Is the Bank of Japan Technically Insolvent? Dangers Involved in Long-Term Deterioration of BoJ Financial Position

Muguruma Naomi, Senior Market Economist, Mitsubishi UFJ Morgan Stanley Securities

Increasing interest is focusing on the Bank of Japan’s exit strategy, or its strategy for ending its ongoing ultra-easy monetary policy.

On April 19 [2017], the Liberal Democratic Party Administrative Reform Promotion Headquarters ([formerly] chaired by House of Councilors member Kono Taro) advised the government to study the risks associated with the Bank of Japan’s exit strategy. World central banks in charge of monetary policy are steadily moving to normalize monetary policy. On June 14 [2017], the Board of Governors of the Federal Reserve System in the United States unveiled a new exit strategy. The Fed will gradually reduce reinvestment of bond principal payments on securities holdings acquired in the course of its conduct of monetary policy with a view to reducing its total assets. It will begin reductions within the year if all goes well. Following its Governing Council meeting of June 8 [2017], the European Central Bank also indicated that it would modify its forward guidance on policy interest rates from an easing bias to a neutral stance, thus setting the stage for implementing its exit strategy.

In Japan, however, the BoJ’s price stability target of 2% is nowhere close to being achieved. At a press conference held on June 16 [2017], Bank of Japan Governor Kuroda Haruhiko declined to discuss the Bank’s exit strategy, saying it would be somewhat difficult at the present time to outline any specific modalities and the steps toward exit.

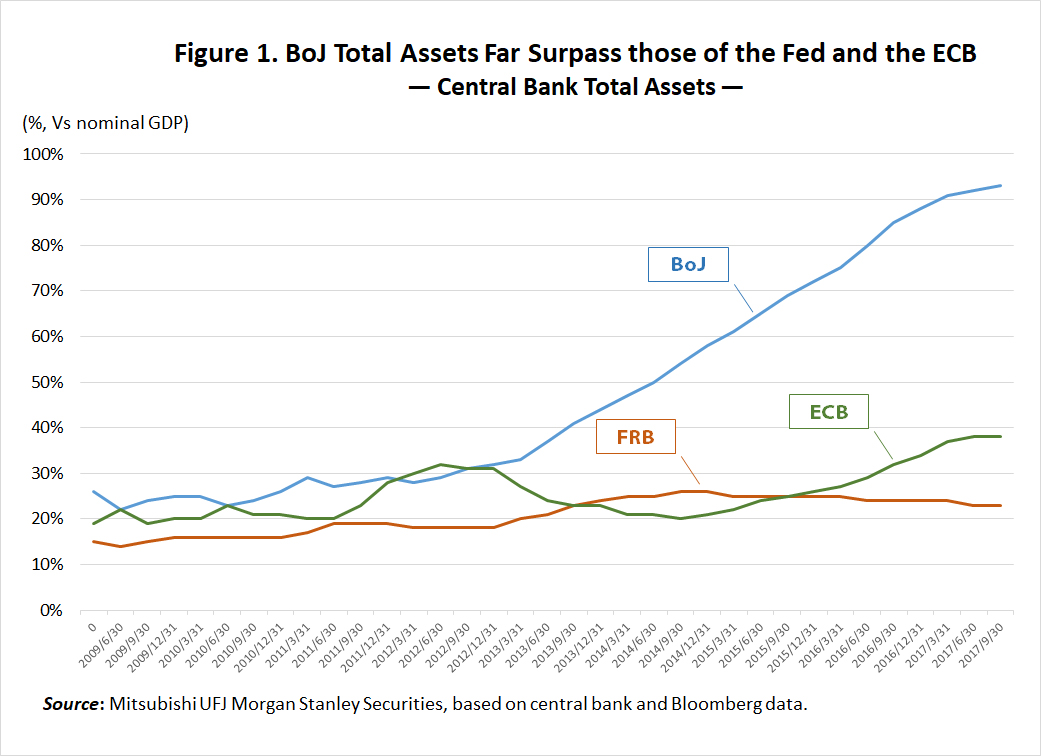

However, over four years have now elapsed since the BoJ initiated its program of massive buying of Japanese government securities. At the end of May [2017], the Bank’s total assets surpassed 500 trillion yen. This figure is more than 90% of Japan’s gross domestic product, far exceeding that of the Federal Reserve or the ECB (see Figure 1). If the BoJ’s total assets don’t stop growing, it will make the potential cost of any exit strategy all the more expensive. For this reason, some observers worry that the BoJ’s deficit will worsen and it could have a negative cash flow or face technical insolvency.

