Stalled Fiscal Consolidation:Private-Sector Financial Asset Surplus is Key

Key points:

- Private sector financial surplus can offset government financial deficit

- Domestic liquidity may be tight in second half of 2020s

- Long-term interest rates could rise before deficit in current account

Prof. Matsubayashi Yoichi

At a meeting of the Council on Economic and Fiscal Policy last January 23, the Cabinet Office announced its “Economic and Fiscal Projections for Medium to Long Term Analysis.” The projections show that, even if economic growth is achieved as targeted under its growth scenario, the government now projects that a surplus will not be achieved in the central and local government primary balance until the fiscal year ending March, 2028, or two years later than the last projection made in July, 2017.

Debt repayment will be limited since a portion of the increased revenue from the October 2019 consumption tax hike will be allocated to childcare support, and total factor productivity (representing technological advances in the macroeconomy), anticipated as an exogenous factor, is expected to be lower than previously thought.

The government expects the ratio of outstanding debt to GDP to follow a secular decline under the growth scenario. Under the more realistic growth rate projection of the baseline scenario, meanwhile, the debt to GDP ratio is seen declining gradually until the middle of the 2020s before turning up beginning in the year ending March, 2028. In the report the government adheres to its aim of achieving a surplus in the primary balance and clearly affirms the goal of steadily lowering the debt to GDP ratio. It seems that the government also regards the debt to GDP ratio as a target for restoring its fiscal position.

Public debt is a stock, and in order to lower the debt to GDP ratio, the basic procedure is to improve each year’s primary balance, which is a flow. But because this also depends on such factors as interest rates and the economic growth rate, the matter can get rather complicated.

In the present article, I would like to review the problem of fiscal sustainability, or whether or not the stock of government debt can be maintained in the future. I would also like to consider the issue from the perspective of the supply and demand for liquidity in the macroeconomy as a whole.

In its original sense, fiscal sustainability refers to a situation in which the government debt to GDP ratio is not continually rising into the future. One point which comes up in the discussion concerns the economic conditions under which government finances can be sustainable. We can identify several necessary conditions. First, if the nominal growth rate is higher than nominal long-term interest rates, the interest payment burden on the outstanding government bonds will be lower than the GDP growth rate, so the government’s fiscal position will be sustainable. Even if this condition is not satisfied, the government’s fiscal position would be sustainable if the primary balance is improving sufficiently.

There are already many empirical studies focusing on the sustainability of Japan’s financial position, and on the whole, and these studies generally conclude that it is not.

In its recent estimates, the Cabinet Office anticipates that, under the growth scenario, the primary balance will gradually improve, and through the year ended March 2026, the economic growth rate will be higher than the long-term interest rate, meaning that government finances in the future will be sustainable. It also anticipates that the debt to GDP ratio in the year to March 2028 will fall to about 158% of GDP.

When discussing the sustainability of a government’s fiscal position in the context of the country’s economy as a whole, valuable insights can be gained by considering the matter from the perspective of the supply and demand for liquidity in the macroeconomy overall. Specifically, one may get a better understanding of the government’s current financial position by taking into consideration the surplus or deficit of liquidity in all sectors of the economy, including the household, the business or the government sector. Below, let us consider this point from the perspective of flows and stocks.

Any given sector within a country may have a liquidity surplus or a liquidity deficit. Thus if we consider all the flows (over a fixed period) among these sectors, within the country as a whole, no surplus or shortfall of funds might appear. This is known as the balance of savings and investment, and seen from the perspective of flows, it’s possible to see how a government’s fiscal deficit (shortfall of funds) is compensated by other sectors.

Based on the Bank of Japan’s Flow of Funds Accounts, for example, Japanese households had a liquidity surplus of about ¥13 trillion in 2016, the Japanese business sector had a surplus of about ¥23 trillion, and the general government had a fund deficit of about ¥12 trillion. The sum of all of the three sectors together amounts to a surplus of about ¥24 trillion, and this surplus then became a capital outflow abroad. In this way, a liquidity deficit at the present time in the domestic government sector can be made good by a liquidity surplus in the private sector.

Over the longer term, however, caution is needed regarding the following two points.

