Japan’s economy shaken by the weak yen: Resonance with and impact on rising resource prices

Komine Takao, Professor, Taisho University

Key points

- Evaluating the value of the yen from an export sector and producer perspective

- Energy prices were stable when the yen depreciated in 2013

- Aim to support yen appreciation on the back of enhanced economic strength

Prof. Komine Takao

The depreciating yen together with the rise in imported energy prices has caused import prices to rise, with the ripple effect of a rise in domestic prices. In response, the “bad yen depreciation theory,” which holds that the weak yen will have a negative impact on the Japanese economy, has surfaced. This represents a significant departure from the dominant long-held notion in Japan that a weak yen is good news and a strong yen is bad news for the economy. This situation can be attributed to several factors.

I begin with an overview of the economic impact of a weak yen. The depreciation of the yen has a range of effects on the Japanese economy as a whole through changes in export and import prices. In the case of imports, the depreciation of the yen directly translates into higher yen-based import prices. In the case of exports, however, there is leeway to modify the selling price of foreign currency, so yen-based prices will rise to some extent and prices based on foreign currencies will fall to some extent. In other words, yen-based export and import prices both rise when the yen weakens, but the degree of increase is greater for import prices.

The impact of this change in export and import prices will be felt throughout the economy. Rising import prices raise costs for domestic firms, so domestic prices will rise (causing import inflation). Higher consumer prices reduce real household income and dampen household consumption. A rise in import prices will also reduce the volume of imports after a certain time lag.

On the other hand, changes in export prices benefit the export industry. Export volumes will increase after a certain time lag as export profitability improves and prices become more competitive, stimulating domestic production.

From the above overview, we see that, first, both a weak yen and a strong yen have positive and negative effects on the economy. Therefore, to apply the label of “good” or “bad” to the yen’s depreciation or appreciation is an unacceptably broad generalization. It depends on how the positive and negative aspects of each are evaluated. Second, economic impacts manifest differently across economic sectors. A weaker yen benefits the producer sector, particularly export-related industries, but negatively impacts import-related industries and households.

Japan has welcomed a weak yen and has had an aversion to a strong yen because it has evaluated the impact of yen rate fluctuations from the perspective of the export sector rather than the import sector, and from the perspective of producers rather than consumers. Given that the finances of households can only benefit from a strong yen, it is curious that a strong yen has had such a poor reputation in the past.

Next, I will consider the background to the “bad yen depreciation theory.” The Japanese economy saw a significant depreciation of the yen from the end of 2012 under Abenomics. During this period, the weak yen was largely evaluated positively. However, in 2022, the weak yen has been viewed unfavorably. It may be questioned whether this is evidence of a shift in Japan’s traditional aversion to a strong yen.

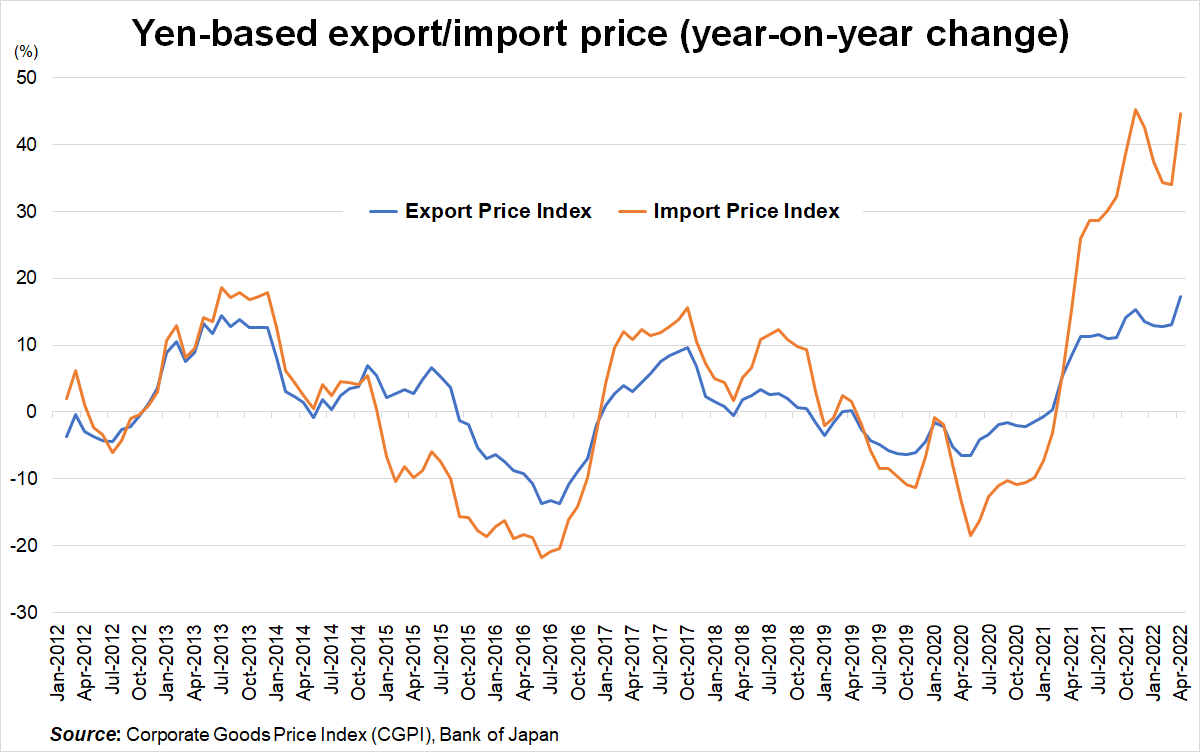

The figure shows the change in yen-based export and import prices. In both 2013 (the last time the yen weakened) and 2021 and beyond (this time), import prices rose faster than export prices. However, while the gap between import prices and export prices was modest last time, this time import prices are significantly higher than export prices. The large rise in import prices is due to the rise in energy prices.