In a lecture entitled “The Role of Capital for Central Banks” given in October of 2003, former BoJ Policy Board member Ueda Kazuo highlighted the risk that (1) the central bank may become subject to various pressures from the government or fiscal authorities if its balance sheet deteriorates substantially and that (2) central banks might be tempted rely on seigniorage to offset losses, thus leading to an increase in the inflation rate.

What, then, is the financial status of the BoJ with respect to policy normalization?

A central bank does not normally run a deficit. A central bank’s assets comprise cost-free bank notes (paper currency issued by the central bank) and reserve deposits (current account balances which private banks are obligated to maintain at the central bank), and the central bank receives interest income from assets such as its government debt holdings and its loans to private banks. It is said that central banks can not become insolvent since they have seigniorage income.

The balance sheets of central banks in industrialized countries underwent a change following the Lehman shock. With the aim of lowering market interest rates, they have engaged in massive asset buying, mainly government bonds, under a policy of quantitative easing. On the liabilities side, they have seen a rise in their excess reserves (private bank current account balances with the central bank in excess of the minimum required reserve).

In order to raise short-term interest rates in the course of normalizing monetary policy, central banks need to either (1) sell their government debt holdings, reduce their excess reserves and revive the demand for funds by private banks, or (2) raise the interest rate on excess reserves (the interest rate paid to private banks on their excess reserves), which is the lower limit of market interest rates.

There is considerable risk that sales of central bank government debt holdings may result in a sharp decline in the government bond market, so like the Fed, the BoJ is likely to choose the second option and raise the interest rate on excess reserves. Also, both the Fed and the BoJ use the amortized cost method for valuing their holdings of government securities, meaning their cash flow would not be affected even if long-term interest rates were to rise and government bond market prices were to fall. Using the amortized cost method for home country bonds and the mark-to-market method for foreign currency denominated assets is the general practice under the financial provisions of central banks.