First, even if the fiscal deficit improves pursuant to the Cabinet Office’s estimates, it is possible that liquidity may be tight depending on the size of the private sector’s liquidity surplus. From the second half of the 2020s, when the baby boom generation reach late old age, households will be using their savings in earnest. Meanwhile, the Japanese business sector is pessimistic about the future economic outlook and is retaining earnings while holding back on capital investments. As a consequence, they have built up a very large liquidity surplus. However, it is by no means certain that this trend will continue through the second half of the 2020s.

The government estimates also calculate cash flows by sector. Private sector cash flows (relative to GDP) are expected to shrink by about 50% during the period between the year ending March 2018 through the year ending March 2028. Thus if the government’s financial balance does not improve substantially, it might be made up by capital inflows from overseas.

This would mean a deficit in the current account and in financial markets might impact long-term interest rates.

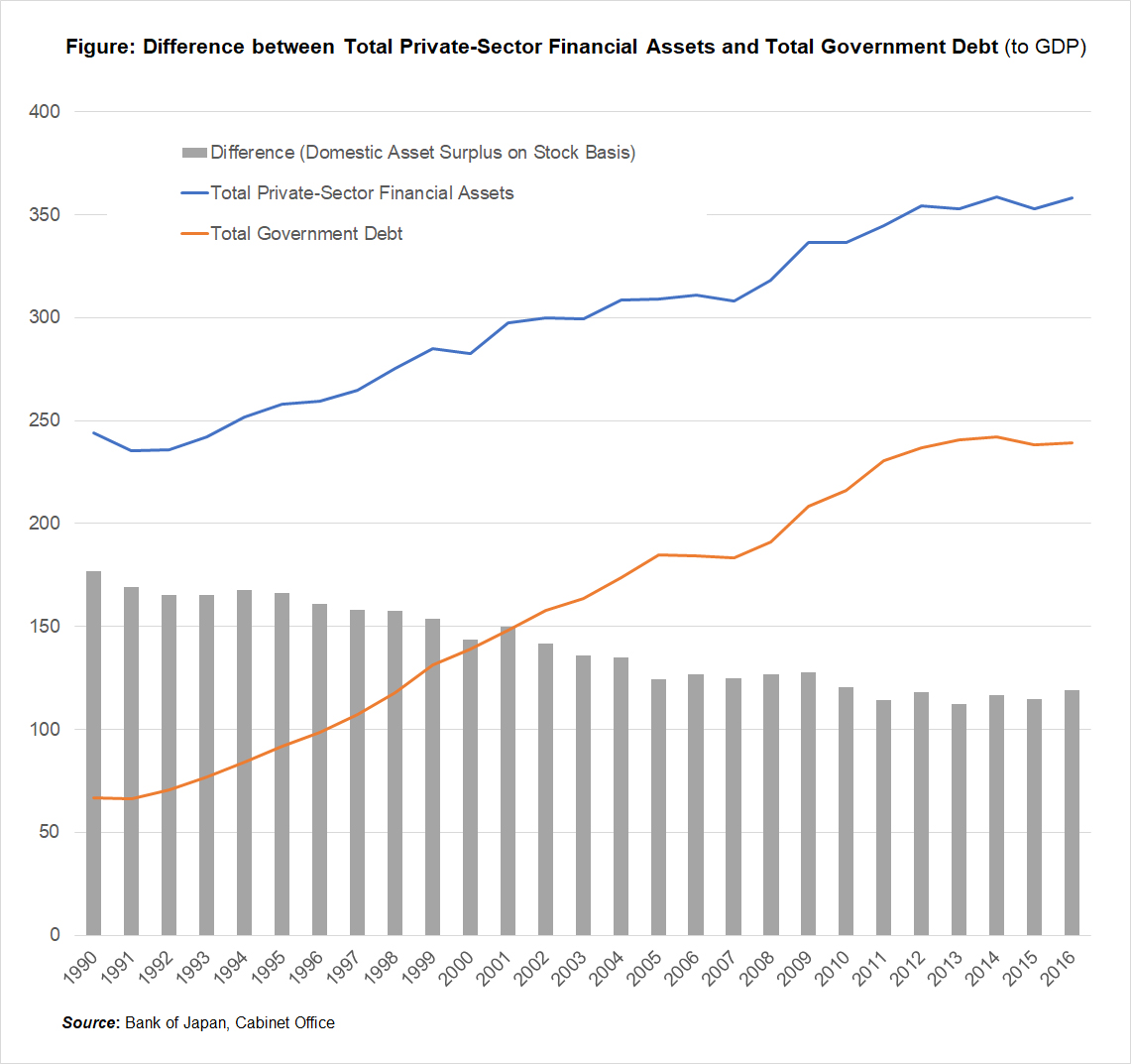

Second, the more important stage is better understood when considered from the perspective of stocks. Savings represent flows for household and business firms but at a fixed point in time represent the stock of financial assets held by the private sector. Meanwhile, the government has a very large outstanding debt balance. As shown in the accompanying figure, when seen relative to Japan’s GDP, the difference between the two (the domestic financial surplus on a stock basis) has been shrinking each year and was about 120% as of 2016.

Of course, not all private sector financial assets are held in the form of government securities. Moreover, the Bank of Japan holds a massive volume of Japanese government securities. However, according to the BoJ’s Flow of Funds Accounts, as of the end of 2017, nearly 40% was still held by financial institutions or in insurance or pension funds. In other words, compared to the debt of the government sector, the volume of financial assets held as stock in the private sector represents the degree of leeway within Japan to offset the government’s debt.

A study by Hideaki Matsuoka of the Japan Center for Economic Research found that if the domestic asset surplus on a stock basis were to fall below 100% of GDP, long-term interest rates would begin rising dramatically. If the trend shown in the bar graph were to continue along the same trajectory, the domestic financial asset surplus would fall under 100% of GDP in 2028. Two important points are relevant in this regard.

