Sanaenomics: Tackling a Historic Turning Point

In her policy speech at the 219th session of the Diet on October 24, 2025, Prime Minister Takaichi Sanae said, “I will strive to build a robust economy, turning people’s unease and apprehension over their current lives and the future into hope, and foster a Japan that is stronger and more prosperous. I will deal with the challenges facing the international community as I embark on restoring Japanese diplomacy that flourishes on the world’s center stage.”

Photo: Cabinet Public Affairs Office

What is needed to sustain and strengthen the evolving Japanese economy? In this text, the author—a private-sector member of the Council on Economic and Fiscal Policy—discusses the economic policies and challenges that the Takaichi administration should pursue in its quest for a “free economy” and a “strong nation.”

On October 21, 2025, Takaichi Sanae took office as Japan’s 104th prime minister. While she is notable for being Japan’s first female prime minister, she is also remarkable in other ways. She is not from a political dynasty; she graduated from a public high school and paid her own tuition to attend a national university. She is not a career bureaucrat from ministries or agencies. Within the Liberal Democratic Party, she belongs to no faction yet has become the foremost policy expert in the political arena. It is precisely Prime Minister Takaichi’s capabilities that we should focus on.

Expectations are high for Prime Minister Takaichi’s policies. However, the challenges we face are enormous.

Japan’s economy now stands at a historic turning point. Economists and commentators repeatedly declare “this is the turning point,” leading to the joke that we somehow end up back where we started. However, this time it is undoubtedly a turning point.

First, the world is entering an era of great turmoil. The causes of this turmoil are widespread, ranging from geopolitical issues such as Russia’s invasion of Ukraine and rising tensions in East Asia to economic issues such as trade wars, Peak China (a slowdown in the Chinese economy), and frequent cyber attacks.

The greatest concern above all else is whether Pax Americana will come to an end. Is the United States abandoning its role as a global power and stepping down from its hegemonic position?

Second, the Japanese economy is finally showing tangible signs of escaping deflation and returning to normal. The question now is whether Japan can transition steadily from a prolonged deflationary period to a period of mild inflation.

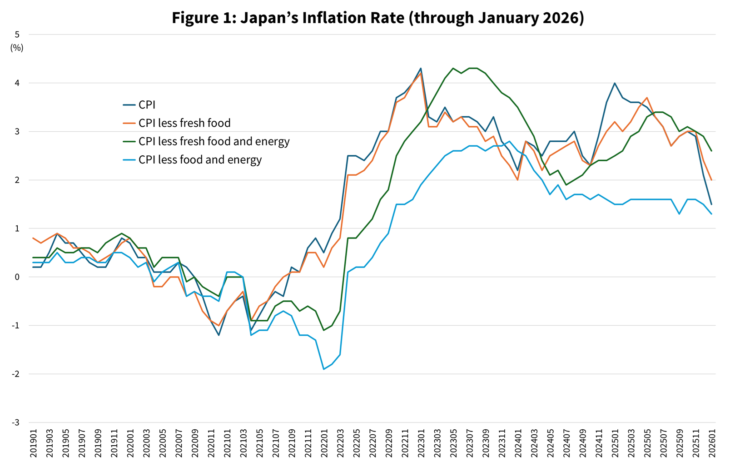

Source: Created by the author based on the Statistics Bureau of the Ministry of Internal Affairs and Communications

Currently, nominal gross domestic product (GDP) has been growing steadily, while real GDP appears to be stagnating. This gap is due to inflation. The headline Consumer Price Index (CPI) nationwide composite inflation rate used to stay at around 3%, but has come down to 1.5% (January 2026), while the Western-style core CPI, which excludes food (excluding alcoholic beverages) and energy prices, is 1.3%. Food prices accounted for the majority of the inflationary pressure, and a closer look reveals that individual prices, such as rice, were also rising. The so-called cost-push element was strong, and the demand-pull element, which causes inflation as wages and inflation and demand strengthens, is weak.

The issue is the current state of the economy and its outlook. Currently, the labor market appears weak due to Trump’s tariffs, and the outlook is extremely uncertain.

Many Japanese economists have predicted negative growth in the second half of 2025. Additionally, shocks with a negative supply-side impact similar to those caused by the COVID-19 pandemic and the Russian invasion of Ukraine may occur more frequently in the future.