Estimating Losses Arising During Exit

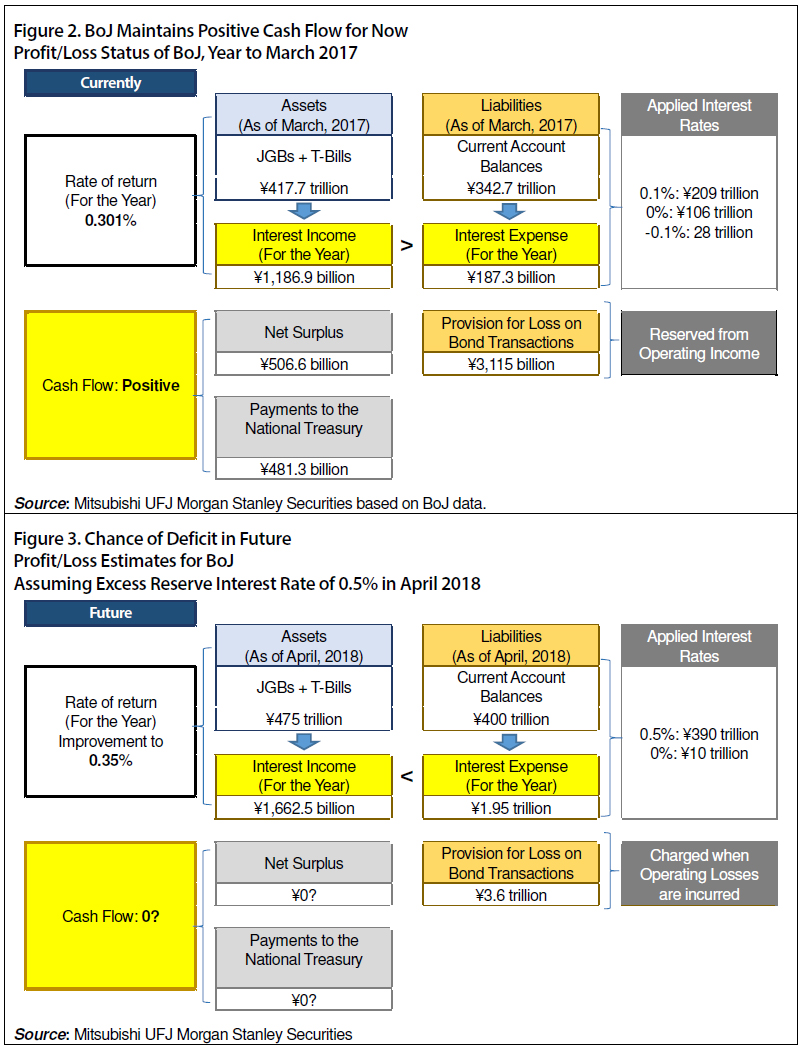

Let us consider the likelihood of losses arising from policy normalization with reference to the BoJ’s financial results for the year ended March, 2017. At the end of the fiscal year, the BoJ’s government bond holdings stood at just over 417 trillion yen. During the year, the Bank earned just under 1.2 trillion yen in interest income (Figure 2). Its rate of return has fallen to about 0.3%. Meanwhile, on current account balances of just under 343 trillion yen the BoJ paid interest of 187.3 billion yen. At present the Bank’s interest expenses are about one sixth of its interest income from government bonds. Its surplus for the year topped 500 billion yen, and the Bank paid 481.3 billion into the treasury.

However, if the BoJ normalizes monetary policy by raising the interest rate it pays on excess reserves, which constitute the lion’s share of its current account balances, the Bank’s interest expense would naturally rise. It might then be unable to cover these payments with the interest income on its government bond holdings.

Our summary projections regarding the Bank’s status are presented in Figure 3. We assume that the Bank will raise the excess reserve interest rate to 0.5% from the present 0.1% in April of 2018 when Governor Kuroda’s term of office expires. The BoJ continues its asset purchase program until the rate hike, so its government bonds holdings will likely be around 475 trillion yen while its total current account balances will be around 400 trillion yen in April 2018.

The BoJ pays a rate of 0.5% on its excess reserve balance of 390 trillion yen, or its total current deposits less required reserves. Its interest expense will thus rise to 1.95 trillion yen. Meanwhile, its interest income on its government bond holdings will depend on how well its rate of return improves. Of the Bank’s government bond holdings, bonds valued at about 50 trillion yen will reach maturity during the fiscal year, which is estimated at about 10% of the total.

When the Bank moves to raise the interest rate on excess reserves it will raise its guided long-term interest rate (measured by the yield on the benchmark 10-year Japanese government bond), which is now about 0%. If the BoJ acts decisively to raise the long-term rate, there will be considerable impact on the economic climate and the government bond market. If the BoJ boosts the rate on excess reserves to 0.5%, its target for the 10-year yield will probably be around 1%. If we assume that the BoJ shortens the average maturity of repurchased government bonds to about seven years (the 7-year yield would be around 0.7%—0.8%), its overall rate of return will improve to about 0.35%, a marginal improvement over the present 0.301%. Nevertheless, interest income on the BoJ’s government bond portfolio will be no more than 1,662.5 billion yen, or less than its interest payment on excess reserves.

A negative spread of this extent would have only a small impact on the BoJ’s financial position and could adequately be covered by the Bank’s provision for possible losses on bond transactions (a reserve against possible losses incurred in bond transactions), which stood at just over 3 trillion yen at the end of the year ended March, 2017.

However, if the BoJ thereafter continues to raise the rate of interest paid on excess reserves, its negative margin would widen considerably. Since any estimate of the total cost of the BoJ’s policy normalization would depend on the Bank’s interest rate decisions, it is impossible to reach any firm conclusions, but it does seem certain that so long as the BoJ’s rate of return remains below the rate it pays on excess reserves, the Bank could easily incur losses.

Past Instances of Central Bank Deficits and Technical Insolvency

Let us now consider what inconveniences central banks have faced when posting losses and falling into technical insolvency.

