Japan’s Economy after Exit from Deflation* Potential growth rate has fallen close to zero percent due to decline in productivity ― Need for declaration of exit from deflation and strengthening of supply capacity

The CPI is steadily rising as a result of the BOJ’s new phase of monetary easing. Meanwhile, the unexpectedly low GDP growth rate indicates the low level of the potential growth rate of the Japanese economy. The potential growth rate is probably currently close to zero percent. In order to raise this, productivity needs to be increased. Given that the economy has exited deflation and has attained almost full employment, there is no need for additional demand creation. What needs to be done is to strengthen supply capacity and restore fiscal health, and to set a clear guideline that this needs doing before the CPI reaches 2%.

HAYAKAWA Hideo, Executive Fellow, Fujitsu Research Institute

End of deflation

The “greatest achievement” of the BOJ’s new phase of monetary easing (quantitative and qualitative easing; QQE) in terms of its effect on the Japanese economy is, undoubtedly, that it pushed up prices. The core CPI, which measures consumer prices excluding fresh food, jumped 3.2% in April from a year earlier. Even excluding the impact of the consumption tax hike, an increase of 1.4–1.5 percent from a year earlier can be seen. It should be noted, however, that the weak yen caused by the QQE program not only led to higher energy and foodstuff prices but also affected durable consumer goods. Home appliances such as TVs and personal computers are less competitive and the shift from “products for export” to “imported products” is also having a big impact.

The CPI forecast in the BOJ’s “Outlook for Economic Activity and Prices” (Outlook Report) is considerably higher than the level expected by private-sector think tanks and economists. Even if it is impossible for the CPI to reach 2 percent by the BOJ’s target of one year later in the spring of 2015, the CPI is expected to be close to 2 percent by the spring of the year after. Given that worries over a relapse into deflation have been allayed, the Government and the BOJ would be well advised to formally declare that “the economy has now exited deflation.”

The view that the CPI will soon reach 2 percent is based on the tightness in the labor supply/demand balance. Currently, the labor supply/demand balance is at its tightest on construction sites and in nursing care-related fields but, recently, the food services industry and retail sector in particular are experiencing extremely tight labor market conditions. Wages will rise, starting with such part timers and other irregular peripheral workers.

The unemployment rate (April 2014: 3.6%) and the job offers to job applicants ratio (April 2014: 1.08) have both almost recovered to pre-Lehman levels, but the nature of labor supply/demand balance is different. Before the Lehman shock, there was a noticeable labor shortage in the manufacturing sector because the economy was export led. However, this time, there is a noticeable labor shortage surrounding the construction sector and personal consumption. This is due to the expansion in public works projects under Abenomics and firm personal consumption. The employment rate of university students and high school students who graduated this spring released on May 16 by the MHLW and MEXT shows that the employment rate of new university graduates is lower than before the Lehman shock, but the employment rate of new high school graduates is, on the contrary, higher than the pre-Lehman level. This probably reflects the tightness of the labor supply/demand balance in areas such as construction and retail. (Fig. 1).

Near-zero potential growth rate

The QQE program was thus successful in raising prices, but also brought into focus the issue that the GDP is not growing as much as expected. Real GDP for the January–March quarter 2014 surged 1.5% (annualized 5.9%), but this is largely due to the substantial contribution of the last-minute surge in demand ahead of the consumption tax hike. The fiscal 2013 real GDP growth rate of 2.3% is also thought to actually equate to around 1% excluding the contribution of the public works projects and the last-minute surge in demand.

At the outset, the “reflationists” asserted that (1) households postpone consumption because of expected price declines, (2) high real interest rates hamper capital investment, and (3) a strong yen curbs export growth. They, therefore, painted a scenario in which an end to deflation would bring growth in personal consumption, negative real interest rates increased capital investment, and a weaker yen would result in growth in exports, and hence very high GDP growth.

Currently, personal consumption is indeed growing. However, capital investment is weak compared with the recovery in corporate earnings, and exports have not increased at all. It is clear that current conditions are by no means as projected under their scenario.

Economists who were not “reflationists” did not think that lower real interest rates would significantly boost personal consumption or capital investment. However, they did believe that a weaker yen would definitely boost exports and raise the growth rate. The current level of economic growth is enough to make them and the reflationists despair.

The fact that, in its Outlook Report released in April, the BOJ substantially lowered its fiscal 2013 GDP forecast from its forecast made in January symbolically represents this discouragement (the forecast of 2.7% made in January was lowered to 2.2% in April and the fiscal 2014 forecast was also lowered from 1.4% to 1.1%). Meanwhile the BOJ maintained its bullish stance on the price forecast, making no revision. Why is it that, despite low growth, only prices are rising? The BOJ attributes this to changing expectations, but a major contributing factor is that Japan’s potential growth rate is falling. In both the Outlook Report released in October last year and the report released in April this year, the BOJ noted that the potential growth rate was estimated at “around the 0.5 percent mark.” However, closer examination of the figures in the two reports reveals something strange.