On the other hand, there are encouraging signs of a new era dawning, with a shift toward a mild inflation regime. Astute journalists like Takita Yoichi have highlighted the Bank of Japan Review Series’s AI-donyu ga Seisansei ni Ataeru Eikyo: Gainenseiri to Kokusaihikaku (The impact of AI adoption on productivity: Conceptual overview and international comparison)[1] and the September “Tankan” (Short-Term Economic Survey of Enterprises in Japan). Due to the labor shortage, there has been a surge in software investment among small and medium-sized enterprises in the wholesale, retail, and accommodation and food service industries, which have been slow to invest in labor-saving and automation technologies. “The new LDP (Liberal Democratic Party) president, Takaichi, faces one challenge: economic transformation is upon us. Don’t let it stop. This is it.” (Takita Yoichi, Keizai Daitenkan no Gyakusetsu: Takaichi Sanae Jiminto Shinsosai wa Nagare ni Hazumi wo (The paradox of a major economic shift: Takaichi Sanae, the new LDP president, gives momentum to the trend), Nikkei Online, October 5, 2025).

A free economy and a strong nation

What is needed to maintain this trend? Let’s review the principles of the Takaichi administration’s economic policies. In order to “foster a Japan that is stronger and more prosperous,” above all else, a robust economy must be fostered. Prime Minister Takaichi’s policy, Sanaenomics, is absolutely correct.

So, what is needed to foster a robust economy? A free market economy is the basis of the economy. An open, competitive market is a source of vitality and entrepreneurial activity. However, we must also pursue another element: security.

The challenges are mounting in areas such as national defense, healthcare, food, energy, natural disaster response, supply chain resilience, and economic security. There may be trade-offs between freedom and security. This is because a free market economy seeks global connectivity and efficiency, whereas security often requires incurring costs, even if it means sacrificing efficiency. Achieving this balance is a worldwide challenge. Nevertheless, AI and data centers require vast amounts of inexpensive electricity, and fostering the defense industry is also an urgent task. Realizing and sustaining a free market economy requires the essential role of government.

According to a recent economic concept, Japan needs to improve and strengthen its state capacity. State capacity refers to a government’s ability to effectively implement and achieve its goals. More specifically, it refers to the government’s ability to provide public goods, enforce laws, and manage the economy. Today, many people are likely questioning the capabilities of the Japanese government. A strong nation does not have to be authoritarian. A strong nation does not mean an authoritarian one. What Japan needs today is to strengthen its state capacity in order to maintain a free market economy, and to respond at a high level to issues such as national defense, tax collection, foreigners’ dealings, intelligence, and economic security.

“High-pressure economy” and “policy coordination”

More specifically, in terms of policy theory, Sanaenomics is based on the concepts of a “high-pressure economy” and “policy coordination.” The concept of a “high-pressure economy” originated with John M. Keynes, who said, “Thus the remedy for the boom is not a higher rate of interest but a lower rate of interest! For that may enable the boom to last. The right remedy for the trade cycle is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom.” (John Maynard Keynes, The General Theory of Employment, Interest and Money (1936), p. 322).

This idea was made clearer by American economist Arthur M. Okun. In a 1973 paper, Okun suggested that nurturing aggregate demand could lead to improvements on the aggregate supply side, such as an increase in labor supply.[2] This idea was revived in 2016 by Janet Yellen,[3] then Chair of the Federal Reserve (FRB).

From this perspective, the ideal policy would be to strengthen aggregate supply while maintaining aggregate demand, resulting in policy coordination.

First, maintaining aggregate demand is a prerequisite. In a “high-pressure economy,” the interdependence between aggregate demand and aggregate supply is important. Nurturing the economy encourages behavioral change among households and businesses. These changes are already evident, as evidenced by a surge in software investment by small and medium-sized enterprises amid labor shortages, as well as increased labor force participation by young people, women, and the elderly.

Equally important is government behavioral change. With inflation returning, the income tax deduction amount, known as the “1.03-million-yen barrier,”[4] which has been frozen since 1995, is becoming a problem. If the tax system remains unchanged, it will distort the labor supply as wages and incomes rise. It is essential that the government implement policy innovations, including those related to the tax system.

Of course, it is undesirable to force the economy to overheat. However, the decline of the Japanese economy stems from a lack of coordination between fiscal and monetary policies. A prime example is Abenomics, the policy under which the government increased the consumption tax twice while easing monetary policy.[5] Hasty tax and interest rate hikes must be avoided.

Second, the aggregate supply must be strengthened. Given the US-China trade war, geopolitical risks, and economic security concerns, restructuring supply chains is a key issue.