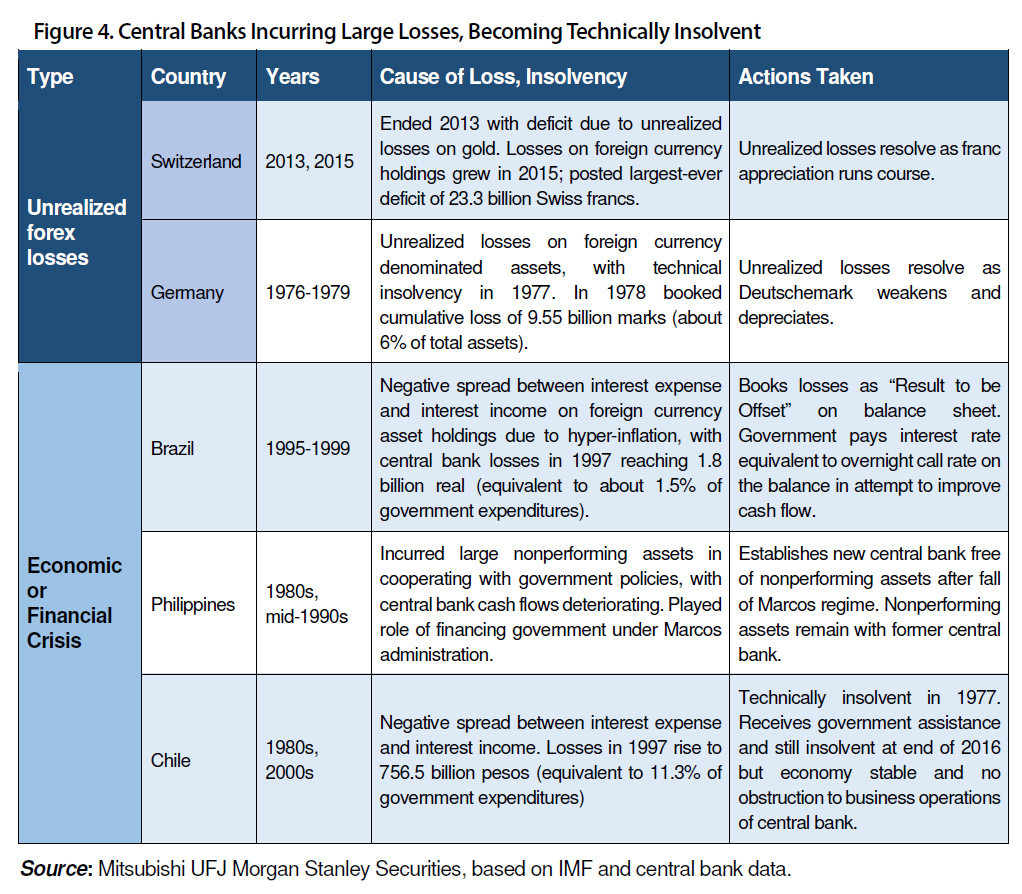

Since they can themselves create money, central banks in fact do not need capital. A central bank needs some level of capital when beginning operations, but after that, issuance of money and performance of its payment obligations are not constrained by its capital in the course of its business. The BoJ has never posted a loss on a fiscal year basis, but a look at world history shows that it is not unusual for central banks to do so. Broadly speaking, central banks have done so either because they have incurred unrealized losses on asset holdings denominated in foreign currencies or because they have become saddled with nonperforming assets arising in response to actions taken to cope with economic crises.

In countries where the central bank administers the country’s foreign currency reserves, unrealized losses in the country’s foreign currency denominated assets can arise if the country’s home currency appreciates, and if that loss can not be offset with other gains, the central bank may incur a deficit. One example from recent memory is that of the Swiss National Bank. More than 90% of the bank’s total assets are denominated in foreign currencies. The bank’s financial report for the year 2015 showed ballooning unrealized losses owing to an appreciation of the Swiss franc against the euro, with the bank posting a loss amounting to 23.3 billion Swiss francs, the biggest loss in the history of the bank (see Figure 4). Germany’s Bundesbank suffered a deficit in 1976, and it was technically insolvent during the years 1977 through 1979. The cause was an appreciation of the Deutschmark against other currencies. The bank’s cumulative losses peaked as reported in its financial results for 1978, reaching 9.55 billion marks or about 6% of the bank’s total assets. In both cases, however, the appreciation of the home currencies unwound, eliminating the losses.

No examples can be found in which a central bank’s deficit or technical insolvency arising from unrealized losses on its foreign currency denominated asset holdings have led to a loss of confidence in the country’s currency or creditworthiness. This may be attributed to the fact that, the losses would be extinguished if such concerns led market participants to sell the country’s currency, and that the losses would eventually be resolved because the value of the home currency would not continue to appreciate forever. One risk seen resulting from a deterioration in the financial position of a central bank is rapid inflation, but the impact of appreciation of the home currency would be in the opposite direction (disinflation).