Since import prices rose 35% in the first quarter of 2022 compared to the previous year and the yen-dollar rate fell by 8.8% during this period, the weak yen accounted for around a quarter of the increase in import prices.

This explains the emergence of the “bad yen depreciation theory” this time around. Because crude oil prices were stable in 2013, the effect of the weak yen was obvious. Manufacturing export earnings turned around and the rise in import prices lifted consumer prices out of negative territory. The weak yen was what made Abenomics a success. This time, however, crude oil prices have increased drastically, resulting in higher costs for the export industry and rising consumer prices.

The “bad yen depreciation theory” has emerged not because of the weak yen per se, but because the weak yen, when combined with rising energy prices, has caused import inflation. In this case, too, the impact of the weak yen when considered in isolation remains largely unchanged.

When the Bank of Japan Governor Kuroda Haruhiko reiterates his view that a weak yen is generally positive for the economy, he is referring to the impact of the weak yen when considered in isolation. The rise in energy prices themselves is beyond our control, so complaining is futile. The weak yen, on the other hand, is a potential source of discontent given that it reflects the state of the Japanese economy itself.

If this supposition is correct, it would seem that the long-standing fear of a strong yen has not been dispelled. In the most recent scenario, too, the “bad yen depreciation theory” would not have emerged if the yen had depreciated without an increase in energy prices. If the yen appreciates again in the future, the “bad yen appreciation theory” will appear, and aversion to a strong yen will gain ground once more.

If the “bad yen depreciation theory” is to be adopted in the future, I believe it should be exploited as an opportunity to shift policy priorities, firstly away from overcoming deflation and toward responding to import inflation. In this regard, it is important to note that the depreciation of the yen is due to a policy divergence between the government and the Bank of Japan (BoJ). The government is injecting 6.2 trillion yen to promote measures to combat high oil prices and consumer prices, as well as providing subsidies in an effort to curb gasoline prices. Meanwhile, the BoJ continues its super monetary easing policy aimed at overcoming deflation. Thus, despite the government’s concern about rising prices, the BoJ is attempting to raise prices.

It is curious that such a blatant policy inconsistency is hardly debated. This policy inconsistency is weakening the yen by expanding the domestic and foreign interest rate differential, accelerating import inflation.

In mid-April, the consumer price index (overall) in the Tokyo metropolitan area rose 2.5% year on year. It is likely that the government and BoJ’s aim of a 2% price increase will be achieved as of April. If long-term interest rates are artificially suppressed even as consumer prices rise, real household income will fall and savings will decline, exacerbating public discontent. Monetary policy should align long-term interest rate fluctuations more closely with prevailing conditions.

The government’s price policy is also questionable. As long as imported energy prices rise, it is difficult to avoid a negative impact on the economy. In the long run, the use of financial measures to control cost increases is not a viable option. Also, higher consumer prices do not provide increased added value, making wage hikes difficult. We should aim to achieve a more energy-saving economic structure by ensuring that prices genuinely reflect cost increases.

The second shift in policy priorities should involve a reconsideration of the attitude toward exchange rates from a long-term perspective. Although a weak yen benefits the export industry and is positive for the economy, the increase in corporate earnings is not considered permanent income and is unlikely to result in higher wages and increased capital investment because it is similar to windfall profits that are unrelated to corporate efforts. A weak yen would also make it easier for low-profit marginal enterprises to survive, which may lower productivity and efficiency in the economy as a whole. The undervaluation of Japanese manpower by other countries will result in a return to the era of exploiting low-cost labor as a selling point. Long-term yen rates will reflect the assessment of Japan’s economic power, crisis-response capability, and problem-solving capability. Long term, the goal should be to boost Japan’s economic power and value-added production capacity, while allowing the yen to appreciate to reflect this.

Translated by The Japan Journal, Ltd. The article first appeared in the “Keizai kyoshitsu” column of The Nikkei newspaper on 16 May 2022 under the title, “Enyasu ni yureru Nihon keizai (I): Shigen kakaku josho to kyoshi, dageki (Japan’s economy shaken by the weak yen (I): Resonance with and impact on rising resource prices).” The Nikkei, 16 May 2022. (Courtesy of the author)

Keywords

- Komine Takao

- Taisho University

- economy

- yen

- depreciation

- “bad yen depreciation theory”

- weak yen

- strong yen

- resource prices

- energy prices

- import prices

- import inflation

- export prices

- consumer prices

- deflation

- Bank of Japan

- interest rates

- household income

- exchange rates

- value-added production

Related posts:

Russian Violence and a Shaken Order: A “Crisis from an Eagerly Awaited Yen Appreciation” Posing a Greater Risk than the Situation in Ukraine

Russian Violence and a Shaken Order: A “Crisis from an Eagerly Awaited Yen Appreciation” Posing a Greater Risk than the Situation in Ukraine

Making the most of human capital: Removing policy obstacles to women’s advancement

Making the most of human capital: Removing policy obstacles to women’s advancement

A Wavering International Trading Order: Putting an End to “Global Optimal Procurement”

A Wavering International Trading Order: Putting an End to “Global Optimal Procurement”

THE BANK OF JAPAN'S EFFORTS TOWARD OVERCOMING DEFLATION

THE BANK OF JAPAN'S EFFORTS TOWARD OVERCOMING DEFLATION

GAUGING JAPAN'S "SOVERRIGN RISK"

GAUGING JAPAN'S "SOVERRIGN RISK"