In the food sector, rising rice prices have become a challenge. The underlying driver is the rice production reduction policy.[6] In addition to this shift, we should provide incentives to improve supply capacity by providing individual income compensation to farmers and encouraging people to enter the agricultural industry. Regarding electricity, instead of restarting nuclear power plants after confirming their safety, we should focus on developing alternative energy sources, such as small modular reactors (SMRs)[7] and nuclear fusion. Furthermore, human resources are crucial. In the short term, we must reassess excessive work style reforms,[8] restore an environment in which willing workers can find employment, and invest in basic science, technology, education, and training.

This issue relates to the need for immigrants and foreign workers, a topic often discussed in the context of immigration policy. Due to its declining fertility rate, Japan’s labor force will rapidly decline,[9] making the phrase “we have no choice but to rely on immigrants and foreign workers” a common refrain. However, if there is a labor shortage, investing in automation, mechanization, and labor-saving measures is also an option. While we may ultimately need a certain number of immigrants and foreign workers, this decision should be made after considering its impact on the labor market, industrial structure, and security, as is done in other countries. Furthermore, immigrants are people with diverse histories, cultures, traditions, and religions. At the very least, acceptance requires a national debate, and Prime Minister Takaichi’s policy of “considering how to deal with the situation from a zero-base perspective” is absolutely correct.

Third, “integrated policy coordination” is necessary. Just as recent inflation is a combination of cost-push and demand-pull factors, a combination of multiple policies is sometimes necessary to solve a problem.

In the case of inflation, it is necessary to strengthen the supply side, which is a cost-push factor, while also strengthening the demand side, which is a demand-pull factor. In this way, it is desirable for the government to closely link stabilization (fiscal and monetary) policies, growth policies, trade policies, and redistribution policies, and to implement them in a consistent manner according to policy objectives.

What is “responsible and proactive public finances”?

Are there any concerns about how Sanaenomics manages fiscal and monetary policy? Let’s start with fiscal policy. Some are concerned that Prime Minister Takaichi’s proactive public finances pose a threat to Japan’s fiscal sustainability.

Prime Minister Takaichi’s slogan is “responsible and proactive public finances.” This means three things. First, Prime Minister Takaichi has repeatedly stated that she has never denied the importance of fiscal sustainability. The problem is that, as history has shown, fiscal sustainability cannot be achieved through tax increases and spending cuts. Rather, economic growth is the permanent source of revenue, and without economic growth, there can be no fiscal consolidation.

Second, this gives rise to the idea that government spending which contributes to growth should be considered an investment. Borrowing is desirable if it generates revenue that exceeds costs and leaves assets remaining.

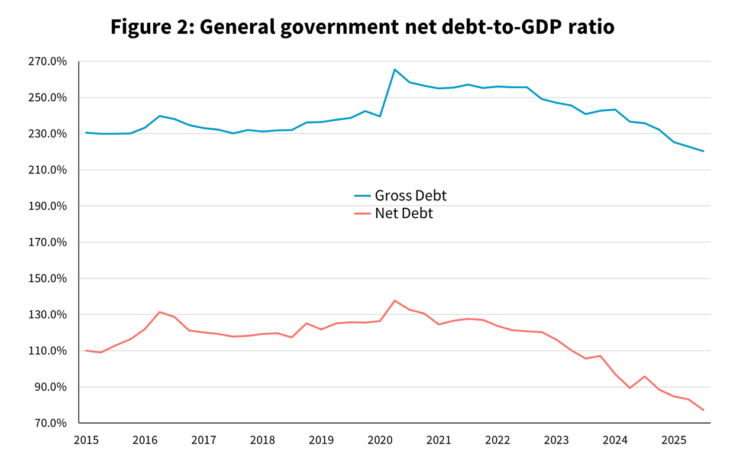

Source: Created by Hoshino Takuya of Dai-Ichi Life Research Institute based on the Bank of Japan’s Flow of Funds Accounts.

Third, this leads to the argument that the goal should be to gradually reduce the general government’s net debt-to-GDP ratio. The media and others tend to discuss Japan’s finances in terms of the fiscal balance itself and the total debt-to-GDP ratio. However, if government spending is a quality investment, then assets will increase; therefore, it is correct to consider net debt. Additionally, it is appropriate to consider debt in terms of repayment capacity and its ratio to GDP.