In Japan, the Ministry of Finance administers foreign currency reserves, and the foreign currency denominated assets held by the BoJ stood at 6.6 trillion yen as of the end of the year ended March, 2017, just 1.3% of the Bank’s total assets. This example therefore does not apply in the BoJ’s case.

Economic crises represent another potential cause for losses to emerge, and these have indeed been serious. There were many in developing countries in the 1980s and 1990s, and they have occurred in the first decade of the present century as well (see Figure 4). There have been many examples in which the central bank has provided liquidity support to private business firms or financial institutions but been unable to collect repayments. Misguided economic policies have also been a cause, with central banks having to take on foreign currency denominated liabilities that should have been the responsibility of the government or to take on nonperforming assets after being forced to cooperate with the government’s industrial policies.

Capital injections into or restructuring of the central bank exist as possible steps toward getting economies back on track. In the 1980s, the former central bank of the Philippines was burdened with nonperforming assets, leading to a deterioration of its financial position. A New Central Bank Act was ultimately put into effect in 1993 to restructure the bank, and a new central bank was established free of impaired assets.

In the past, the BoJ was unable to recover a portion of claims which it held on the defunct Yamaichi Securities, although the amount was limited. Looking further back in history, the BoJ’s financial position deteriorated when, following the Great Kanto Earthquake in 1923, the Bank agreed to rediscount commercial bills (earthquake bills) which later proved to be uncollectible.

However, past instances in which the financial positions of central banks deteriorated owing to economic crises are not comparable when considering the cost of BoJ policy normalization now. This is because, according to the BoJ’s explanation, the central bank would have achieved the 2% inflation target accompanied by rising wages when it starts policy normalization. This would not by anything like a financial crisis.

The cost of the BoJ’s policy normalization should be seen from a different perspective. Specifically, that perspective is how present and future seigniorage is to be shared with the government.

Let us turn next to the preparations which other central banks are making to provide for the costs to be incurred as they unwind ultra-easy monetary policies.

The example which is easiest to understand is that of Bank of England. The BoE decided from the outset that all gains or losses arising from its asset purchase program should devolve to HM Treasury. In 2012 it was decided that any income arising from accumulated asset purchases by the central bank should be transferred to the Treasury. Since that time, these payments have been on a quarterly basis. Since any losses arising in the sale of UK debt securities in the context of the BoE’s policy normalization will also be incurred by HM Treasury, the BoE need not worry about the cost of policy normalization.

Preparations for Policy Normalization Differ for Each Central Bank

In the case of the United States, the Fed has no agreement with the government regarding gains or losses associated with its asset purchase program, and as is the case with the BoJ, will bear or receive such losses or gains itself. A look at the relationship between the cash flows of Federal Reserve District Banks and the Fed’s payments into the Treasury shows that they have changed over time. One major change made recently was related to the implementation of the Fixing America’s Surface Transportation (FAST) Act in December of 2015. The Act requires that the aggregate Federal Reserve Bank capital surplus not exceed 10 billion dollars and that amounts exceeding that be transferred to the Treasury. Under the prior system, Federal Reserve Banks were allowed to accumulate surplus up to the same amount of their paid-in capital before transferring any excess to the Treasury. But the FAST Act has compelled the Fed to divest itself of its capital surplus in this way, making it more difficult for the Fed to build up reserves against possible future losses.

Even so, the Fed is not in danger of falling into technical insolvency. Owing to accounting policy changes in 2011, any losses incurred by Federal Reserve Banks will not be charged to equity capital but instead booked as liabilities to the Treasury. According to the Fed, only the New York Federal Reserve Bank has done so in the past and only for a brief period. Even if the Fed should incur losses in the future, it could use future profits to pay down that liability rather than reducing its equity capital. As is the case with the BoJ today, when the Fed announced the rule changes in 2011, there was speculation that the Fed might face technical insolvency. However, this accounting policy change means that the Fed does not face the possibility of technical insolvency in structural terms.