First, the domestic financial asset surplus could fall on a stock basis even if the ratio of government debt to GDP were to continue following a declining trend. According to Cabinet Office projections, the government debt to GDP ratio will continue declining over the long term. However, if the rising trend in the financial assets of the private sector begins to slow markedly in the future, it is possible that the overall domestic asset surplus could eventually decline on a stock basis. As mentioned above, there is no guarantee that the present level of savings in the household and business sectors will be maintained from and after the second half of the 2020s.

In other words, the question of the sustainability of government finances must be examined from a relative angle which takes into consideration the supply of liquidity.

Second, any drastic decline in the overall domestic financial asset surplus on a stock basis will very likely have a substantial impact not only on financial markets but on the real economy if and when it becomes a reality (most likely in the second half of the 2020s). Long-term interest rates could react dramatically at a stage prior to the appearance of a deficit in the current account. It is also possible that volatility in the market price of Japanese government securities could result in a high inflation rate. Moreover, these future risks could lead to broader instability among private sector economic actors, leading to a contraction of current consumption and investment activity.

It is critical to assess the sustainability of the government financial position from a diversity of perspectives which take into consideration the macroeconomy as a whole. This point needs to be borne in mind when the stability of the government debt to GDP ratio is set as a policy target.

Translated by The Japan Journal, Ltd. The article first appeared in the “Keizai kyoshitsu” column of The Nikkei newspaper on 9 February 2018 under the title, “Tonoku zaisei-kenzenka (Part II): Minkanbumon no shikinyojo kagi (Stalled Fiscal Consolidation (Part II): Private-Sector Financial Asset Surplus is Key).” The Nikkei, 9 February 2018. (Courtesy of the author)

Related posts:

Blueprint for the Future of Social Welfare (I) : Social Security Cutting Across Policies, Public Finance and Employment

Blueprint for the Future of Social Welfare (I) : Social Security Cutting Across Policies, Public Finance and Employment

Blueprint for the Future of Social Welfare (II) : Limiting State Responsibility to the Guaranteed Minimum

Blueprint for the Future of Social Welfare (II) : Limiting State Responsibility to the Guaranteed Minimum

Medical and Nursing Care Expenses and Social Security

Medical and Nursing Care Expenses and Social Security

HondaJet: Fulfilling the Dream of Soichiro

HondaJet: Fulfilling the Dream of Soichiro

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015