As a result, it is highly likely that WFH will gradually take root in our society. Therefore, the challenge ahead is how to minimize the decline in productivity due to the shift to WFH. Digital tools such as online conferencing offer various advantages, including overcoming the barrier of geographical distance and removing seating capacity constraints.

It may be said that the COVID-19 crisis has provided an opportunity for many people to acquire the necessary skills for using new digital tools, thereby broadening the range of options in performing their jobs. If both teleworking and in-office work are retained as options to be used for different work depending on the nature of the task at hand and the respective merits and demerits of real-world and online activities–instead of making such circumstances mutually exclusive and permanent—the overall effects on productivity could be positive in principle. However, given that in-office work produces higher efficiency for some types of work, it is likely that workers for whom full teleworking is optimal will remain an exception, with most teleworkers commuting to their office a few days a week.

The shift to WFH also has had the effect of encouraging reconsideration regarding the longstanding practices related to workplace meetings and document-based decision making. If the COVID-19 crisis acts as a catalyst for the abolition or simplification of inefficient meetings, the reduction of documents requiring the stamping of seals, and the reduction of the practice of “ringi” (Japanese process of circulating written documents for official approval from department heads), which has long been retained merely as an established custom, we may expect a positive impact of WFH on future productivity in Japan.

According to a recent survey of Japanese firms, when asked about impediments to and constraints on WFH, more than half of the respondent firms replied that some tasks cannot be performed at home due to laws, regulations, or internal rules. Specifically, many firms cited labor regulations and the laws and rules governing the protection of personal information. Teleworking productivity will improve if the scope of tasks that may be performed online is expanded through government-level efforts to correct institutional obstacles and through managerial efforts related to the revision of internal rules.

Second, levelling demand fluctuation in the services industry should be considered. What sets the current crisis significantly apart from past recessions is that the services industry has been more seriously affected than the manufacturing industry. The consumer behavior of avoiding infection risk and the government’s requests for voluntary store closures and social distancing led to an extreme decline in demand, mainly in face-to-face services industries, such as accommodations, restaurants, entertainment services and passenger transportation.

Many services industries characteristically exhibit simultaneous production and consumption, which means that production cannot be leveled over time by holding inventories. As a result, the business performance of those industries is strongly affected by fluctuations in demand. According to my analysis regarding the entertainment-related services and accommodation industries, firms and establishments whose production experience wide seasonal, weekly, daily or other time-series fluctuations have lower overall productivity. In addition, the level of productivity tends to be more dispersed across firms during recessions than in boom times.

In order to avoid customer congestion and to provide social distancing space between people, restaurants, entertainment facilities, and railway operators are adjusting seating arrangements. The peak capacity declines as a result, but if some of the peak demand can be shifted to off-peak seasons or times, congestion may be avoided and the negative impact on production may be mitigated at the same time. Some firms are trying to introduce dynamic pricing using big data and artificial intelligence (AI) technology. The diffusion of staggered commuting and staggered vacation schedules could also have an indirect positive impact on the productivity of services companies. Levelling demand through these measures may contribute to improvement in the productivity of the services industries that cannot escape the constraint imposed by simultaneous production and consumption after the COVID-19 pandemic has been contained.

Third, it is essential to take advantage of the mechanism of market dynamism. Even if the entire economy moves toward recovery following the containment of the pandemic, the level of activity is expected to differ from industry to industry and from firm to firm within an industry. During a recession, productivity gaps between firms widen, forcing some firms to exit the market. However, in the medium- to long-term, the exit of inefficient firms and productive firms’ expansion of market shares raise the aggregate productivity of the economy through the reallocation effect.

In order to provide relief to firms or establishments struggling with the COVID-19 crisis, the government has implemented relief measures such as providing financing support through government-affiliated financial institutions, the expansion of the employment adjustment subsidy program, and the introduction of the business continuity subsidy program. According to a survey that I conducted with firms with 50 or more regular employees, 44% had applied for the employment adjustment subsidy program, while 25% had applied for financing support. These policy measures are necessary in an emergency to mitigate the negative impact of the COVID-19 shock. However, it is desirable to both avoid continuing the measures for an excessively long duration and to design relief programs that will facilitate the reallocation of labor and resources between industries and between firms. Doing so will contribute to raising the overall productivity of the economy after the containment of the COVID-19 pandemic.

Translated by the Research Institute of Economy, Trade and Industry (RIETI).* The article first appeared in the “Keizai kyoshitsu” column of The Nikkei newspaper on 9 December 2020 under the title, “Korona kiki to Seisan-sei (III): Zaitaku kinmu no tekisetsuna riyo, kagi (Appropriate Use of Teleworking is the Key—The COVID-19 Crisis and Productivity).” The Nikkei, 9 December 2020. (Courtesy of the author)

*RIETI: http://www.rieti.go.jp/en/index.html

Keywords

- Morikawa Masayuki

- Research Institute of Economy, Trade and Industry

- RIETI

- Hitotsubashi University

- GDP

- COVID-19 crisis

- productivity

- teleworking

- in-office work

- service industry

- Labour Force Survey

- negative supply-demand gap

- levelling demand

- revision of internal rules

- AI

- dynamic pricing

- market dynamism

- relief programs

Related posts:

Asia’s Growth and the Rise of China

Asia’s Growth and the Rise of China

New Phase of International Trade Policy III: No conflict with RCEP, TPP

New Phase of International Trade Policy III: No conflict with RCEP, TPP

The New Phase of International Trade Policy: Expanding and Promoting the TPP after the Return of the United States

The New Phase of International Trade Policy: Expanding and Promoting the TPP after the Return of the United States

The Path to Overcoming Crisis: Finding Overall Optimum Solutions for a Heap of Challenges

The Path to Overcoming Crisis: Finding Overall Optimum Solutions for a Heap of Challenges

The Whereabouts of Household Financial Assets: The COVID-19 Pandemic Transforms Retirement Plans

The Whereabouts of Household Financial Assets: The COVID-19 Pandemic Transforms Retirement Plans