In the Eurozone, member country central banks in addition to the ECB, have engaged in asset buying. Adopting the view that the financial independence of central banks is indispensable for effective monetary policy and confidence in central banks, the ECB has been encouraging the central banks of the Eurosystem member states to maintain sound finances. The ECB itself is able to set aside up to 20% of its annual revenue for reserves up to an amount equal to its paid-in capital. The central banks of the Eurosystem have themselves adopted provisions essentially along these lines. Should the ECB incur losses, it would first charge the losses against reserves. If that is not sufficient, the ECB Governing Council has the authority to offset the losses against the income of member country central banks. There are no provisions for Eurozone governments to make good any losses but there is substantial leeway for central banks to add to reserves.

In the case of the BoJ, supplementary provisions to the former Bank of Japan Act provided that if reserves are not sufficient to offset losses incurred in each business year, the government must provide supplementary funds equivalent to the shortfall. There is no provision for such compensation of losses under the new Bank of Japan Act which came into effect in 1998. Instead, the Bank may add to its reserves with the authorization of the Minister of Finance under Article 53(2). Based on this article, the BoJ began in the year ended March, 2016 adding to its provision for losses on bond transactions, with the balance of these provisions reaching about 3.1 trillion yen as of the end of the year ended March, 2017. As the BoJ sets aside reserves, the amount the Bank pays to the government (the government’s non-tax revenue) decreases by the same amount.

It could be said that the BoJ and the ECB are setting aside seigniorage now in anticipation of the risk of future losses. The Federal Reserve, on the other hand, will make good any future losses with future seigniorage. In the case of Britain, any such losses will be borne by HM Treasury.

No Room for Optimism Given Long-Term Consequences

In any case, the cost of normalizing monetary policy will impact government finances at some juncture. If the BoJ should incur losses larger than anticipated in the course of its policy normalization, it would be reasonable to assume that, like the Federal Reserve, it will treat the losses as a liability payable to the Ministry of Finance and then offset that liability with future seigniorage. Any massive losses or technical insolvency arising from an economic crisis would present problems, but if the inflation target of 2% can be reached, the assumption is that, even if the BoJ were technically insolvent, it would have no significant impact on confidence in the government or the currency. Indeed, the central bank of Chile even now has yet to resolve its negative capital position, but no problems seem to have arisen since the country’s economic and fiscal positions have been on the mend. The central bank of Israel also continues operations despite being technically insolvent.

That said, it would not be safe to say that confidence in the central bank will not suffer regardless of how large losses are, only because economic crises are not the cause of such losses or the banks’ capital accounts are technically remain unaffected.

In addition to the foregoing point made by Ueda, consideration should be given to the financial condition of the government. In the event that the central bank treats losses it incurs as liabilities to the treasury, the assumption is that it will then pay down those liabilities using future seigniorage. However, given the government’s potential incentive to acquire revenues for the treasury, it may not allow the central bank offsetting its losses with seigniorage. Should that be the case, the central bank’s impaired financial position might never be resolved, which in time might adversely impact confidence in the government or the currency.

Translated from “Nihon Ginko saimu choka wa aruka ― Zaimu akka ga choki-ka sureba kiken (Is the Bank of Japan Technically Insolvent? ― Dangers Involved in Long-Term, Deterioration of BoJ Financial Position),” Weekly Toyo Keizai, 8 July 2017, p.70-74. (Courtesy of Toyo Keizai Inc.) [July 2017]

Related posts:

Future of the Automotive Industry Strategies with a View to the Future of EVs and Beyond: Exploring the Application of Technologies to Other Fields

Future of the Automotive Industry Strategies with a View to the Future of EVs and Beyond: Exploring the Application of Technologies to Other Fields

Future of the Automotive Industry: Preparing for structural changes in the supply chain networks

Future of the Automotive Industry: Preparing for structural changes in the supply chain networks

ASEAN’s Problem of Declining Birthrates and Population Aging ― How to Cope with Widening Domestic Gaps

ASEAN’s Problem of Declining Birthrates and Population Aging ― How to Cope with Widening Domestic Gaps

20th Anniversary: Countries Affected by the Asian Financial Crisis Are Confronted with Common Issues Accompanied by Growth ― Japan Must Be a Successful Example of Tackling the Income Gap and Aging Population

20th Anniversary: Countries Affected by the Asian Financial Crisis Are Confronted with Common Issues Accompanied by Growth ― Japan Must Be a Successful Example of Tackling the Income Gap and Aging Population

No Need to Fear a Fall in Population

No Need to Fear a Fall in Population