Furthermore, as inflation returns and nominal GDP grows steadily, tax revenues increase and the general government’s net debt-to-GDP ratio improves rapidly. According to the Bank of Japan’s (BoJ) flow of funds statistics, this ratio reached 77% in the third quarter of 2025, marking the lowest level since 2008 (see Figure 2).

Normalizing the economy is the key to normalizing monetary policy

When it comes to monetary policy, there is much discussion about when interest rates will be raised. It is as if raising interest rates would normalize monetary policy. However, the BoJ’s goal is price stability, and achieving a sustained and stable price stability target of 2%. Interest rates are merely a means to achieve this goal, and raising interest rates does not mean normalization. In fact, if raising interest rates causes the economy to decline, it would be pointless. Interest rates will be “normalized” as a result of economic normalization.

From this perspective, if the BoJ were to raise interest rates in the face of strong cost-push factors and negative real GDP growth, it would need to provide the public with a clear explanation. Moreover, monetary policy is based on current data and future forecasts rather than simply specifying a deadline for interest rate hikes.

Is a new joint statement between the government and the Bank of Japan necessary?

In this regard, 13 years have passed since the government and the BoJ issued the Joint Statement of the Government and the Bank of Japan on Overcoming Deflation and Achieving Sustainable Economic Growth. Now that a complete escape from deflation is becoming a reality, should a new joint statement be issued?

The US Federal Reserve and the Bank of Canada review their monetary policy framework every five years. The joint statement defines the relationship between the government and the central bank; therefore, it is not the same as a review. However, depending on the situation, it is possible that the joint statement could be periodically revised to ensure that the government and the central bank share a common understanding. Given the current situation, the government has yet to declare that Japan has overcome deflation; therefore, a review of the joint statement would likely be premature. Nevertheless, I would like to clarify the key discussion points.

First, the joint statement itself embodies the spirit of Article 4 of the Bank of Japan Act,[10] which stipulates that the government and the BoJ must work closely together and communicate to maintain consistency in economic policy. This is desirable from the perspective of macroeconomic policy coordination.

Second, from a policy coordination perspective, consistency between policies should be pursued. In particular, given the events since 2013, we must avoid a scenario in which monetary easing and fiscal austerity coexist. At the same time, we must clearly explain how fiscal and monetary policies interact, such as how nominal economic growth improves fiscal conditions.

Third, the current situation calls for policy coordination. Furthermore, while changing targets to nominal GDP levels and growth rates, for example, may have theoretical merit, it would raise issues such as who is responsible.

Internal and external risks

Various risks are involved in managing the economy going forward.

First, although the risk of a return to deflation is currently considered low, the specter of “Japanification,” which is defined by slow growth, low inflation, and low interest rates, still looms large. In Japan, corporations remain net savers.

Second, besides the demand side, we should consider the possibility that various cost-push shocks will arrive successively in the future. Specific examples include infectious diseases, geopolitical risks, and natural disasters.

Third, considerable uncertainty remains surrounding US economic policy. In addition to preparing for the negative impact of Trump’s tariffs, we must also be wary of the Mar-a-Lago Agreement, about which some have been whispering. As Japan’s macroeconomy was disrupted by the Plaza Accord[11] in September 1985, which encouraged a stronger yen, careful attention is required when implementing macroeconomic policy.

Fourth, we should pay attention to financial markets. In the United States, a deterioration in lending standards has become apparent amid a strong stock market. As the credit cycle enters a later stage, some are questioning whether a bubble is forming.

In order to address these risks and crises, the government must thoroughly coordinate its policies.

Restoring a Japan with hope and expectations for the future

At the beginning, I stated that the Japanese economy is at a historic turning point. We must pool our wisdom and strength to navigate this turning point as effectively as possible and further promote the prosperity of the Japanese economy.

Finally, I would like to share a post from Kawabuchi Saburo, Chairman of the Japan Top League Alliance, on X (formerly Twitter), dated 6 October 2025, following the election of Prime Minister Takaichi as president of the Liberal Democratic Party.

“I have a feeling that something will change in Japan now that Takaichi-san has become president of the LDP. Perhaps it’s because people hope for this, even though they know it won’t be easy. This is a major turnaround that defied the predictions of most political commentators, which makes me feel all the more confident that she will restore hope to Japan’s future. Please do your best.”

The question now is whether the expectations and hopes he speaks of will be realized.