In the report released in October last year, the potential growth rate is close to 0.3–0.4 percent (a specific figure is not published). So, the BOJ could be forgiven for saying, based on this, that the potential growth rate is “around the 0.5 percent mark.” But, in the report released in April this year, the potential growth rate looks, if anything, lower than 0.2% and is definitely not at a level that could be described as being “around the 0.5 percent mark.”

The estimate is calculated automatically. Given that the BOJ releases this estimate, it must surely know that the potential growth rate is falling. In the report, the BOJ says that the potential growth rate “is expected to rise gradually” in the future and its argument seems undeniably far-fetched. Of course, it is not easy to estimate the potential growth rate and, as the BOJ explains, a wide perspective needs to be taken.

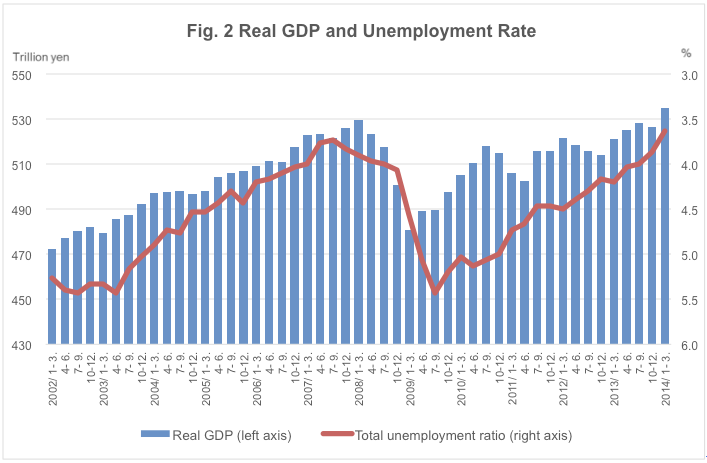

So let us try taking a more simple approach. This is something that can be seen from the relationship between real GDP and the unemployment rate (Fig. 2). The level of real GDP in January–March 2014 was, for the first time, higher than its peak before Lehman Brothers crashed. In the meantime, the unemployment rate was also down to the pre-crisis level. If supply capacity has continued increasing based on BOJ’s assumed potential growth rate of 0.5% over the six-year period following the crisis, potential GDP has to have increased by a total of 3% over the six years. However, real GDP is actually the same level as before the Lehman crisis, which means that, based on potential GDP, there is a 3% GDP gap. In this case, the unemployment rate should be rising, but the unemployment rate is, in fact, lower. Unless the potential growth rate is close to zero, this phenomenon cannot be rationally explained.

Stagnation of productivity

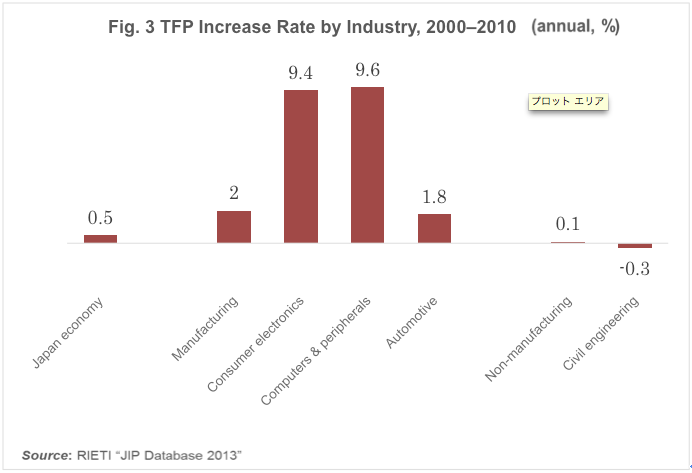

Why is the potential growth rate close to zero? Basically, this is because labor supply is shrinking due to the falling birthrate and aging population, but recently, decline in productivity is also a major contributing factor. There are two possible explanations for the decline in productivity. The first is the decline of industrial sectors where productivity was high.

The industries which previously had the highest productivity increase rates were electronics and computers. If we look at average TFP (total-factor productivity) increase rate by industry from 2000 to 2010, we see that that consumer electronics (9.4%) and computer and peripherals (9.6%) have far higher TFP increase rates than other industries. While it is impossible to know industry-specific TFP at the present time, judging from trade movements, the TFP increase rates of these industries may be substantially lower. The TFP increase rate for the automotive sector, which one would imagine to be high, is no more than 1.8%.

Another reason is that industrial sectors with low productivity have expanded. Sectors surrounding personal consumption, public works projects and the nursing care sector, which are underpinning current economic growth, have low productivity. The TFP increase rate is 0.1% for non-manufacturing and -0.3% for civil engineering. The industrial sectors with high productivity have become the losers and the sectors with weak productivity are starting to expand (Fig. 3).

The phenomenon of stagnant growth under rising prices can be interpreted as an exit from deflation due to decline in supply capacity. The realization of de facto full employment under a low growth rate is evidence of this.

Current account balance will swing into a sustained deficit between 2015 and 2020

Next, I would like to touch on Japan’s current account surplus, which has decreased substantially of late, and its widening trade deficit. There is an approach called the “development stage theory of balance of payments,” which was fashionable in the 1980s. This is a theory that divides the balance of payments into six stages: (1) young debtor nation, (2) mature debtor nation, (3) debt repayment nation, (4) young creditor nation, (5) mature creditor nation and (6) credit disposition nation, and says that the current account balance, the balance on goods and services, the income balance and net external assets change depending on the stage. Japan maintained a high rate of saving and became a country with a huge current account surplus and is still now a mature creditor nation at (5). However, if population aging accelerates further in the future, the growth rate will also naturally decline.

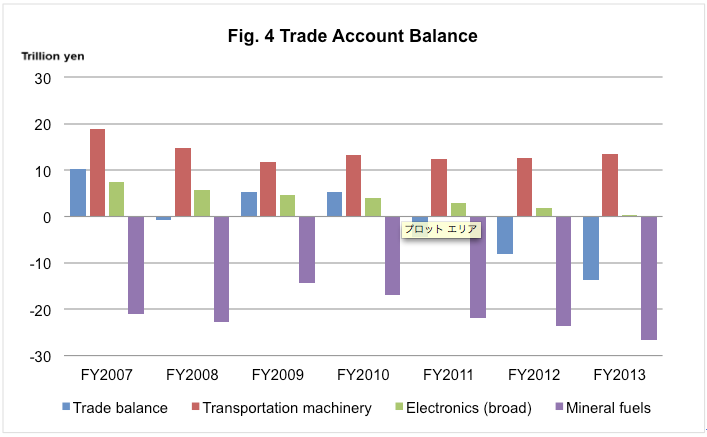

If we look at the trade balance by industry, this again shows marked contraction in the surplus for electoronics (Fig. 4). Last fiscal year, the balance was almost zero. The combination of increased energy imports and waning competitiveness symbolized by electoronics is evident in the current huge trade deficit. Since the most recent current account deficit also reflects the impact of increased imports on the back of the last-minute surge in demand, the current account balance may swing back to surplus for a time, but I believe that it will once again fall into deficit between 2015 and 2020.

In fact, in the 1980s, analysts pointed out that the Japanese economy was headed for both a labor shortage and a current account deficit. They believed that, due to the falling birthrate and aging population, labor supply would decrease and the saving rate would also fall. However, neither of these projections came true. Why? The bubble economy burst and, if anything, the savings-investment balance swung to surplus because the decline in investment was greater than the decline in savings. As for the labor supply/demand balance, there was no labor shortage because the fall in the growth rate more than offset the fall in the labor supply. Consequently, people forgot these predictions.

However, amid continued declines in the labor supply and saving rate associated with population aging, if the decline in investment is stopped, the specters of a labor shortage and current account deficit will appear. Now, at last, it seems that the long forgotten prophecy is about to come true.

If the saving rate decreases and the current account balance falls into deficit, this would, in itself, not be a bad thing. Breaking into past savings to keep going is, in itself, natural. However, in Japan’s case, there is the problem of expansion of the budget deficit, which has been underpinned by savings.

There is a government target to achieve a primary budget (PB) surplus for central and local governments by FY2020. The “Economic and Fiscal Projections for Medium to Long Term Analysis” released in January by the Cabinet Office puts the average GDP growth rate over the ten years from FY2013 to FY2022 at approximately 3% in nominal and 2% in real terms but even this assumes a PB to GDP ratio of around -1.9% or a deficit of between 11 to 12 trillion yen in FY2020. Moreover, if the potential growth rate is near to zero, it is unrealistic to expect a growth rate around the 2% mark. Recalculation using a realistic growth rate results in a greater than imagined deficit.

The CPI will in any case reach 2 percent sometime. When it does, the BOJ will either stop buying about 7 trillion yen monthly in JGBs or downscale its purchases. If it stops buying JGBs, long-term interest rates cannot possibly remain at their current level of 0.6%. Since the PB estimate is before interest payment, interest payments have to be added to the deficit. Since interest payments will increase due to higher interest rates, the fiscal balance will deteriorate even further. It is no exaggeration to say that the macroeconomic policy prescriptions all lead to this one point of restoring Japan’s fiscal health.