Translated from “Rekishiteki Tenkanten ni Idomu Sanaenomics (Sanaenomics: Tackling a Historic Turning Point),” Voice, January 2026, pp. 60–69. (Courtesy of PHP Institute) [February 2026]

WAKATABE Masazumi

WAKATABE MasazumiProfessor, Faculty of Political Science and Economics, Waseda University / A member of the Council on Economic and Fiscal Policy, Cabinet Office / Former Deputy Governor, Bank of Japan

Born in Kanagawa Prefecture in 1965. Graduated from the Graduate School of Economics at Waseda University and the University of Toronto Graduate School of Economics after completing a doctoral course. He has served as a professor at the Faculty of Political Science and Economics at Waseda University since 2005, and has also served as a visiting scholar at the University of Cambridge, George Mason University, and Columbia University. He served as Deputy Governor of the Bank of Japan from March 2018 to March 2023. His major works include Keizaigakusha-tatchi no Tatakai — Economikusu no Kokogaku (Economists’ Struggle: The Archaeology of Economics) (Toyo Keizai Inc., 2003), Showa Kyoko no Kenkyu (Studies on the Showa Depression) (co-authored, Toyo Keizai Inc., 2004, winner of the 47th Nikkei Economic Book Culture Award), Kiki no Keizaiseisaku (Economic Crises and Policy Responses) (Nippon Hyoronsha, 2009, winner of the 31st Ishibashi Tanzan Award), Japan’s Great Stagnation and Abenomics (PalgraveMacmillan, 2015).

[1] https://www.boj.or.jp/research/wps_rev/rev_2025/rev25j10.htm (in Japanese)

[2] Arthur M. Okun, 1973. “Upward Mobility in a High-Pressure Economy.” Brookings Papers on Economic Activity, 4(1): 207–262.

[3] Janet Yellen, 2016. “Macroeconomic Research After the Crisis.”

[4] The “1.03-million-yen barrier” means that if a person earns less than 1,030,000 yen from part-time work and has no other income, he or she is not subject to income tax and his or her spouse is entitled to a spousal deduction if certain requirements are met.

[5] The Abe administration implemented two increases to the consumption tax: from 5% to 8% in April 2014, and from 8% to 10% in October 2019.

[6] From the 1970s to 2018, the Japanese government implemented the rice paddy reduction policy, a production adjustment measure designed to curb the overproduction of staple rice and stabilize prices. The policy encouraged farmers to leave land fallow or switch to growing soybeans or wheat and provided subsidies to reduce the amount of land used for rice paddies.

[7] These next-generation reactors are small, with an output of less than 300 MW per unit. Their components are manufactured as modules in factories and assembled on site. They are expected to improve safety, reduce construction costs and time, and provide flexibility in installation locations. They can be used for multiple purposes, such as carbon-free power generation and hydrogen production. Development is progressing in countries around the world.

[8] The Abe Shinzo administration launched this policy as a pillar of the “third arrow” of Abenomics, the structural reform initiative. The policy aims to address structural issues in Japan’s working environment, including the decline in the working-age population due to a low birthrate and an aging population, long working hours, and wage disparities based on employment type.

[9] https://www.japanpolicyforum.jp/politics/pt201401201524543388.html

[10] Article 4: Taking into account the fact that currency and monetary control is a component of overall economic policy, the Bank of Japan must always maintain close contact with the government and exchange views sufficiently, so that its currency and monetary control and the basic stance of the government’s economic policy are mutually compatible.

[11] On September 22, 1985, at the Plaza Hotel in New York, the finance ministers and central bank governors of the G5 (Japan, the United States, the United Kingdom, Germany, and France) agreed to a historic agreement to correct the excessive strength of the dollar and to coordinate efforts to weaken it. The primary objective was to reduce the U.S. trade deficit. This resulted in a rapid appreciation of the yen, plunging Japan into a bubble economy.

Keywords

- Sanaenomics

- Takaichi Sanae

- turning point

- high-pressure economy

- integrated policy coordination

- inflation

- immigration

Related posts:

The Dilemma between Free Trade and Economic Security

The Dilemma between Free Trade and Economic Security

What Is Meant by Supply Chain Resilience?

What Is Meant by Supply Chain Resilience?

Japan’s International Cooperation Seen from Palau: Rising Geopolitical Interests, Principles and Strategies under Scrutiny

Japan’s International Cooperation Seen from Palau: Rising Geopolitical Interests, Principles and Strategies under Scrutiny

China’s Expanding Presence in Central Asia: Its Global Strategy and Public Responses

China’s Expanding Presence in Central Asia: Its Global Strategy and Public Responses

A Policy Vision Beyond Abenomics

A Policy Vision Beyond Abenomics