Recently, there is talk about additional easing by the BOJ, and if the BOJ prioritizes looking after its own interests and saving face, additional quantitative easing may be on the cards. However, this will only make the CPI reach 2 percent quicker. What will happen if growth strategies fail to materialize and the CPI just reaches 2 percent without any sign of a way forward towards restoring Japan’s fiscal health? There will be no choice but to be pessimistic. Therefore, even if the BOJ wants to embark on additional easing market participants should hold it back but, worryingly, the JGB market participants simply don’t believe what the BOJ says or appear to have absolutely no inkling that additional quantitative easing is dangerous.

Insufficient supply capacity not insufficient demand

What we need to ascertain now is that, given Japan has exited deflation and is in a state of near full employment, there is no need for additional demand creation. The kind of situation that existed before the Lehman crisis — i.e. full employment coupled with deflation — was delicate, but given that deflation has ended, there is no reason at all for additional demand. All that needs to be done now is to strengthen supply capacity and restore fiscal health, and to set a clear guideline that this needs doing before the CPI reaches 2%.

In my view, the most effective way to strengthen supply capacity, in other words, the most effective growth strategy is to reform the healthcare system. It takes time for the effects of agriculture and employment system reforms to become apparent, but healthcare system reform has the advantage that the effects of reform are quick to appear. First of all, I recommend to abolish the “free access system.” Currently, whatever their symptoms, Japanese citizens are free to choose their doctor and medical institution and are allowed to be examined at a university hospital even if they have a cold. This free access system should be abolished and a home doctor system should be introduced. Through this, improvement in the efficiency of healthcare delivery would be achieved. At the same time, efforts would be made to apply ICT in healthcare through the use of electronic medical records. Home doctors would manage the medical records and refer patients to specialists if their symptoms were serious. This would eliminate redundant tests and enable prevention of medication errors.

The menu for healthcare reform would also include the introduction of mixed billing, but politically this is no doubt a difficult theme. Even though mixed billing is reasonable, it is impossible to get past the emotional arguments that this is preferential treatment for the rich, and are people’s lives a question of money? Links between electronic medical records and the MyNumber system will prove hugely effective.

Japan’s medical technologies rank among the top in the world, and Japan realized a system of the public health insurance for the whole nation fifty years ago. However, the adoption rate of electronic medical records is extremely low. The introduction of electronic medical records would help restore Japan’s fiscal health and would also lead to increased productivity. At least, it would have a more significant effect than the introduction of mixed billing.

Another fast-working growth strategy would be to get rid of the “1.03 million yen ceiling and the 1.3 million yen ceiling,” which are thresholds for payment of income taxes and social security taxes. These ceilings not only pose an obstacle to the employment of women but they also keep down the wages of non-regular workers and are at the very heart of the problem. Removing these ceilings would no doubt act as a trigger for raising wages across the whole of Japan.

Translated from “Tokushu ‘Defure dakkyaku-go no nihon keizai’: Seisansei no teika niyori senzaiseichoritsu wa zero kinbo ni teika ― Defure-dakkyaku no sengen to kyokyuryoku no kyoka wo (Special Feature ‘Japan’s Economy After Exit from Deflation’: Potential growth rate has fallen close to zero percent due to decline in productivity ― Need for declaration of exit from deflation and strengthening of supply capacity),” Kinyu Zaisei Jijo, 16 June 2014, pp. 10–15 (Courtesy of KINZAI Institute for Financial Affairs, Inc.)

* After the Bank of Japan embarked on a new phase of monetary easing last April, the consumer price index stabilized at above year-earlier levels, silencing claims that the Japanese economy was in a deflationary slump. Since the economy has overcome the challenges of the supply-demand gap and unemployment, lingering concern of structural oversupply has faded. If anything, the falling potential growth rate associated with the shrinking working population, the falling saving rate associated with population aging, and the perpetuation of the current account deficit consistent with this are causes for concern.

Related posts:

It is not time for local governments to compete with each other. Intensive investment in key base cities nationwide is urgently needed.

It is not time for local governments to compete with each other. Intensive investment in key base cities nationwide is urgently needed.

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

CONSUMPTION TAX – NO SENSE OF CRISIS AMOUNTS TO A TRUE FINANCIAL CRISIS

CAN JAPAN EXPORT ITS WATER BUSINESS?

JAPAN PLAYS CATCH-UP TO WIN SATELLITE ORDERS

POPULATION TRENDS AND THE REGIONAL ECONOMY

CAN JAPAN EXPORT ITS WATER BUSINESS?

JAPAN PLAYS CATCH-UP TO WIN SATELLITE ORDERS

POPULATION TRENDS AND THE REGIONAL ECONOMY